Key Takeaways

- Slower digital transformation and increased fintech competition threaten customer retention, revenue growth, and margins in core banking operations.

- High exposure to domestic real estate and shifting demographics increase credit risk and constrain future growth in lending and deposits.

- Diversified growth strategies, disciplined risk and cost management, and enhanced shareholder returns position Hana Financial Group for sustained profitability amid evolving market conditions.

Catalysts

About Hana Financial Group- Through its subsidiaries, provides financial services in South Korea.

- Intensifying digital disruption and rapid growth of agile fintech competitors threaten Hana Financial Group's ability to sustain its traditional banking revenue, as slower digital transformation relative to peers could undermine medium

- to long-term customer acquisition and retention, compressing both revenue and net margins.

- South Korea's aging and shrinking workforce is set to reduce overall loan demand and the retail savings pool, which heavily constrains future revenue growth potential for both household lending and deposit-related businesses.

- The group's persistent overexposure to the highly leveraged domestic real estate market leaves its balance sheet vulnerable to an eventual property correction, heightening risk of sharp increases in non-performing loans, deteriorating asset quality, and ultimately higher credit costs that could erode net profits.

- Mounting geopolitical risks and global economic decoupling-particularly increased uncertainty related to China and regional trade-are likely to dampen the growth of Hana's cross-border operations, exposing international earnings streams to currency volatility and elevated risk premiums, which would weigh on consolidated revenues.

- Ongoing structural decline in branch profitability due to widespread digital adoption, combined with rising regulatory compliance costs and increasingly stringent capital requirements, will constrain operating leverage and force higher SG&A expenses, negatively impacting earnings and return on equity.

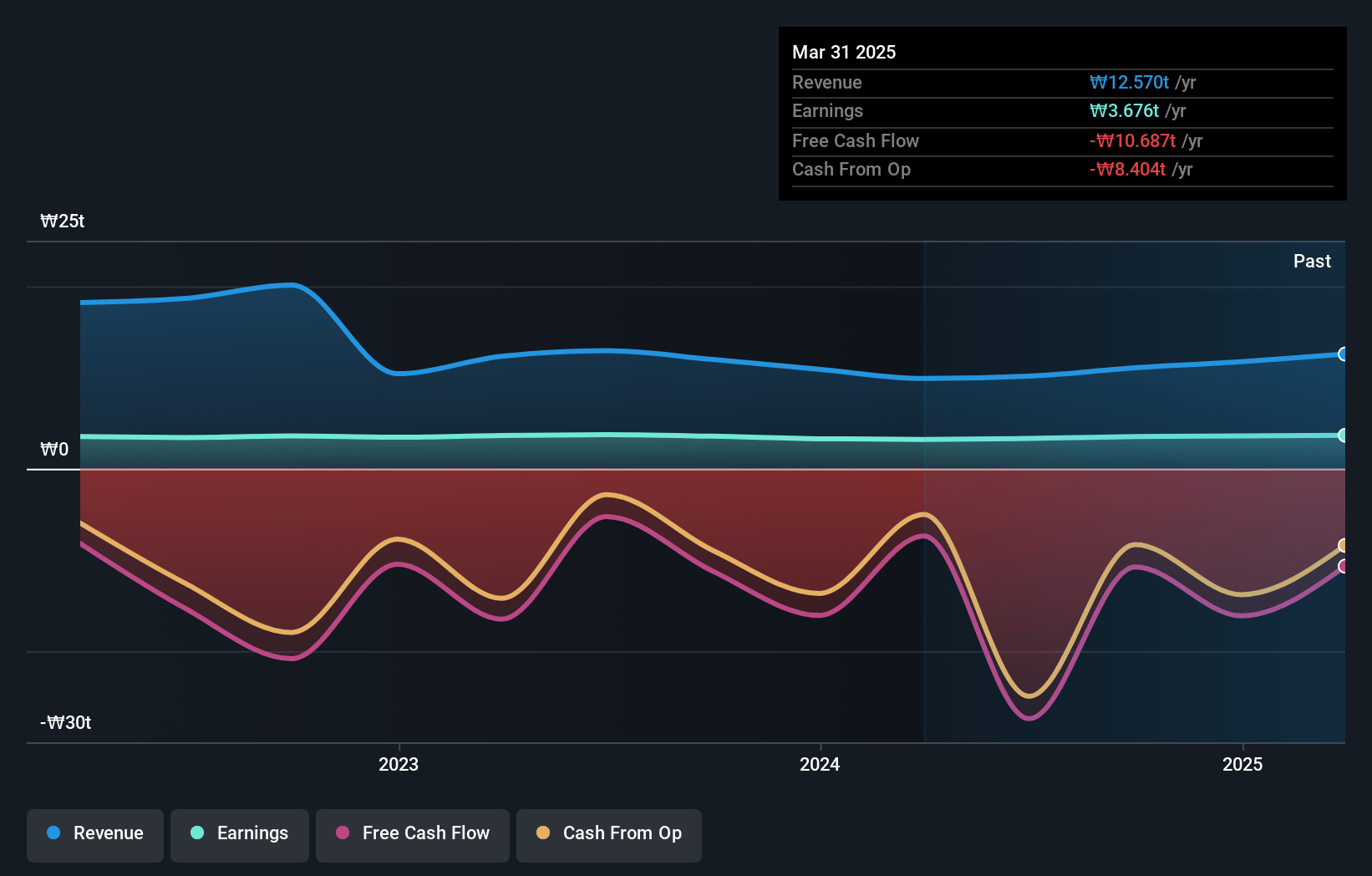

Hana Financial Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Hana Financial Group compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Hana Financial Group's revenue will decrease by 5.3% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 29.2% today to 38.0% in 3 years time.

- The bearish analysts expect earnings to reach ₩4052.8 billion (and earnings per share of ₩14665.53) by about July 2028, up from ₩3675.7 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 5.3x on those 2028 earnings, down from 6.7x today. This future PE is lower than the current PE for the KR Banks industry at 7.5x.

- Analysts expect the number of shares outstanding to decline by 1.79% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.19%, as per the Simply Wall St company report.

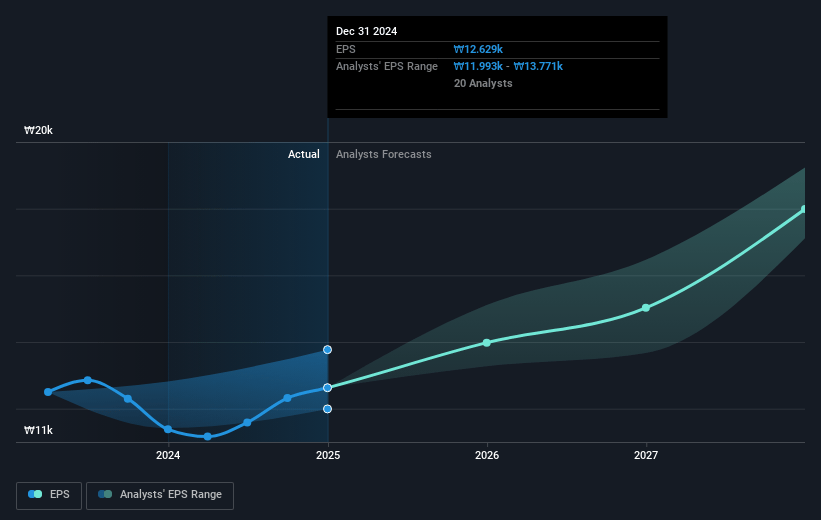

Hana Financial Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Resilient growth in core earnings, including a 9.1 percent year-over-year increase in net income and strong fee and interest income, indicates that Hana Financial Group is effectively navigating market challenges, supporting sustained profit growth and revenue expansion.

- Proactive capital management, such as ongoing share buybacks and a fixed annual dividend of ₩1 trillion with plans for gradual increases, provides strong shareholder returns and enhances earnings per share growth over time.

- Strategic focus on high-quality, collateral-backed loan growth-as well as robust risk management and provisioning-has resulted in stable credit costs and asset quality, mitigating risk to net margins and supporting longer-term financial performance.

- Steady overseas expansion, especially in Asia, and the strengthening of nonbanking businesses such as securities and wealth management, are diversifying profit streams and tapping into higher growth markets, boosting consolidated revenue and reducing reliance on domestic lending.

- Persistent cost control efforts, as seen in reduced recurring G&A expenses and ongoing operational efficiency measures, are improving the group's cost-to-income ratio, providing additional upside to net profits and supporting margin resilience in the long run.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Hana Financial Group is ₩65500.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Hana Financial Group's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₩133000.0, and the most bearish reporting a price target of just ₩65500.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ₩10678.4 billion, earnings will come to ₩4052.8 billion, and it would be trading on a PE ratio of 5.3x, assuming you use a discount rate of 8.2%.

- Given the current share price of ₩90800.0, the bearish analyst price target of ₩65500.0 is 38.6% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.