Narratives are currently in beta

Key Takeaways

- Technological advancements and strategic expansions aim to enhance customer experience, driving operational efficiency, investment income, and earnings growth.

- Focus on granular deposits and festive demand strategies aims to stabilize costs and spur revenue growth, supporting positive net interest margins.

- Strains from industry slowdown, digital onboarding embargo, credit stress, and rising costs could pressure Kotak Mahindra Bank's margins and financial performance.

Catalysts

About Kotak Mahindra Bank- Provides a range of banking and financial services to corporate and individual customers in India.

- The acquisition of the personal loan portfolio from Standard Chartered could increase higher-yielding unsecured asset growth, impacting revenue positively as restrictions are lifted and the bank targets affluent customer segments.

- Strategic technological advancements, including a new mobile app and process automation, aim to improve customer experience and operational efficiency, which could enhance net margins by reducing costs and increasing customer retention.

- Kotak Mahindra Bank's plan to capitalize on festive season demand and anticipated government spending in sectors like commercial vehicles and rural finance is expected to spur revenue growth in the latter half of the year.

- Expansion in the asset management segment, with average AUM growth of 41% year-on-year and strategic focus on growing equity assets and SIP inflows, is poised to boost investment income and drive overall earnings growth.

- The bank's focus on securing granular deposits, including relaunching savings products and enhancing its digital current account offerings, is anticipated to stabilize funding costs and support favorable net interest margins.

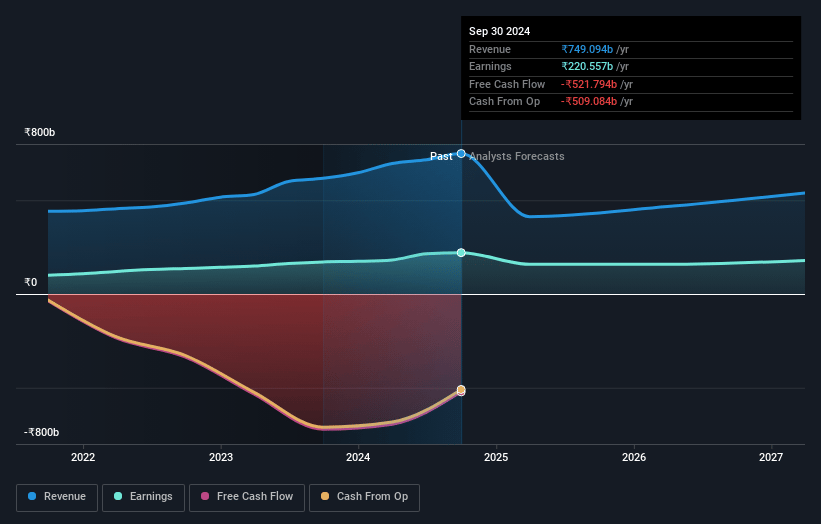

Kotak Mahindra Bank Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Kotak Mahindra Bank's revenue will decrease by -7.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 29.4% today to 33.2% in 3 years time.

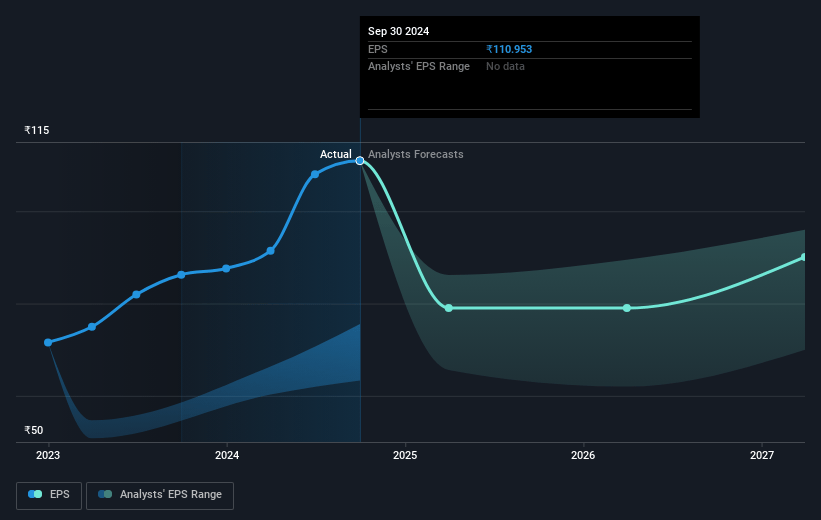

- Analysts expect earnings to reach ₹194.7 billion (and earnings per share of ₹97.98) by about January 2028, down from ₹220.6 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 30.4x on those 2028 earnings, up from 16.1x today. This future PE is greater than the current PE for the IN Banks industry at 12.4x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 14.15%, as per the Simply Wall St company report.

Kotak Mahindra Bank Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The slowdown in consumer vehicles and tractor industries affected asset growth in some business lines, risking lower revenues if the industry trends don’t improve soon.

- The embargo on digital onboarding has limited the growth in unsecured retail segments like credit cards, potentially harming net interest margins and future earnings if the situation persists.

- The banking industry is currently experiencing credit stress, particularly in the vintage segment of its credit card business and the microfinance sector, possibly leading to increased credit costs and reduced net margins.

- Rising cost of funds despite strong deposit growth could strain the bank’s net interest margin and earnings if similar trends continue.

- Potential regulatory actions and compliance requirements, especially pertaining to technology infrastructure improvement mandates from the RBI, may lead to increased operational expenses, affecting net profit margins and overall financial performance.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of ₹2000.55 for Kotak Mahindra Bank based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ₹2300.0, and the most bearish reporting a price target of just ₹1579.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be ₹586.8 billion, earnings will come to ₹194.7 billion, and it would be trading on a PE ratio of 30.4x, assuming you use a discount rate of 14.2%.

- Given the current share price of ₹1788.05, the analyst's price target of ₹2000.55 is 10.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives