Last Update01 May 25Fair value Decreased 24%

AnalystConsensusTarget has decreased profit margin from 11.3% to 7.9% and increased future PE multiple from 125.4x to 179.6x.

Read more...Key Takeaways

- Acquisition of SeQure Dx and SPL portfolio expansion could drive future revenue growth through improved offerings and new clinical progressions.

- Strategic focus on efficiency and high-growth areas may enhance net margins and long-term profitability amid expected market growth in cell and gene therapy.

- Challenging economic conditions and cautious customer spending threaten MaxCyte's revenue and margin growth, highlighting risks in forecasting future financial performance.

Catalysts

About MaxCyte- A life sciences company, discovers, develops, and commercializes cell therapeutics in the United States and internationally.

- The acquisition of SeQure Dx expands MaxCyte's offerings into safety assessments in cell and gene therapy, providing cross-selling opportunities and potentially increasing revenue by broadening the customer base and service offerings.

- The continued expansion of MaxCyte's SPL (Strategic Platform License) portfolio, with a record number of new agreements signed in 2024, indicates a potential for future revenue growth as these programs progress to clinical development and commercialization.

- MaxCyte's focus on improving capital and operational efficiency, alongside strategic investments in high-growth areas, suggests potential enhancement in net margins and long-term profitability.

- The approval and expansion of access to the CASGEVY nonviral cell therapy model indicate future growth in commercial revenue from royalties as the therapy gains traction in new markets.

- The expected growth in the cell and gene therapy market, with potential approvals for multiple new therapies by 2027-2031, suggests substantial future revenue opportunities for MaxCyte as an enabler of these programs.

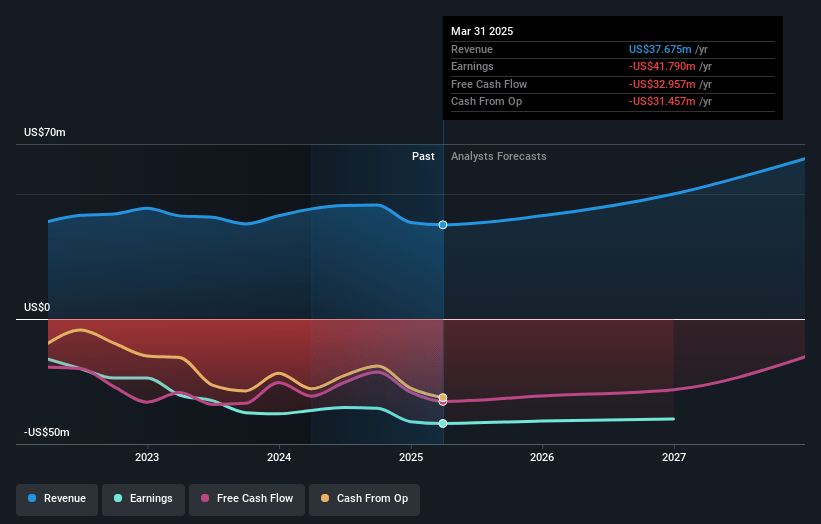

MaxCyte Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming MaxCyte's revenue will grow by 17.5% annually over the next 3 years.

- Analysts are not forecasting that MaxCyte will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate MaxCyte's profit margin will increase from -106.3% to the average GB Life Sciences industry of 7.9% in 3 years.

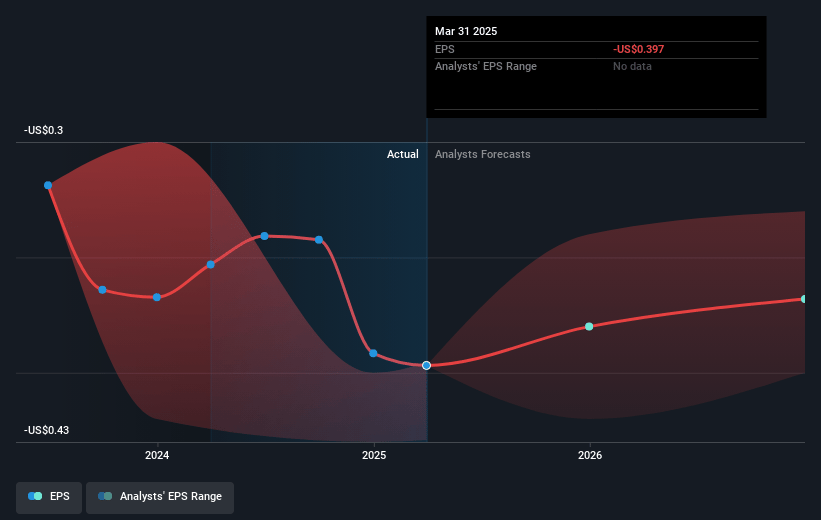

- If MaxCyte's profit margin were to converge on the industry average, you could expect earnings to reach $5.0 million (and earnings per share of $0.05) by about May 2028, up from $-41.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 179.6x on those 2028 earnings, up from -7.4x today. This future PE is greater than the current PE for the GB Life Sciences industry at 11.5x.

- Analysts expect the number of shares outstanding to grow by 1.42% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.43%, as per the Simply Wall St company report.

MaxCyte Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- MaxCyte experienced a 6% decline in total revenue in 2024 compared to 2023, and a significant 45% decline in revenue during the fourth quarter of 2024 compared to the same period in the previous year, indicating potential challenges in maintaining revenue growth.

- The company noted that instrument revenue for 2024 was impacted by customer caution on capital expenditure, which could continue to pressure revenue and margin growth if clients maintain a conservative approach to purchasing equipment.

- Gross margin declined to 74% in the fourth quarter of 2024, down from 90% in the fourth quarter of 2023, potentially affecting net margins if the trend continues.

- The operating environment remains challenging, as noted by MaxCyte, due to broader macroeconomic factors affecting customer behavior, which could impact future revenue growth and financial stability.

- MaxCyte's guidance does not assume any change in the macroeconomic environment, suggesting uncertainty and potential risks in accurately forecasting revenue growth, thereby affecting earnings projections.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £5.023 for MaxCyte based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $62.7 million, earnings will come to $5.0 million, and it would be trading on a PE ratio of 179.6x, assuming you use a discount rate of 6.4%.

- Given the current share price of £2.14, the analyst price target of £5.02 is 57.4% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.