Catalysts

About CMS Info Systems

CMS Info Systems is a leading cash management, ATM services and technology-enabled security solutions provider to banks, NBFCs and retail businesses in India.

What are the underlying business or industry changes driving this perspective?

- Rapid scale-up of the HAWKAI remote monitoring and Vision AI platform, with targets to reach 80,000 sites by FY '30 and strong traction across banks and large enterprises, is expected to meaningfully increase high-margin, annuity-like tech revenues and lift overall earnings quality.

- Large, multi-year PSU and private bank outsourcing contracts, including the INR 500 crore SBI cash RFP and upcoming RFPs covering 30,000 to 35,000 bank branches, provide long-duration revenue visibility and support double-digit services revenue growth and improving EBITDA.

- Industry consolidation in ATM managed services and MSP ecosystems, following the exit of weaker players, is driving better pricing discipline and higher fixed-price wins, which is expected to structurally enhance realizations and support PAT margin expansion.

- Rural and semi-urban cash usage, supported by white-label ATMs and a fast-growing retail cash logistics footprint with a scalable Gig operating model, is expanding the addressable market and is expected to drive steady volume growth with rising network productivity and net margins.

- Ongoing automation investments in AI, machine learning based routing and workflow bots across operations are designed to structurally lower unit operating costs, supporting a return to FY '25 PAT margin levels and stronger free cash flow conversion over time.

Assumptions

This narrative explores a more optimistic perspective on CMS Info Systems compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts. How have these above catalysts been quantified?

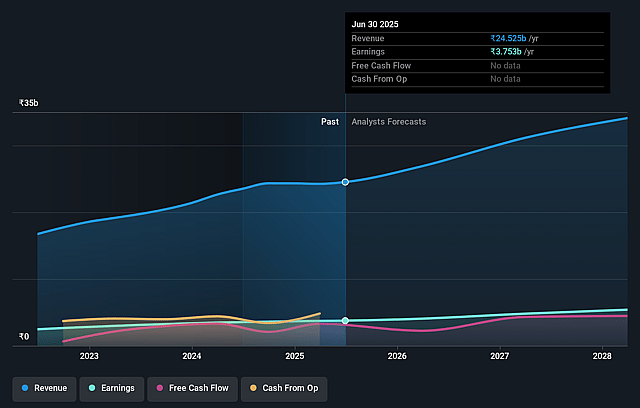

- The bullish analysts are assuming CMS Info Systems's revenue will grow by 13.1% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 14.7% today to 15.1% in 3 years time.

- The bullish analysts expect earnings to reach ₹5.3 billion (and earnings per share of ₹32.46) by about December 2028, up from ₹3.6 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 27.0x on those 2028 earnings, up from 15.9x today. This future PE is greater than the current PE for the IN Commercial Services industry at 18.7x.

- The bullish analysts expect the number of shares outstanding to grow by 0.24% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 12.79%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?

- Structural headwinds from rising digital payments could cap long term ATM and branch cash usage growth. Even with industry consolidation and new PSU tenders, the installed base and transaction intensity of ATMs may stagnate, limiting upside in cash logistics and ATM management revenue and constraining earnings growth.

- Dependence on a concentrated set of large PSU and private sector bank contracts, including SBI and ICICI Bank, means that delays in RFP closures, network rationalization or a strategic shift by banks toward in house management or more aggressive pricing could compress realizations, slowing services revenue growth and pressuring net margins.

- The HAWKAI and broader tech solutions strategy assumes sustained high growth and successful scale up across BFSI and non BFSI sectors. However, intensified competition, technological disruption or slower than expected adoption of AI led surveillance and branch monitoring could lead to underutilized platforms, lower annuity revenues and weaker return on recent CapEx, dragging on earnings.

- Working capital stress in the MSP ecosystem, elongated DSOs and elevated expected credit loss provisioning, as seen post the AGS episode, highlight a structural vulnerability in the cash and ATM value chain that could reappear in future downturns. This could lead to recurring provisions, weaker operating cash flow and reduced conversion of EBITDA to free cash flow.

- Persistent wage inflation, periodic long term settlements and the need to maintain excess network capacity during transitions, combined with large ongoing automation and technology investments, may offset productivity gains and delay the expected recovery to prior PAT margin levels. This could reduce operating leverage and limit earnings expansion.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The assumed bullish price target for CMS Info Systems is ₹605.0, which represents up to two standard deviations above the consensus price target of ₹466.0. This valuation is based on what can be assumed as the expectations of CMS Info Systems's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹605.0, and the most bearish reporting a price target of just ₹380.0.

- In order for you to agree with the more bullish analyst cohort, you'd need to believe that by 2028, revenues will be ₹35.2 billion, earnings will come to ₹5.3 billion, and it would be trading on a PE ratio of 27.0x, assuming you use a discount rate of 12.8%.

- Given the current share price of ₹344.7, the analyst price target of ₹605.0 is 43.0% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on CMS Info Systems?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.