Last Update 01 Jul 26

Fair value Decreased 13%CMSINFO: Share Buyback And Major ATM Contract Will Support Future Upside

Analysts have trimmed their price target for CMS Info Systems from ₹380 to ₹330, reflecting updated assumptions around slightly different revenue growth, profit margin expectations, and a lower future P/E multiple.

What’s in the News for CMS Info Systems

- CMS Info Systems completed a share buyback program, repurchasing 4,939,126 shares, or 3% of its equity, for ₹1,679.3 million between May 14, 2026 and June 4, 2026 under the buyback announced on May 14, 2026.

- The company announced a share repurchase program to buy back up to 4,939,126 shares, representing 3% of outstanding equity, for ₹1,679.3 million at a price of ₹340 per share. The program is funded from free reserves and the securities premium account, with May 22, 2026 set as the record date and June 4, 2026 as the program end date.

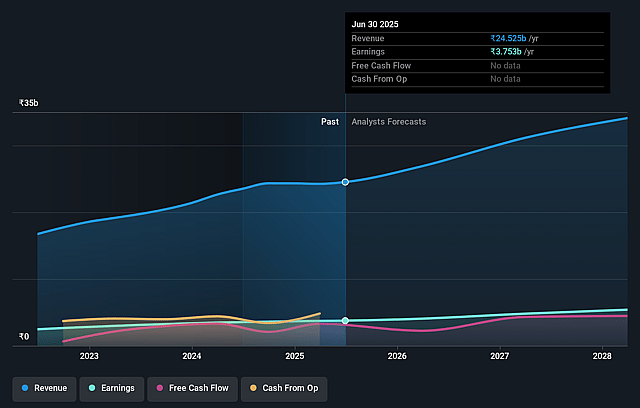

- CMS Info Systems provided earnings guidance for the 2027 financial year, targeting total revenue in the range of ₹28,000 million to ₹29,000 million, which the company stated would represent 13% to 17% growth.

- The board recommended a final dividend of ₹2.50 per equity share of face value ₹10, representing 25%, subject to shareholder approval at the 19th AGM and payable within 30 days of the AGM, if approved.

- CMS Info Systems secured a 5 year integrated ATM managed services outsourcing mandate from HDFC Bank, covering 6,000 ATMs and including services such as currency forecasting, logistics, and its Vision AI solution HAWKAI™, with the order valued at ₹4,000 million.

Valuation Changes for CMS Info Systems

- Fair Value: reduced from ₹380.0 to ₹330.0 per share, a decline of around 13% in the valuation estimate.

- Discount Rate: adjusted slightly lower from 12.79% to 12.51%, indicating a small change in the assumed required return.

- Revenue Growth: revised modestly higher from 11.34% to 11.97%, reflecting a slightly stronger growth assumption for CMS Info Systems.

- Net Profit Margin: fine tuned from 14.29% to 14.13%, implying a marginally lower profitability assumption.

- Future P/E: reduced from 18.79x to 15.63x, indicating a lower valuation multiple applied to CMS Info Systems in the updated model.

Catalysts

About CMS Info Systems

CMS Info Systems provides cash logistics, ATM management, retail cash solutions and technology led remote monitoring and surveillance services to banks, NBFCs and large retailers.

What are the underlying business or industry changes driving this perspective?

- Although the HAWKAI remote monitoring platform is scaling rapidly toward 50,000 sites and targeting 80,000 sites by FY 30, competitors can also chase the same multi‑year bank branch surveillance opportunity of over 35,000 branches. This competition could cap pricing power and dilute the uplift to long term service revenue growth.

- While banks are refreshing on site ATM and recycler networks and public sector banks are expected to outsource more bank owned ATMs, the structural shift toward digital payments could limit absolute cash usage growth. This may keep ATM volumes subdued and constrain the recovery in cash logistics revenue and EBIT margins.

- Despite a consolidating managed services provider ecosystem that should favor larger players, tighter bank credit to weaker MSPs and elongated working capital cycles highlight ongoing counterparty risk. This can keep provisions elevated and weigh on net margins and cash conversion even if top line grows.

- Although technology and AI driven route optimization, Gig delivery models and automation are intended to offset wage inflation and long term settlements, execution delays or underperformance in these programs could leave the company with a structurally higher fixed cost base. This may limit operating leverage and EBIT margin expansion.

- While the expansion into non BFSI remote monitoring for dark stores, logistics and other enterprises broadens the addressable market, high initial platform investments and customer specific solutioning may keep depreciation and overheads elevated. This could suppress earnings growth and return ratios until scale benefits fully materialize.

Assumptions

How have these above catalysts been quantified?

- This narrative explores a more pessimistic perspective on CMS Info Systems compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming CMS Info Systems's revenue will grow by 12.0% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 12.2% today to 14.1% in 3 years time.

- The bearish analysts expect earnings to reach ₹4.9 billion (and earnings per share of ₹30.94) by about July 2029, up from ₹3.0 billion today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as ₹5.5 billion.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 15.6x on those 2029 earnings, up from 15.2x today. This future PE is lower than the current PE for the IN Commercial Services industry at 21.0x.

- The bearish analysts expect the number of shares outstanding to decline by 0.06% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.51%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- The HAWKAI remote monitoring platform is scaling quickly toward 50,000 sites with a clear line of sight to 80,000 sites by FY 30 and a potential INR 3,000 crore opportunity across 35,000 bank branches, which could drive faster than expected long term growth in high margin tech services revenue and expand overall earnings.

- Industry consolidation in ATM managed services and remote monitoring, combined with tightening credit for weaker MSPs, is pushing more volumes and large, fixed price PSU and private bank contracts toward stronger players like CMS, which may structurally improve pricing discipline and raise long run revenue and net margins.

- Large multi year PSU and private bank wins, including the INR 500 crore SBI cash outsourcing contract over 10 years and multiple upcoming RFPs that could lift ATM counts back to 74,000 to 75,000, provide growing annuity style services revenue visibility that could support a sustained increase in earnings.

- Scaling of Gig delivery models, AI and machine learning driven route optimization, and automation of workflows and customer service are targeted at structurally lowering unit operating costs over time, which could restore EBIT margins to prior levels and potentially lift long term net margins above current expectations.

- Continued expansion of non BFSI remote monitoring into dark stores, logistics, NBFCs and other enterprises, supported by aggressive tech and platform investments, may diversify the business away from cyclical cash logistics and accelerate services revenue growth, leading to stronger long term earnings and higher return ratios.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bearish price target for CMS Info Systems is ₹330.0, which represents up to two standard deviations below the consensus price target of ₹362.75. This valuation is based on what can be assumed as the expectations of CMS Info Systems's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹380.0, and the most bearish reporting a price target of just ₹330.0.

- In order for you to agree with the more bearish analyst cohort, you'd need to believe that by 2029, revenues will be ₹34.9 billion, earnings will come to ₹4.9 billion, and it would be trading on a PE ratio of 15.6x, assuming you use a discount rate of 12.5%.

- Given the current share price of ₹280.4, the analyst price target of ₹330.0 is 15.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on CMS Info Systems?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.