Key Takeaways

- Strong demand, robust digitalization trends, and a disciplined cost structure position Asseco Poland for sustained earnings growth and margin expansion across core sectors.

- Aggressive M&A and proprietary platform expansion bolster market share, enabling cross-selling, enhanced pricing power, and resilient, high-quality recurring revenue streams.

- Heavy reliance on core sectors and slow adaptation to tech trends expose the company to margin pressure, market share loss, and increased regulatory and innovation-related costs.

Catalysts

About Asseco Poland- Produces and sells software products worldwide.

- Analysts broadly agree that public and enterprise software demand will remain strong, but the current growth rates-nearly 20% year-on-year in public sector software and double-digit contract backlog increases-suggest that Asseco Poland could outperform even optimistic expectations for revenue and net margin expansion, especially as digitalization accelerates in core sectors like healthcare, energy, and government.

- Analyst consensus anticipates some moderation in margin gains, but Asseco Poland's disciplined cost structure, operational leverage, and transition of large projects into more profitable maintenance phases may drive a longer-term improvement in group-wide net margins and cash flow conversion than currently forecast.

- The company's aggressive and ongoing M&A program, with eight new additions across diverse geographies in Q1 alone, positions Asseco Poland to rapidly scale its cloud, AI, and specialized fintech offerings across high-growth markets, catalyzing above-trend revenue and EPS growth as integration synergies are realized.

- Expansion of proprietary, in-house software platforms for banking, insurance, and healthcare not only supports pricing power and higher gross margins but also enables durable cross-selling opportunities as cloud adoption and regulatory demands reshape IT budgets, leading to sustained earnings growth.

- With increasing regulatory emphasis on cybersecurity and data privacy-especially within the EU-and Asseco's established credibility as a trusted European vendor, the company is poised to capture outsized share of mission-critical government and financial contracts, anchoring high-quality, recurring revenue and resilient long-term profitability.

Asseco Poland Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on Asseco Poland compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming Asseco Poland's revenue will grow by 9.0% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 3.2% today to 3.7% in 3 years time.

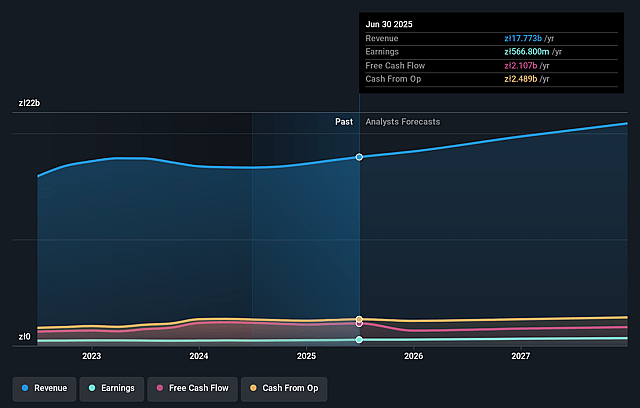

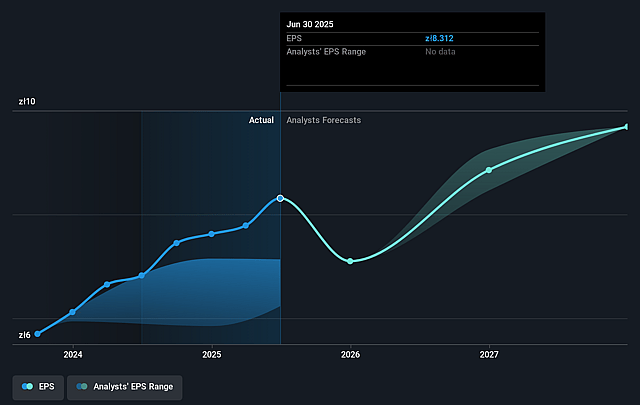

- The bullish analysts expect earnings to reach PLN 857.3 million (and earnings per share of PLN 10.16) by about September 2028, up from PLN 566.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 20.5x on those 2028 earnings, down from 24.3x today. This future PE is lower than the current PE for the GB Software industry at 21.6x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 11.87%, as per the Simply Wall St company report.

Asseco Poland Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's reliance on public sector and banking clients in Poland and Central/Eastern Europe leaves its revenues vulnerable to reductions in government IT spending cycles, potential cuts to digitalization budgets, or banking sector consolidation, which could negatively affect future revenue streams.

- A lagging pace of innovation in highly competitive areas such as cloud-native and AI-driven products puts Asseco Poland at risk of margin compression, as customers increasingly demand these advanced solutions and global peers offer more compelling alternatives, thereby threatening both top-line growth and net margins.

- Intensifying competition from global IT services giants, such as Accenture, Capgemini, and TCS, entering Central and Eastern Europe could erode Asseco Poland's existing market share in core verticals, resulting in downward pressure on revenues and potentially lower earnings.

- The growing popularity of no-code and low-code software platforms may reduce demand for Asseco Poland's custom enterprise software solutions, a major revenue source, leading to a structural decline in both revenue and earnings over time.

- Increasing regulatory complexity, greater cybersecurity threats, and market shifts toward SaaS models are likely to necessitate significant compliance and R&D investments, putting pressure on operating margins and potentially requiring upfront capital expenditures that may suppress near-term earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for Asseco Poland is PLN185.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Asseco Poland's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of PLN185.0, and the most bearish reporting a price target of just PLN89.12.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be PLN23.0 billion, earnings will come to PLN857.3 million, and it would be trading on a PE ratio of 20.5x, assuming you use a discount rate of 11.9%.

- Given the current share price of PLN201.8, the bullish analyst price target of PLN185.0 is 9.1% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on Asseco Poland?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.