Key Takeaways

- Aggressive EV policy shifts and electrification of public transport threaten core CNG demand, putting long-term sales growth and revenue expansion at risk.

- Margin pressure is heightened by volatile gas sourcing, rising competition, and expanding regulatory scrutiny, weakening earnings resilience and shareholder returns.

- Strong demand, expanding customer base, diversified energy initiatives, and effective risk management position the company for sustained growth, improved margins, and long-term financial stability.

Catalysts

About Indraprastha Gas- Engages in the distribution and sale of natural gas in India.

- Intensifying policy headwinds and electrification of public transport in Delhi, including the decision by the Delhi Transport Department to make all new DTC buses electric and policy drafts considering a ban on petrol and CNG vehicles, signal a structural decline in long-term demand for CNG, threatening Indraprastha Gas's core revenue base and future volume growth.

- Growing adoption of electric vehicles, supported by aggressive government policy shifts toward net-zero carbon targets, will accelerate erosion of CNG's addressable market, leading to persistent stagnation or contraction in core CNG sales and sustained pressure on sales volumes.

- The saturation of the Delhi-NCR market, combined with weak growth in CNG sales despite substantial new vehicle additions, implies limited incremental growth potential and an impending slowdown in revenue expansion, exacerbated by ongoing EV penetration.

- Natural gas sourcing volatility and higher reliance on RLNG contracts, coupled with escalating global price risks, introduce margin uncertainty and increase cost of goods sold, reducing EBITDA margins and earnings resilience over the long term.

- Rising competition from new entrants in recently awarded geographies, along with the possibility of further regulatory scrutiny or price controls, will force higher capital expenditures and likely compress net margins, undermining normalized return on capital employed and shareholder returns.

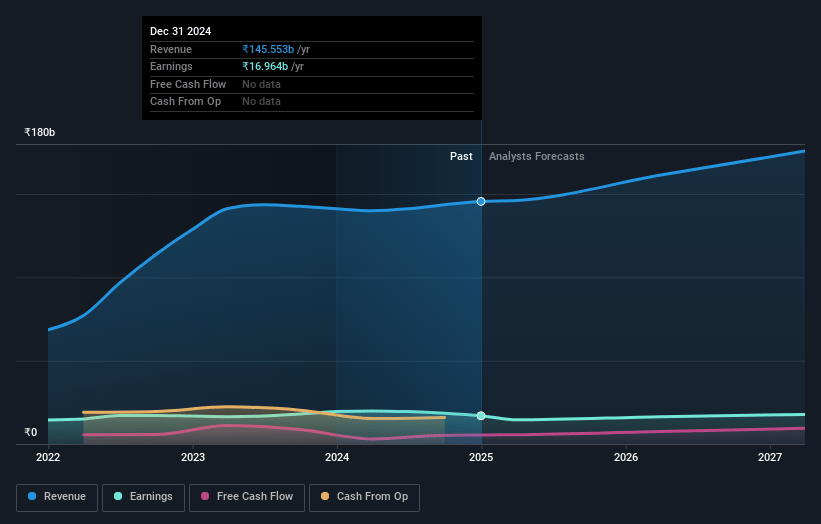

Indraprastha Gas Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Indraprastha Gas compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Indraprastha Gas's revenue will grow by 1.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will shrink from 11.5% today to 7.7% in 3 years time.

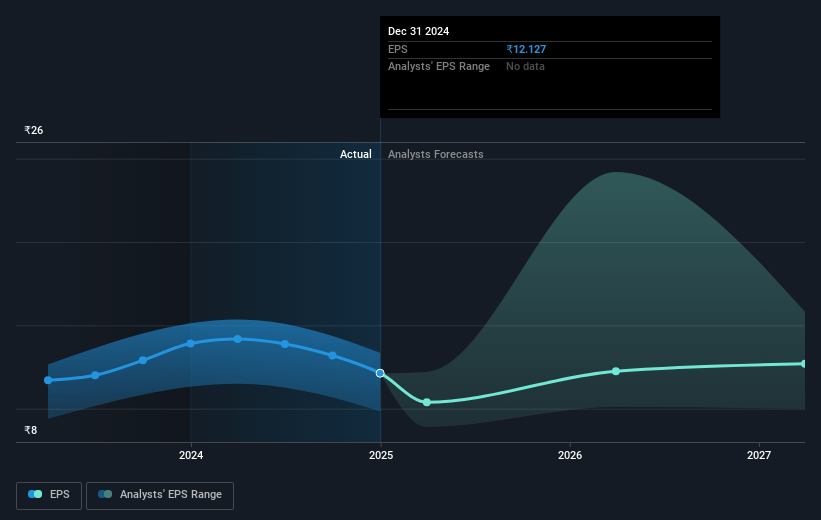

- The bearish analysts expect earnings to reach ₹12.0 billion (and earnings per share of ₹8.56) by about July 2028, down from ₹17.2 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 23.9x on those 2028 earnings, up from 17.1x today. This future PE is greater than the current PE for the IN Gas Utilities industry at 17.1x.

- Analysts expect the number of shares outstanding to decline by 0.06% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.55%, as per the Simply Wall St company report.

Indraprastha Gas Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Sustained double-digit growth in key segments such as domestic PNG, commercial, and industrial sales, as well as robust CNG vehicle additions, indicate a strong long-term demand profile that could drive continued revenue and earnings growth.

- Aggressive expansion into new geographical areas, where sales volumes are rising rapidly (up to 30%+ in some GAs), is increasing the company's customer footprint and points to sustained volume and revenue growth that will support future financial performance.

- The company's significant planned capital expenditure for network expansion and core business (₹1,300 crores annually for several years), along with scaling up CNG stations and connections, suggests increased operating leverage and improved margins over the medium to long term.

- Diversification initiatives including a large solar project, investments in biogas, and partnerships on LNG and CBG will provide new revenue streams and help mitigate margin compression from pure-play gas distribution, thereby improving long-term stability in operating profit.

- Management's ability to secure term gas sourcing contracts, manage volatility in gas allocation, and maintain a balanced portfolio (with 65% Henry Hub linkage) reduces risks from price shocks and enhances margin stability, supporting steady growth in net profits and returns on capital employed.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Indraprastha Gas is ₹144.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Indraprastha Gas's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹648.0, and the most bearish reporting a price target of just ₹144.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ₹155.7 billion, earnings will come to ₹12.0 billion, and it would be trading on a PE ratio of 23.9x, assuming you use a discount rate of 12.5%.

- Given the current share price of ₹210.39, the bearish analyst price target of ₹144.0 is 46.1% lower.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.