Last Update 18 Dec 25

Fair value Increased 0.20%NG.: Dividend Outlook And Regulatory Outcomes Will Shape Returns Ahead

Analysts have modestly raised their price target on National Grid, reflecting a slightly higher fair value estimate of approximately $11.96 as they factor in stronger anticipated revenue growth, partially offset by a small compression in forecast profit margins and future valuation multiples.

Analyst Commentary

Bullish analysts view the modestly higher price target as a reflection of improving growth visibility for National Grid, particularly as regulated asset base expansion and inflation-linked mechanisms support more resilient top line progression.

At the same time, they note that the shares still trade at a discount to their assessment of long term intrinsic value, suggesting scope for further upside if execution stays on track and regulatory outcomes remain constructive.

Bullish Takeaways

- Bullish analysts highlight that stronger anticipated revenue growth, supported by ongoing network investment, can offset near term margin compression and still justify a higher fair value.

- They argue that the current valuation embeds conservative assumptions on allowed returns and regulatory risk, leaving room for multiple expansion if the policy backdrop stays stable.

- Improving visibility on capital deployment and project delivery is seen as reducing execution risk, which can support more confident long term cash flow forecasts.

- Some bullish analysts believe National Grid’s inflation protection and relatively predictable earnings profile compare favorably to broader utilities peers, warranting a tighter discount to sector averages.

Bearish Takeaways

- Bearish analysts caution that even with upgraded revenue expectations, rising operating costs and interest expense could limit earnings leverage and constrain upside to the new target.

- They remain wary that future regulatory settlements may pressure allowed returns, capping valuation multiples despite solid underlying asset growth.

- Concerns persist around execution risk on large scale capital programs, where delays or cost overruns could erode returns and weigh on investor confidence.

- Some bearish analysts argue that, after the recent rerating, the risk reward profile is more balanced, with limited room for disappointment on growth or policy outcomes without triggering downside.

What’s in the News

- Directors proposed an interim dividend of 16.35 pence per ordinary share, or $1.0657 per American Depositary Share, for the year ending 31 March 2026, payable on 13 January 2026 to shareholders on the register as of 21 November 2025 (Key Developments).

- Ex dividend dates for the 2025 to 2026 interim dividend were set for 20 November 2025 for ordinary shares and 21 November 2025 for ADRs (Key Developments).

- Earnings guidance for the six months ended 30 September 2025 indicates group performance is in line with expectations, with underlying EPS, as usual, expected to be weighted to the second half of the year (Key Developments).

- Operating profit in UK Electricity Transmission and UK Electricity Distribution is anticipated to be broadly evenly split across the year, while US regulated businesses are expected to see profits weighted to the second half, aided by fewer storms in New York and new electricity distribution rates in New England (Key Developments).

- National Grid Ventures is expected to deliver a roughly even weighting of profitability across the year (Key Developments).

Valuation Changes

- Fair Value Estimate has risen slightly from $11.93 to $11.96, reflecting a modestly higher assessed equity value.

- Discount Rate is unchanged at 7.07 percent, indicating a stable view of National Grid’s risk profile and required return.

- Revenue Growth has increased meaningfully from about 11.10 percent to roughly 12.80 percent, signalling stronger expected top line expansion.

- Net Profit Margin has fallen modestly from around 19.92 percent to about 19.24 percent, incorporating expectations of slightly higher cost pressures.

- Future P/E multiple has edged down marginally from approximately 15.34x to about 15.20x, implying a slightly more conservative valuation of future earnings.

Key Takeaways

- National Grid plans massive network investments to drive asset growth, boost future revenues, and stabilize earnings.

- Strategic initiatives like asset sales and streamlined processes support margins while enhancing earnings and operational efficiency.

- Regulatory risks, tax policy changes, rising equipment costs, supply chain constraints, and legislative delays could impact National Grid's profitability, earnings growth, and project timelines.

Catalysts

About National Grid- National Grid plc transmits and distributes electricity and gas.

- National Grid plans to invest around £60 billion in its networks over the next 5 years, which is expected to drive significant asset growth and provide strong visibility on future revenues. This is likely to positively impact future revenue streams and earnings growth.

- The company has secured new rates for its Downstate New York gas business and Massachusetts Electric business, which provides better visibility on investment plans and supports earnings stability. This regulatory clarity is likely to improve net margins and earnings.

- The ongoing £4 billion Upstate Upgrade in the U.S. and accelerated investment in the National Grid Ventures segment reflect an increase in capacity and infrastructure reliability, which should enhance future revenues.

- National Grid's strategic initiatives to secure supply chain capacities and streamline project delivery processes aim to mitigate potential delays and cost overruns, thus supporting net margins and operational efficiency.

- The planned sale of non-core assets, such as National Grid Renewables and the Grain LNG facility, is expected to unlock shareholder value, potentially leading to buybacks or debt reduction, and enhance earnings per share (EPS).

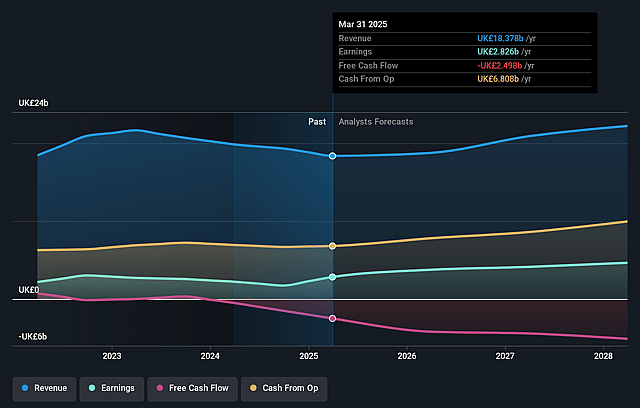

National Grid Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming National Grid's revenue will grow by 6.5% annually over the next 3 years.

- Analysts assume that profit margins will increase from 15.4% today to 21.0% in 3 years time.

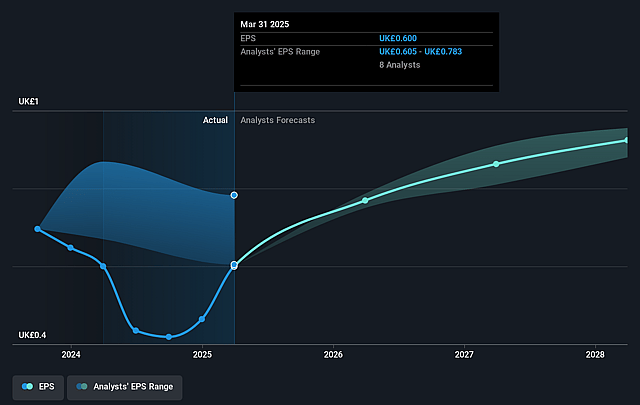

- Analysts expect earnings to reach £4.7 billion (and earnings per share of £0.92) by about September 2028, up from £2.8 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 18.7x on those 2028 earnings, up from 17.9x today. This future PE is greater than the current PE for the GB Integrated Utilities industry at 18.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.82%, as per the Simply Wall St company report.

National Grid Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Regulatory risks associated with the RIIO-T3 process could impact National Grid's allowed returns. If returns are set at the lower end of the expected range, it could affect earnings growth. Additionally, changes in the associated incentive mechanisms could further impact profitability.

- Potential changes in U.S. tax policy could affect National Grid's financial performance. Although changes in tax rates are often passed through to customers, adjustments could create cash-flow and earnings volatility.

- Rising equipment costs, such as for transformers and HVDC systems, due to increased demand could affect National Grid's capital expenditure efficiency and lead to higher costs than anticipated, which might impact net margins if such costs cannot be fully recovered.

- There is a risk of supply chain constraints and delays, especially with securing critical materials and equipment for capital projects. This could delay project timelines, impact CapEx deployment, and subsequently affect revenue growth and earnings.

- Several projects depend on favorable planning and legislative reforms. Any delays in reforms, such as fast-track consenting in the U.K., could impact infrastructure project timelines, hindering the ability to meet investment targets, affecting future earnings growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £11.781 for National Grid based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be £22.2 billion, earnings will come to £4.7 billion, and it would be trading on a PE ratio of 18.7x, assuming you use a discount rate of 6.8%.

- Given the current share price of £10.18, the analyst price target of £11.78 is 13.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on National Grid?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.