Key Takeaways

- ASMPT is poised to dominate advanced packaging for memory and logic markets due to unique technology, industry relationships, and global manufacturing capabilities.

- Expansion into automation and materials, along with key partnerships, will drive margin improvement, revenue diversification, and long-term earnings resilience.

- Geopolitical uncertainty, elevated R&D spending, customer concentration, industry vertical integration, and weak end markets collectively threaten future revenue growth, margins, and profitability.

Catalysts

About ASMPT- An investment holding company, engages in the design, manufacture, and marketing of machines, tools, and materials used in the semiconductor and electronics assembly industries internationally.

- Analyst consensus focuses on expanding TCB orders with new HBM customers, but this may underestimate the scale; ASMPT is positioned to become the de facto standard for advanced HBM4 packaging, leveraging strong technical differentiation and deepening relationships with all three top global memory makers, supporting rapid revenue expansion and potential for outsized market share gains in the high-growth AI memory market.

- While analysts broadly highlight pilot production wins and technological leadership for chip-to-wafer TCB tools in logic, they underappreciate the medium-term revenue and margin uplift from becoming the process of record at leading foundries, as the industry shift to heterogeneous integration and chiplets will escalate demand for ASMPT's advanced packaging technologies in both logic and memory, opening a pathway to persistent net margin expansion above 40 percent.

- The acceleration of artificial intelligence proliferation, widespread IoT adoption, and surging edge device deployment will drive structural, multi-year growth in demand for advanced packaging and interconnect solutions-areas where ASMPT holds unique product and automation capabilities-set to drive recurring revenue growth and higher-through-cycle earnings.

- Global supply chain localization and government incentives for domestic semiconductor manufacturing are triggering a new wave of capacity buildouts; ASMPT's worldwide manufacturing footprint and flexibility enables it to capture equipment demand across every major region, boosting order backlog and providing greater visibility for long-term earnings stability and growth.

- ASMPT's expansion into high-margin automation and materials solutions, together with deepening partnerships with key OSATs and leading foundries, positions the company for improving revenue diversification, resilience through cycles, and the ability to structurally increase consolidated net margins as semiconductor packaging complexity keeps rising.

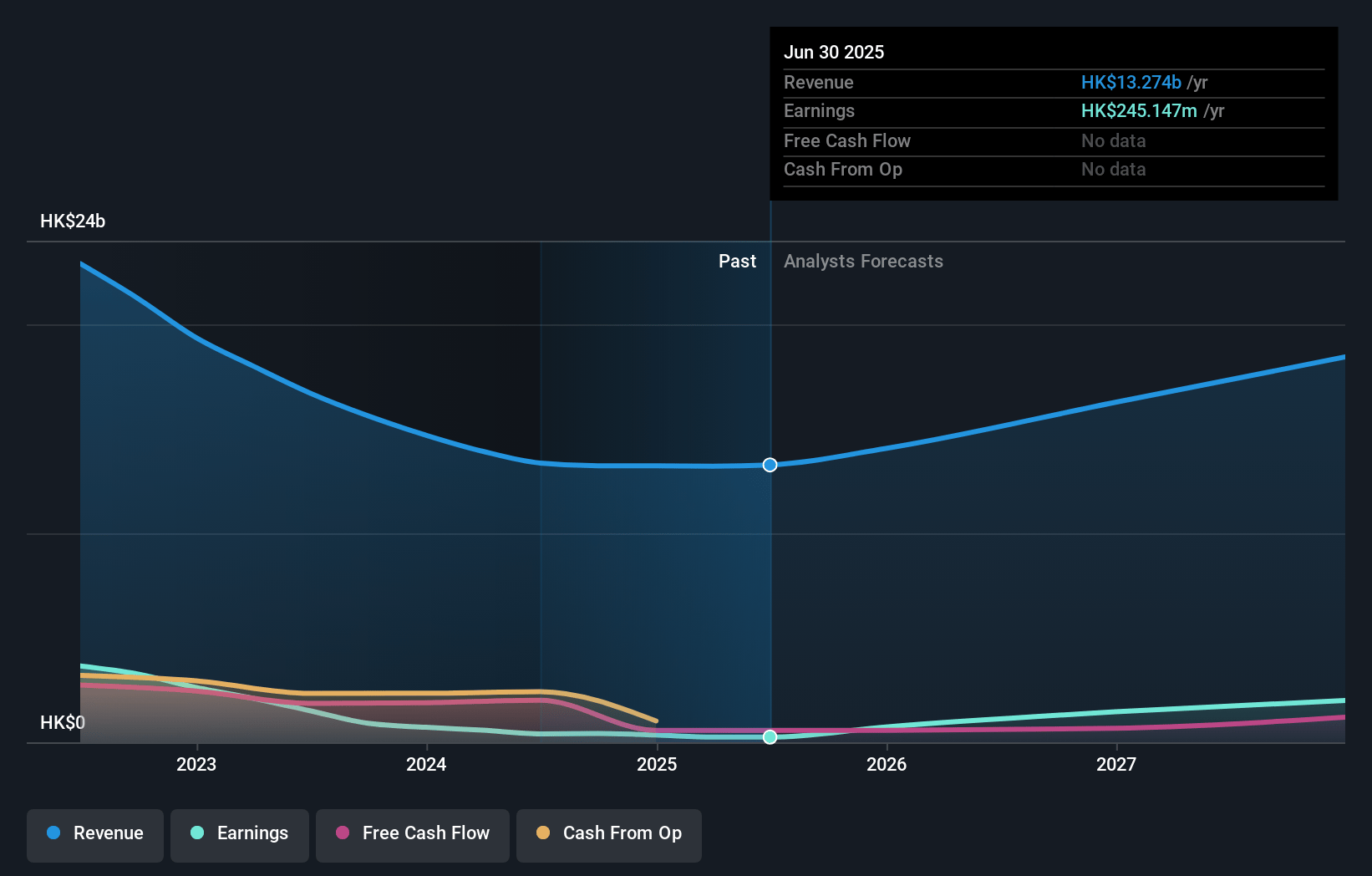

ASMPT Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on ASMPT compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

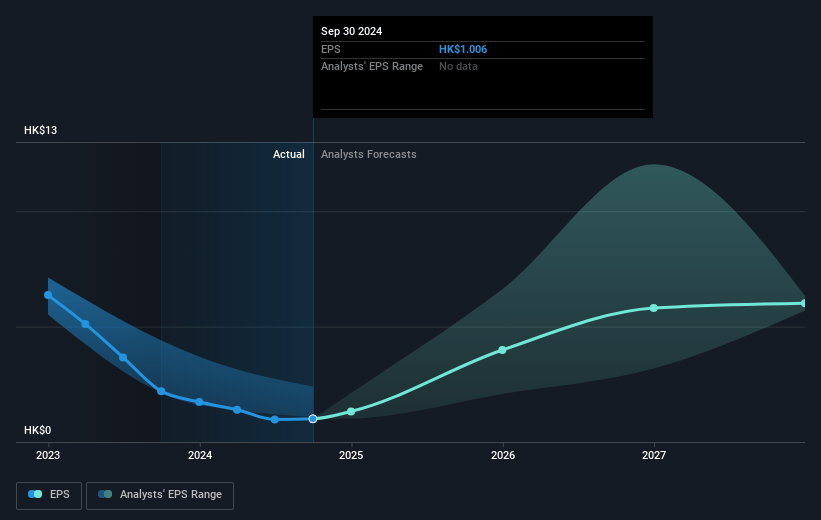

- The bullish analysts are assuming ASMPT's revenue will grow by 19.1% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 1.9% today to 15.1% in 3 years time.

- The bullish analysts expect earnings to reach HK$3.4 billion (and earnings per share of HK$8.09) by about July 2028, up from HK$249.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 16.2x on those 2028 earnings, down from 100.9x today. This future PE is lower than the current PE for the HK Semiconductor industry at 24.3x.

- Analysts expect the number of shares outstanding to grow by 0.47% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.85%, as per the Simply Wall St company report.

ASMPT Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Rising geopolitical tensions and export restrictions, particularly regarding US-China tariffs, have created indirect uncertainty for ASMPT's business, making the mainstream segment's growth trajectory difficult to forecast and potentially impacting both future revenues and overall earnings.

- Increased R&D intensity and strategic infrastructure investment, especially in developing advanced packaging and TCB tools, is materially raising operating expenses, which has already contributed to a year-on-year decline of 53 percent in adjusted net profit and poses an ongoing risk to net margins and profitability.

- Growing vertical integration by leading-edge semiconductor manufacturers and foundries, who may move packaging in-house, could limit demand for ASMPT's third-party solutions, resulting in reduced market share and potentially lower revenue in core segments.

- ASMPT's customer concentration-reliance on a handful of major memory and logic customers for bulk and repeat orders-means any reduction in volumes, delayed follow-on orders, or loss of a key account could drive significant volatility in revenue and earnings.

- Sustained softness or slow recovery in mainstream automotive and industrial end markets, combined with heightened competition from emerging Asian equipment suppliers and possible downward pricing pressure, could depress sales volumes and gross margins, particularly in the SMT segment, impacting both revenue and profitability over the long term.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for ASMPT is HK$97.72, which represents two standard deviations above the consensus price target of HK$72.52. This valuation is based on what can be assumed as the expectations of ASMPT's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of HK$100.0, and the most bearish reporting a price target of just HK$56.6.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be HK$22.3 billion, earnings will come to HK$3.4 billion, and it would be trading on a PE ratio of 16.2x, assuming you use a discount rate of 9.9%.

- Given the current share price of HK$60.35, the bullish analyst price target of HK$97.72 is 38.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.