Last Update 17 Jun 26

AOM: Stable Revenue And Margin Outlook Will Support Continued Share Re Rating

Analysts have kept their £3.17 price target for ActiveOps unchanged, citing steady assumptions on fair value, revenue growth, profit margin and future P/E that together support a broadly consistent outlook for the stock.

What’s in the News for ActiveOps

- No recent ActiveOps news, periodical coverage or key developments were provided in the supplied sources, so there are currently no specific events to highlight for investors.

- In the absence of new disclosures, the unchanged £3.17 price target for ActiveOps currently reflects the latest available analyst assumptions on fair value, revenue, profit margin and future P/E.

- Investors reviewing ActiveOps stock may wish to monitor upcoming company announcements, regulatory filings and earnings releases for fresh information that could update this view.

Valuation Changes for ActiveOps

- Fair Value: The £3.17 fair value estimate for ActiveOps is unchanged. This indicates a consistent view of the stock’s central valuation reference point.

- Discount Rate: The discount rate used in the model has risen slightly from 8.97% to 9.05%. This implies a marginally higher required return in the assessment of future cash flows.

- Revenue Growth: The assumed revenue growth rate remains effectively stable at around 15.89%, with only a negligible numerical adjustment in the latest model.

- Net Profit Margin: The profit margin assumption is also effectively unchanged at about 6.49%. This reflects a consistent view on expected profitability for ActiveOps.

- Future P/E: The future P/E assumption has risen slightly from 78.0x to 78.1x. This indicates a very small adjustment to the earnings multiple applied in the valuation.

Key Takeaways

- ActiveOps can capitalize on AI demand for decision intelligence tools and significant ARR growth potential from existing clients like Fidelity International.

- New sales hires and the transition to enhanced platforms suggest increased market reach and improved margins from upselling and cross-selling.

- Reliance on a major customer and direct sales alongside marketing expenditures pose revenue and scalability risks, impacting revenue stability and net margins.

Catalysts

About ActiveOps- Engages in the provision of hosted operations management software as a service solution to industries in Europe, the Middle East, India, Africa, North America, and Asia Pacific.

- ActiveOps is well-positioned to capitalize on the growing demand for AI-driven operational solutions, which could significantly drive revenue growth as organizations seek better decision intelligence tools.

- The company's land and expand strategy, particularly with high-profile clients like Fidelity International, indicates potential for substantial ARR growth within existing accounts, directly impacting revenue projections.

- Ongoing investments in new sales channel capacity, with 5 new sales hires and more expected, suggest a potential increase in market reach and customer acquisition, positively affecting future revenue.

- The transition to the new ControliQ platform and the upcoming Series 4 release enables ActiveOps to upsell and cross-sell enhanced products, likely improving net margins as these products carry higher gross margins.

- ActiveOps has identified significant untapped ARR potential from its existing customer base, estimated at £90 million, which could drive long-term revenue growth without needing extensive new customer acquisition efforts.

ActiveOps Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?

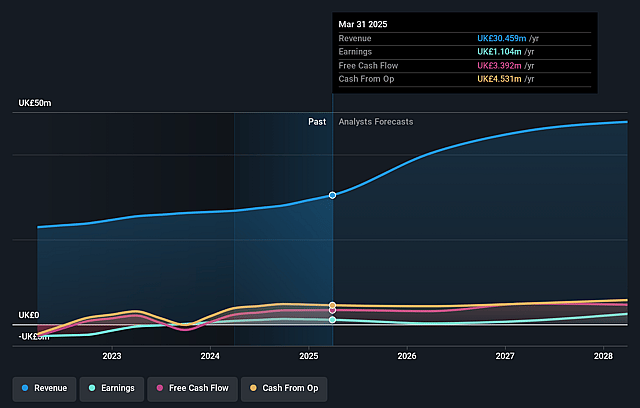

- Analysts are assuming ActiveOps's revenue will grow by 15.9% annually over the next 3 years.

- Analysts assume that profit margins will increase from -0.5% today to 6.5% in 3 years time.

- Analysts expect earnings to reach £3.7 million (and earnings per share of £0.02) by about June 2029, up from -£203.0 thousand today.

- In order for the above numbers to justify the price target of the analysts, the company would need to trade at a PE ratio of 78.6x on those 2029 earnings, up from -913.4x today. This future PE is greater than the current PE for the GB Software industry at 20.3x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 9.05%, as per the Simply Wall St company report.

Risks

What could happen that would invalidate this narrative?- ActiveOps' reliance on a single significant customer that has indicated a reduction in user base could impact ARR growth, highlighting potential risks to revenue stability.

- Notification from a significant customer about the reduction in user base implies potential vulnerability in customer retention, which might affect revenue and net margins.

- The direct sales model and limited current reliance on channel sales partners suggest potential scalability constraints, which could hinder revenue growth.

- Significant investments in marketing and R&D with varying margins in training implementation could strain net margins if additional revenue is not generated from these investments.

- Execution risk related to expanding sales and marketing capacity without directly correlating increased revenue immediately may temporarily impact earnings and net margins.

Valuation

How have all the factors above been brought together to estimate a fair value?

- The analysts have a consensus price target of £3.17 for ActiveOps based on their expectations of its future earnings growth, profit margins and other risk factors.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £3.55, and the most bearish reporting a price target of just £2.86.

- In order for you to agree with the analysts, you'd need to believe that by 2029, revenues will be £57.5 million, earnings will come to £3.7 million, and it would be trading on a PE ratio of 78.6x, assuming you use a discount rate of 9.0%.

- Given the current share price of £2.6, the analyst price target of £3.17 is 18.1% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on ActiveOps?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.