Key Takeaways

- Aggressive competition and value-focused consumer preferences are constraining V.I.P. Industries' pricing power, sales volumes, and ability to shift towards premium products.

- Delayed digital transformation and rising regulatory or input costs threaten long-term profitability and market share against more agile, online-focused competitors.

- Strong brand positioning, disciplined management, and sector tailwinds are set to drive long-term growth, improved margins, and market share gains for V.I.P. Industries.

Catalysts

About V.I.P. Industries- Manufactures and retails luggage, backpacks, handbags, and accessories in India and internationally.

- The intensity of competition in the lower and value end of the luggage market, especially through e-commerce channels and aggressive discounting by new entrants, is eroding V.I.P. Industries' volume growth and pricing power. This ongoing shift toward lower-priced options is likely to weigh on both revenue and net margins in the coming quarters.

- While demand for premiumization exists, the vast majority of India's consumer base (around 80-85%) continues to prioritize value, which could limit the revenue mix shift towards higher-margin premium products for the foreseeable future and dampen margin expansion.

- The proliferation of direct-to-consumer and online-first brands, coupled with exclusive e-commerce partnerships by competitors, is increasing market fragmentation and price competition, presenting a sustained risk to V.I.P. Industries' sales volumes and overall profitability.

- Delays or underinvestment in digital and omni-channel transformation may further erode V.I.P. Industries' market share as more agile competitors outperform in modern channels, negatively impacting long-term revenue and earnings growth.

- Increased regulatory scrutiny and potential input cost pressures arising from tightening climate policies and sustainability requirements present a future risk to gross margins, as cost structures may rise without the ability to fully pass on these expenses to the value-driven end customer.

V.I.P. Industries Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming V.I.P. Industries's revenue will grow by 9.8% annually over the next 3 years.

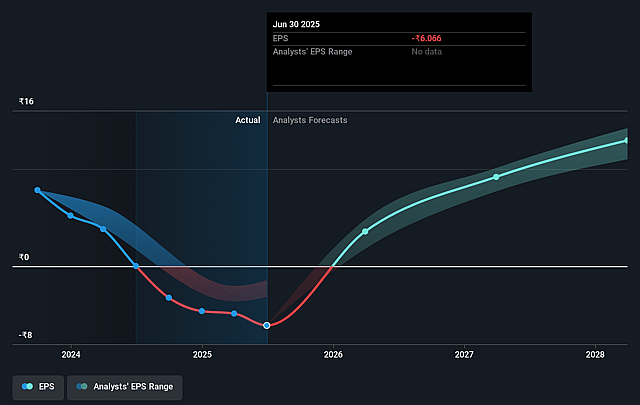

- Analysts assume that profit margins will increase from -4.1% today to 6.5% in 3 years time.

- Analysts expect earnings to reach ₹1.8 billion (and earnings per share of ₹12.71) by about September 2028, up from ₹-859.3 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting ₹2.0 billion in earnings, and the most bearish expecting ₹1.6 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 44.5x on those 2028 earnings, up from -71.5x today. This future PE is greater than the current PE for the IN Luxury industry at 24.0x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 15.71%, as per the Simply Wall St company report.

V.I.P. Industries Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Continued growth in India's travel sector and rising domestic and international travel indicate a strong secular demand for luggage products, which supports the possibility of robust revenue growth for V.I.P. Industries in the long term.

- The company's premiumization strategy is already yielding visible results, as evidenced by double-digit growth in the Carlton brand and ongoing innovation with initiatives like smart bag tags, which could drive margin expansion and improved revenue mix.

- V.I.P. Industries has demonstrated strong cost controls and operational resilience; despite double-digit revenue contraction, adjusted EBITDA margins held at 10%, and capacity utilization in Bangladesh improved significantly-potentially supporting better long-term profitability and earnings stability.

- Successful liquidation of old inventory, combined with prudent provisioning and no distress selling below cost, shows disciplined inventory management, which could prevent margin erosion and bolster net margins once short-term headwinds subside.

- The accelerating shift in the Indian luggage market from unorganized to organized players due to regulatory and market forces positions V.I.P.-a trusted household brand-to gain share and strengthen financial performance as secular trends play out, positively impacting long-term revenue and earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹370.2 for V.I.P. Industries based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹482.0, and the most bearish reporting a price target of just ₹300.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹27.8 billion, earnings will come to ₹1.8 billion, and it would be trading on a PE ratio of 44.5x, assuming you use a discount rate of 15.7%.

- Given the current share price of ₹432.55, the analyst price target of ₹370.2 is 16.8% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on V.I.P. Industries?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.