Last Update 02 Jul 26

Fair value Decreased 26%LTM: Sector Tailwinds And Earnings Momentum Will Face Slower Traffic Risks

Analysts have trimmed the Latam Airlines price target to ₹3,285 from ₹4,438 as they factor in slightly lower assumed revenue growth and a more conservative future P/E, while still pointing to improving sector conditions, lighter balance sheets and earnings momentum highlighted in recent research.

Analyst Commentary

Recent Street research on Latam Airlines, or LTM, reflects a mix of optimism about sector conditions and reservations about how sustainable earnings momentum and valuation might be, especially if macro or industry trends turn less supportive. For you as an investor, the key is to separate what is tied to shorter term geopolitical and fuel price shifts from what is tied to the company’s own execution and balance sheet strength.

On the constructive side, coverage initiations have pointed to improving sector conditions, LTM’s lighter balance sheet and earnings momentum, as well as expectations that air travel penetration in Latin America could continue to build over time. Some research also flags a relatively supportive competitive backdrop, with a focus on more rational industry behavior. JPMorgan, for example, has expressed a preference for Latam Airlines over some regional peers and has framed its stance around these company specific factors rather than just broad sector moves.

At the same time, several reports temper that optimism by calling out softer economic growth across Latin America and the potential for traffic to cool, even as near term conditions look better following geopolitical de escalation. This is where the recent trimming of the LTM price target stands out, as it folds in lower assumed revenue growth and a more conservative future P/E. This suggests that some of the earlier enthusiasm in the stock’s valuation may have gone too far relative to execution and growth risks.

For readers tracking Latam Airlines, the overall research tone can be read as cautiously constructive, with upside arguments now more clearly balanced against questions about how the company might perform if macro tailwinds fade or if competition becomes more aggressive again. The takeaway is less about a single headline rating and more about how analysts are fine tuning assumptions around revenue, margins and what multiple they are willing to pay for that profile.

Bearish Takeaways

- Bearish analysts are building in slower revenue assumptions for Latam Airlines, which reduces their justified P/E and helps explain why the latest price target has been cut despite references to improving sector conditions.

- Concerns about sluggish economic growth in Latin America feed into cautious traffic expectations, which in turn introduce risk to LTM’s growth profile if demand softens more than current base case assumptions.

- The move to a more conservative valuation framework, including a lower future P/E, highlights skepticism about how durable current earnings momentum will be and whether the stock’s prior multiples fully reflected execution risks.

- Some research frames the sector as sensitive to geopolitical developments and fuel price trends, which can pressure margins and make it harder for Latam Airlines to consistently hit earnings targets even with a lighter balance sheet.

What’s in the News for LTM

- LTM has scheduled a board meeting on July 11, 2026 to review unaudited standalone and consolidated financial results for the quarter ended June 30, 2026 and to consider other business matters. (Source: Company board meeting notice)

- LTM announced it has joined Athena, an industry coalition led by Chainguard focused on protecting open source software from AI driven vulnerabilities, signaling continued attention to cybersecurity and software supply chain resilience for enterprise clients. (Source: Company client announcement)

- LTM launched BlueVerse for Databricks, combining its BlueVerse AI ecosystem with the Databricks platform to support AI driven data monetization and pre built industry solutions across sectors such as manufacturing, banking, financial services, insurance, media & entertainment, and retail & consumer goods. (Source: Company client announcement)

- LTM introduced several BlueVerse related offerings, including BlueVerse for iRun, BlueVerse Currency, BlueVerse M.A.X, and the LTM Business Orchestration Platform, all framed as AI centered models and tools aimed at outcome based pricing, IT operations, marketing execution, and SAP centric business processes. (Source: Company product announcements)

- LTM approved a final dividend of ₹53 per equity share for the financial year 2025 to 2026 at its June 1, 2026 AGM, following an earlier board meeting that considered audited results and a dividend proposal for that year. (Source: Company dividend and board announcements)

Valuation Changes for Latam Airlines (LTM)

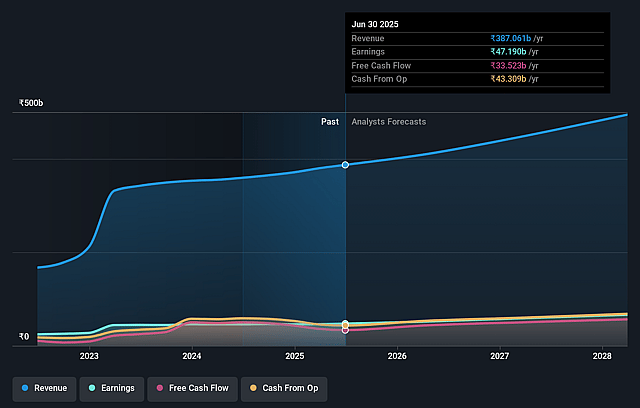

- Fair Value: trimmed from ₹4,438.40 to ₹3,285.00, a reduction of about 26%, reflecting a lower implied upside than before.

- Discount Rate: adjusted from 15.97% to 15.19%, a modest decline that slightly reduces the required return used in the analysis.

- Revenue Growth: revised from 8.61% to 7.09%, indicating more cautious assumptions for future ₹ revenue expansion at Latam Airlines.

- Net Profit Margin: kept essentially unchanged, moving fractionally from 13.22% to 13.23%, signaling a stable earnings margin view on ₹ profits.

- Future P/E: cut from 30.59x to 21.70x, a sizable step down that points to a more restrained valuation multiple for the stock.

Catalysts

About LTIMindtree

LTIMindtree is a global technology consulting and digital engineering company that delivers AI led transformation, cloud, and platform services to enterprises across industries.

What are the underlying business or industry changes driving this perspective?

- Rapid client adoption of AI driven productivity, particularly in large, long tenure accounts, risks structurally shrinking traditional effort based revenue pools faster than LTIMindtree can backfill with new AI programs. This could pressure medium term revenue growth.

- Widespread recalibration of contract pricing and scope at renewals, as clients embed AI and vendor consolidation demands, could reset commercials at lower run rate levels and cap the company’s ability to sustain recent EBIT margin expansion.

- The push to become an AI centric, agentic enterprise partner requires heavy, continuing investment in platforms like BlueVerse, studios, centers of excellence and large scale reskilling. These investments may outpace monetization and dilute net margins if win rates or ramp ups underdeliver.

- High utilization levels combined with staggered wage hikes, elevated fresher intake, and selective subcontractor use to ramp mega deals increase execution risk on complex transformations. This creates potential for cost overruns or delivery issues that could hurt earnings.

- As AI infused delivery lets clients do more with fewer people across BFSI, technology, media and other key verticals, LTIMindtree’s current headcount heavy model may face a prolonged mix shift toward lower ticket, higher automation work. This could constrain long term revenue scale and return on equity.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on LTM compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming LTM's revenue will grow by 7.1% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 11.9% today to 13.2% in 3 years time.

- The bearish analysts expect earnings to reach ₹68.7 billion (and earnings per share of ₹230.91) by about July 2029, up from ₹50.2 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ₹87.2 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 21.7x on those 2029 earnings, up from 21.0x today. This future PE is lower than the current PE for the IN IT industry at 21.8x.

- The bearish analysts expect the number of shares outstanding to grow by 0.07% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.19%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The company is already demonstrating steady top line growth, with Q2 FY '26 revenue of USD 1.18 billion growing 4.8% year on year in dollar terms and crossing INR 10,000 crore in INR terms. If this is sustained or accelerated by strong order inflow, it could support higher future revenue and earnings than a bearish view assumes, thereby underpinning the share price.

- Structural demand for AI centric transformation appears strong and broad based, with four consecutive quarters of around USD 1.6 billion in order inflow, large wins across all five verticals, and more than 1,500 digital agents already in use. This suggests a durable long term growth engine that may drive resilient revenue and expanding EBIT margins.

- Management is executing a multi lever margin improvement program, with EBIT already at 15.9% after a 160 basis point sequential expansion and further gains targeted from AI driven productivity, pyramid correction and overhead optimization. These initiatives could lift net margins and earnings beyond conservative expectations.

- Large scale AI reskilling and capability building, evidenced by over 80,000 employees completing GenAI training, new BlueVerse studios, patents and ecosystem partnerships, positions the company to capture secular AI adoption tailwinds. This may enhance win rates, support premium pricing and strengthen long term earnings power.

- A robust balance sheet and cash generation profile, including cash and investments of about USD 1.58 billion, free cash flow to profit after tax of 72.4% and return on equity of 21.8%, plus a rising dividend, provide financial resilience. This can fund growth investments and shareholder returns, limiting downside risk to valuation and the share price.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for LTM is ₹3285.0, which represents up to two standard deviations below the consensus price target of ₹4669.51. This valuation is based on what can be assumed as the expectations of LTM's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹6217.0, and the most bearish reporting a price target of just ₹3285.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be ₹519.6 billion, earnings will come to ₹68.7 billion, and it would be trading on a PE ratio of 21.7x, assuming you use a discount rate of 15.2%.

- Given the current share price of ₹3546.7, the analyst price target of ₹3285.0 is 8.0% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on LTM?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.