Last Update01 May 25

Key Takeaways

- The Real Estate and Lifestyle segments are driving revenue growth through increased sales, product launches, and lifestyle event investments.

- Effective liability management and strategic debt restructuring are enhancing financial health and improving net margins and earnings predictability.

- Focus on affordable housing and deconsolidation impacts revenue, while limited dividend plans and FX risk reduction influence financial strategies and investor perceptions.

Catalysts

About Lippo Karawaci- Provides property development services in Indonesia.

- The Real Estate segment saw a significant increase in marketing sales to IDR 6 trillion, exceeding the initial target by 12%. Continued focus on affordable housing and new product launches could sustain revenue growth in this segment.

- The Healthcare segment, particularly Siloam, is executing a transformational plan increasing efficiency and expanding beds, which could enhance net margins and overall profitability.

- Strengthening operating cash flows and reducing interest expenses via effective liability management has improved the balance sheet's health, potentially impacting future earnings positively.

- The Lifestyle segment continues to grow, with Lippo Malls seeing a 5% increase in visitors and occupancy improvements. Investments in renovations and lifestyle events could further drive revenue and earnings.

- Efforts to reduce FX risk by eliminating U.S. dollar-denominated debt and focusing debt in local currency may enhance net margins and contribute to more predictable future earnings.

Lippo Karawaci Future Earnings and Revenue Growth

Assumptions

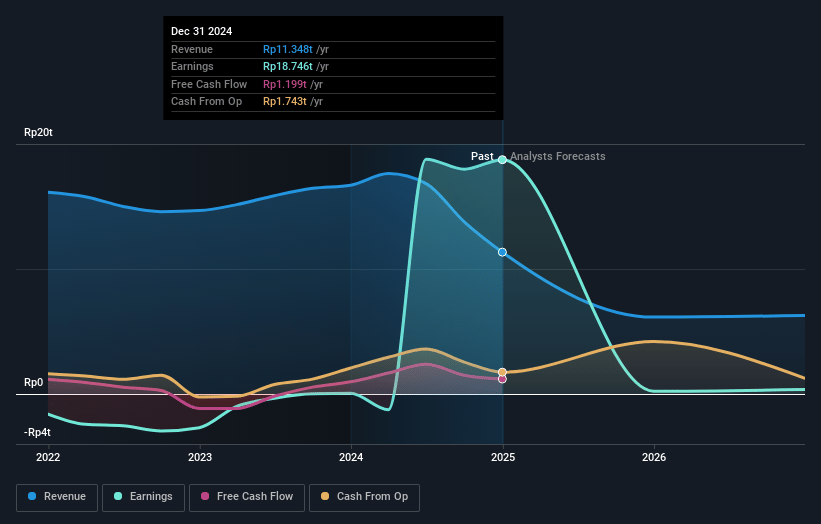

How have these above catalysts been quantified?- Analysts are assuming Lippo Karawaci's revenue will decrease by 27.8% annually over the next 3 years.

- Analysts are not forecasting that Lippo Karawaci will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Lippo Karawaci's profit margin will increase from 165.2% to the average ID Real Estate industry of 18.3% in 3 years.

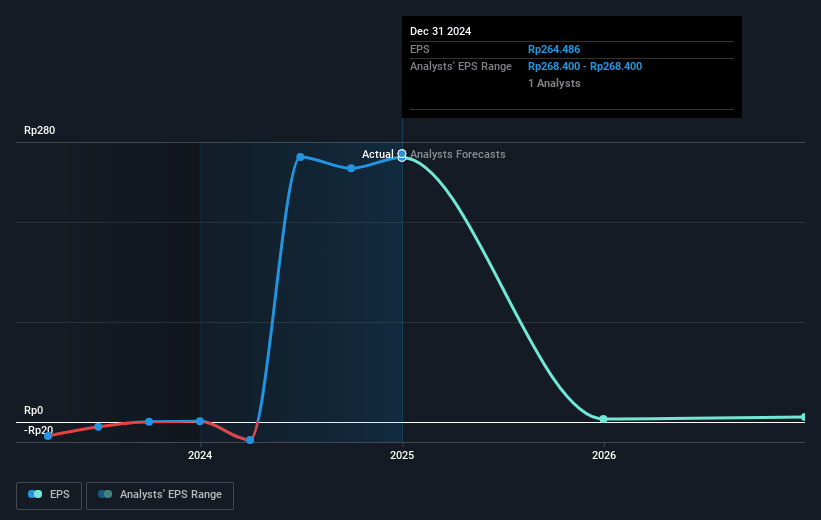

- If Lippo Karawaci's profit margin were to converge on the industry average, you could expect earnings to reach IDR 783.7 billion (and earnings per share of IDR 11.06) by about May 2028, down from IDR 18746.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 29.8x on those 2028 earnings, up from 0.3x today. This future PE is greater than the current PE for the ID Real Estate industry at 14.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 20.17%, as per the Simply Wall St company report.

Lippo Karawaci Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The deconsolidation of Siloam from Lippo Karawaci's P&L due to the partial stake sale may reduce overall revenue recognition, impacting statutory revenues from IDR 18.5 trillion to IDR 11.5 trillion.

- The company does not plan to issue dividends this year, which might affect investor sentiment and perceptions of financial stability and profitability.

- Focus on affordable housing might limit profitability margins, as these are often lower margin products, even though they attract a high volume of first-time homebuyers.

- Potential challenges in raising price points for affordable housing products without losing consumer demand could affect revenue growth projections if not managed effectively.

- The company removed U.S. dollar-denominated liabilities to minimize FX risk, but this limits the flexibility to leverage different currency bond markets unless market conditions stabilize, potentially impacting future fundraising strategies and financial cost management.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of IDR190.0 for Lippo Karawaci based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be IDR4271.2 billion, earnings will come to IDR783.7 billion, and it would be trading on a PE ratio of 29.8x, assuming you use a discount rate of 20.2%.

- Given the current share price of IDR92.0, the analyst price target of IDR190.0 is 51.6% higher. Despite analysts expecting the underlying buisness to decline, they seem to believe it's more valuable than what the market thinks.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.