Key Takeaways

- Overcapacity, rapid renewables rollout, and weak demand threaten Aboitiz Power's generation revenues and increase earnings volatility.

- Heavy investments in fossil fuels and slow transition to renewables expose the company to regulatory, financial, and stranded asset risks.

- Aggressive long-term contracting, expansion in renewables, and improved operational efficiency position Aboitiz Power for stable revenues, margin growth, and stronger earnings outlook.

Catalysts

About Aboitiz Power- Through its subsidiaries, engages in the power generation and distribution, and electricity retail businesses in the Philippines.

- Excess new generation capacity coming online in Luzon, along with an accelerated buildout of renewable plants and increased adoption of distributed solar, is expected to drive persistent oversupply and depress spot market prices, which will significantly erode Aboitiz Power's generation revenues well into the future.

- Heavy ongoing investments in both coal and gas assets leave Aboitiz Power exposed to rising regulatory restrictions and higher financing costs as local and global pressure mounts to divest from fossil fuels, a dynamic likely to further compress margins and weigh on future net income.

- The company's slow pace in shifting from legacy thermal assets to renewables relative to global peers risks stranded asset write-downs and the loss of government incentives, ultimately dragging down long-term earnings growth and return on equity.

- Concentration in the Philippine power market means Aboitiz Power is heavily exposed to local regulatory policy risks and macroeconomic slowdowns-continued weak demand, as observed in the latest quarter, amplifies revenue volatility and threatens cash flow stability.

- Execution risk in deploying large-scale renewable and storage projects remains high, with potential for cost overruns and delays as grid constraints or interconnection bottlenecks worsen nationwide, further capping capacity additions, growth prospects, and long-run profitability.

Aboitiz Power Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Aboitiz Power compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Aboitiz Power's revenue will grow by 5.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 15.7% today to 12.5% in 3 years time.

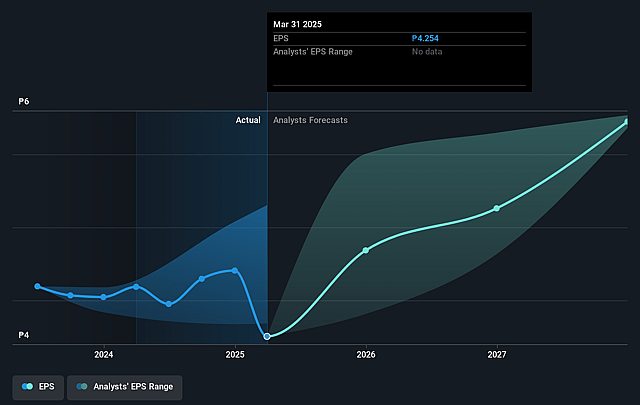

- The bearish analysts expect earnings to reach ₱27.7 billion (and earnings per share of ₱3.84) by about September 2028, down from ₱29.4 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 12.4x on those 2028 earnings, up from 10.8x today. This future PE is greater than the current PE for the PH Renewable Energy industry at 8.0x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.22%, as per the Simply Wall St company report.

Aboitiz Power Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- AboitizPower is aggressively contracting its generation portfolio, with expectations to have around 90% of baseload capacity locked in through long-term bilateral contracts by year-end, which should stabilize revenues and reduce earnings volatility associated with low spot prices.

- Large-scale investments in renewable energy and battery storage, with 421 megawatts of renewables under construction and new hybrid battery projects, position the company to benefit from the country's transition to clean energy and capture long-term demand growth, thereby supporting future earnings and improving margins.

- Continued growth in electricity demand, evidenced by a 9% year-on-year increase in energy sold and expanding distribution utility volumes, highlights a secular trend of electrification and industrialization in the Philippines, which is likely to drive top-line revenue growth over time.

- The Chromite Gas Holdings acquisition and new gas plants are already contributing to net profit and EBITDA, while improved plant availability in the coal fleet from 70% to 90% between the first and second quarters enhances operational efficiency and helps to support gross profit margins.

- Management is confident about near-term improvements in earnings, citing the ramp-up of new contracts with higher margins, full operations of new gas units, and the transition of ASPA contracts to higher approved rates-all of which are set to lift net income in the second half of the year.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Aboitiz Power is ₱32.06, which represents two standard deviations below the consensus price target of ₱45.54. This valuation is based on what can be assumed as the expectations of Aboitiz Power's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₱54.3, and the most bearish reporting a price target of just ₱31.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ₱221.9 billion, earnings will come to ₱27.7 billion, and it would be trading on a PE ratio of 12.4x, assuming you use a discount rate of 14.2%.

- Given the current share price of ₱44.0, the bearish analyst price target of ₱32.06 is 37.2% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.