Key Takeaways

- Intensifying geopolitical tensions, regulatory demands, and increased competition are heightening risks to Nordic's supply chain, profitability, and market share in core segments.

- Dependence on key customers and prolonged product cycles increase vulnerability to revenue volatility, earnings stagnation, and weakened operating leverage.

- Strong product innovation, strategic diversification, and disciplined cost management position Nordic Semiconductor for sustained growth and profitability amid expanding IoT and wireless technology markets.

Catalysts

About Nordic Semiconductor- A fabless semiconductor company, develops and sells integrated circuits for use in short- and long- range wireless applications in Europe, the Americas, and the Asia Pacific.

- The growing risk of geopolitical tensions and new trade barriers between the US, China, and Europe threatens to disrupt Nordic Semiconductor's global supply chain and directly limit addressable markets, creating high uncertainty around long-term revenue sustainability and potentially leading to loss of top-line growth momentum.

- Escalating regulatory and ESG requirements are expected to increase operational costs and complexity, with mounting compliance burdens likely to erode net margins and reduce overall profitability over the coming years, especially as the company emphasizes sustainability leadership and faces higher reporting and audit standards.

- Rising competition from Asian manufacturers in wireless chips and microcontrollers is expected to result in persistent pricing pressure, undermining Nordic's market share in core segments and squeezing gross margins, which may ultimately lead to margin compression and lower earnings quality.

- Nordic's concentration of revenue among a few high-volume customers, particularly in industrial and healthcare sectors, exposes the company to significant volatility if key customers reduce orders or switch to alternative suppliers, thus threatening both revenue stability and predictability of cash flows in future periods.

- Continued heavy investment in research and development, coupled with the risk of prolonged product transition cycles-such as the nRF54 ramp-heightens the possibility of delays in realizing new revenue streams, leaving Nordic vulnerable to stagnating earnings and reduced operating leverage, especially if new product launches fail to gain timely traction or market standards fragment.

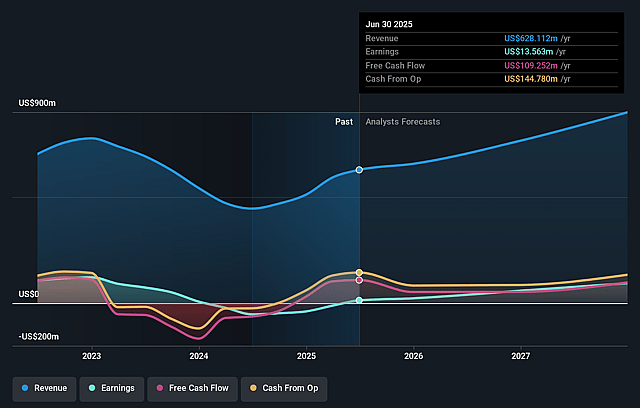

Nordic Semiconductor Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Nordic Semiconductor compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Nordic Semiconductor's revenue will grow by 10.2% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 2.2% today to 10.0% in 3 years time.

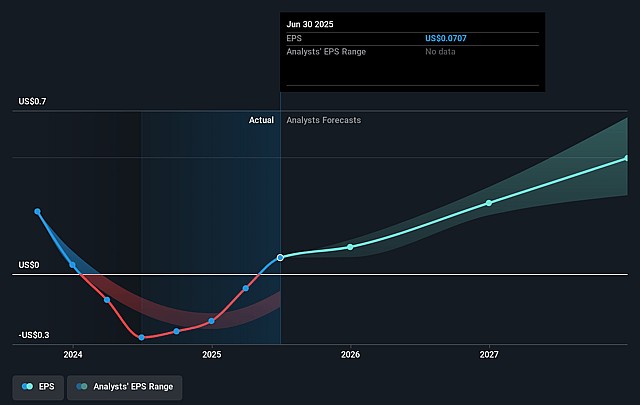

- The bearish analysts expect earnings to reach $83.7 million (and earnings per share of $0.43) by about September 2028, up from $13.6 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 31.6x on those 2028 earnings, down from 219.0x today. This future PE is lower than the current PE for the GB Semiconductor industry at 215.7x.

- Analysts expect the number of shares outstanding to decline by 0.67% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.36%, as per the Simply Wall St company report.

Nordic Semiconductor Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The strong 28 percent year-on-year revenue growth and continued guidance for quarterly revenue increases, including expectation for meaningful revenue acceleration from new products starting in 2026, suggest top-line expansion could continue, contradicting expectations for declining revenues.

- Nordic Semiconductor's leadership in Bluetooth Low Energy design certifications and the successful launch of the advanced nRF54 series, backed by robust design activity and expanding customer pipeline, indicate that market share and product volume could grow, supporting higher long-term earnings.

- Strategic expansion into software, cloud services, and AI solutions through the Memfault and Neuton.AI acquisitions diversifies the business and adds recurring revenue streams, which may enhance gross margins and provide resilience to profit levels over time.

- The company's commitment to cost control, operational efficiency, and targeted flat operating expenditures, even during growth in sales and product introductions, shows a disciplined path toward higher EBITDA margins, supporting improved net margins in the long run.

- Broad secular industry tailwinds-including increasing energy efficiency demands, IoT proliferation across consumer, industrial, and healthcare sectors, and the roll-out of advanced wireless standards-position Nordic to benefit from expanding addressable markets, which could drive sustained revenue and earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Nordic Semiconductor is NOK109.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Nordic Semiconductor's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of NOK190.0, and the most bearish reporting a price target of just NOK109.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $840.0 million, earnings will come to $83.7 million, and it would be trading on a PE ratio of 31.6x, assuming you use a discount rate of 9.4%.

- Given the current share price of NOK156.8, the bearish analyst price target of NOK109.0 is 43.9% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.