Narratives are currently in beta

Key Takeaways

- Growth in high-margin categories aims to improve net margins and profitability through stronger product mix and pricing strategies.

- Expansion in Professional Hygiene targeting emerging markets is expected to drive revenue growth and capture new market demands.

- Currency fluctuations and rising raw material costs threaten earnings and margins, while restructuring and debt issues pose additional risks to growth and liquidity.

Catalysts

About Essity- Develops, produces, and sells hygiene and health products and services in Europe, North and Latin America, Asia, and internationally.

- Essity is aiming for accelerated growth in high-margin categories within Consumer Goods, such as incontinence care and Feminine Care, which is expected to improve net margins through a stronger product mix and pricing strategy.

- Increased focus on expanding Professional Hygiene in emerging markets, where only 20% of sales currently occur, is intended to drive revenue growth through greater market penetration and capturing emerging market demands.

- The successful restructuring efforts in Professional Hygiene and continuous improvements in pricing agility across the business are likely to bolster earnings and maintain stable EBITA margins despite market volatility in raw material costs.

- Essity plans to scale Health & Medical by leveraging its strong brand and market position, targeting margin improvements and enhanced profitability as volume scales improve operating leverage.

- Consistent cash flow generation and a strong balance sheet enable ongoing share buybacks, projected to enhance earnings per share, thus increasing shareholder value over time.

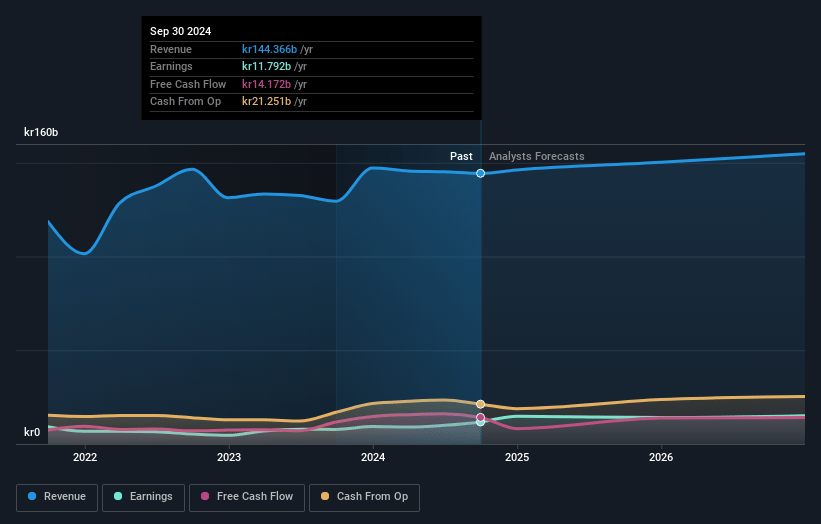

Essity Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Essity's revenue will grow by 4.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 8.2% today to 9.3% in 3 years time.

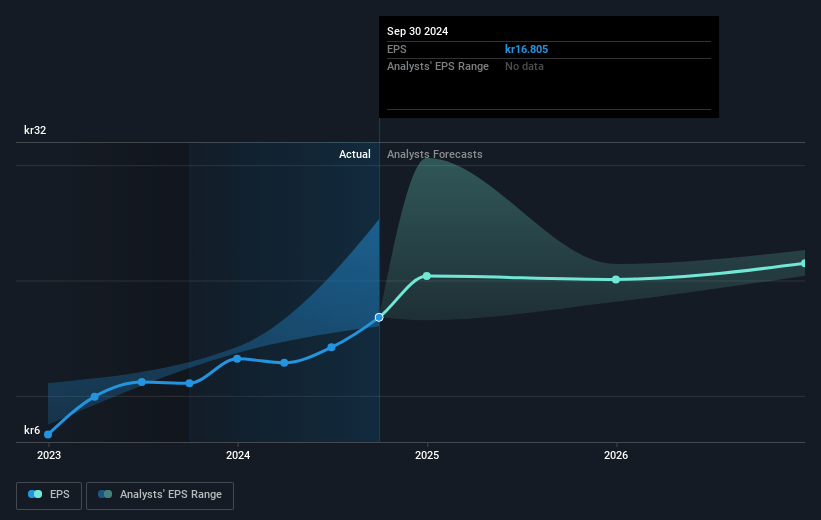

- Analysts expect earnings to reach SEK 15.3 billion (and earnings per share of SEK 22.12) by about January 2028, up from SEK 11.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.9x on those 2028 earnings, down from 17.5x today. This future PE is lower than the current PE for the GB Household Products industry at 23.7x.

- Analysts expect the number of shares outstanding to decline by 0.29% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.5%, as per the Simply Wall St company report.

Essity Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's EBITA declined by 1% year-over-year due to currency translation effects, which highlights the risk of fluctuating foreign exchange rates impacting future earnings.

- The Professional Hygiene segment experienced an organic sales decline of 0.8%, signaling potential challenges in maintaining growth, which could affect overall revenue.

- Increased raw material costs, especially for wood pulp, have raised concerns about sustaining profit margins, indicating risk to net margins if costs continue to rise.

- Restructuring activities in North America and Europe for Professional Hygiene have temporarily impacted growth, suggesting potential risks to consistent revenue growth across all segments.

- The bondholder dispute and early repayment demands could pose a financial risk, potentially affecting liquidity and net debt ratios if not resolved favorably.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of SEK 326.91 for Essity based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of SEK 380.0, and the most bearish reporting a price target of just SEK 270.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be SEK 163.8 billion, earnings will come to SEK 15.3 billion, and it would be trading on a PE ratio of 16.9x, assuming you use a discount rate of 4.5%.

- Given the current share price of SEK 295.7, the analyst's price target of SEK 326.91 is 9.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives