Last Update01 Sep 25Fair value Increased 1.78%

Tesco’s fair value estimate was marginally revised upward to £4.29, primarily reflecting a modest increase in its future P/E multiple while revenue growth forecasts remained steady.

What's in the News

- Tractor Supply is expanding its final-mile delivery network by hiring drivers and renting vehicles to serve rural customers more effectively, aiming to boost digital and B2B sales (WSJ).

Valuation Changes

Summary of Valuation Changes for Tesco

- The Consensus Analyst Price Target remained effectively unchanged, moving only marginally from £4.22 to £4.29.

- The Future P/E for Tesco has risen slightly from 16.62x to 17.36x.

- The Consensus Revenue Growth forecasts for Tesco remained effectively unchanged, at 2.8% per annum.

Key Takeaways

- Investments in quality, innovation, and digital expansion aim to boost customer satisfaction, market share, and top-line growth.

- Streamlined operations and personalized pricing strategies focus on enhancing net margins and customer loyalty, supporting revenue and earnings growth.

- Intense competition, economic uncertainty, regulatory changes, and supplier cost increases could compress Tesco's margins despite investments in quality, service, and colleague pay.

Catalysts

About Tesco- Operates as a grocery retailer in the United Kingdom, Republic of Ireland, the Czech Republic, Slovakia, and Hungary.

- Tesco's focus on boosting customer satisfaction through investments in quality, innovation, and enhanced shopping experiences is expected to drive future market share gains, potentially increasing revenue growth.

- Sustained efforts in streamlining operations and achieving cost savings under their 'Save to Invest' program are likely to enhance net margins by improving operational efficiency and offsetting cost pressures.

- The decision to continue expanding their digital presence and capabilities, including the Tesco Whoosh rapid delivery service and Marketplace, is poised to boost orders and basket sizes, contributing to top-line growth.

- The strategic emphasis on Clubcard and personalized pricing strategies, coupled with expanded promotional offers, aims to deepen customer loyalty and increase sales volume, positively impacting both revenue and net margins.

- A robust commitment to shareholder returns, as evidenced by significant share buybacks, supports confidence in EPS growth while maintaining a strong balance sheet allows for strategic investments that can drive future earnings.

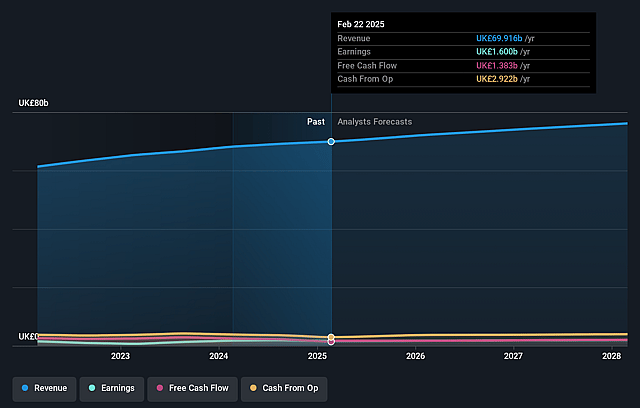

Tesco Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Tesco's revenue will grow by 2.8% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.3% today to 2.6% in 3 years time.

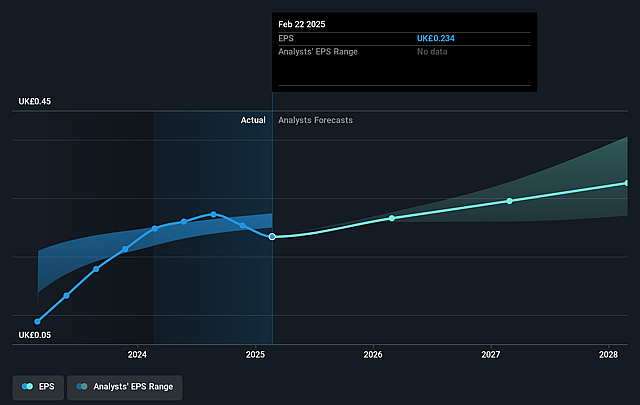

- Analysts expect earnings to reach £2.0 billion (and earnings per share of £0.33) by about September 2028, up from £1.6 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 16.8x on those 2028 earnings, down from 17.5x today. This future PE is about the same as the current PE for the GB Consumer Retailing industry at 16.8x.

- Analysts expect the number of shares outstanding to decline by 1.72% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.76%, as per the Simply Wall St company report.

Tesco Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Intense competition in the U.K. food retail sector requires Tesco to maintain high levels of quality, value, and service, which could compress net margins as they invest heavily to stay competitive.

- The economic uncertainty and pressure on household budgets may negatively impact consumer sentiment and reduce overall consumer spending, potentially hindering revenue growth.

- Increased investment in U.K. colleague store pay and wages could elevate operating expenses, affecting net margins if not offset by revenue growth.

- Regulatory changes and tax increases could impose additional costs, affecting earnings and net income if not mitigated by price increases or operational efficiencies.

- The volatility in commodity markets and exchange rates, combined with increased supplier costs, could further squeeze margins if Tesco cannot pass these costs onto consumers without losing market share.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £4.292 for Tesco based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £4.75, and the most bearish reporting a price target of just £3.16.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be £76.0 billion, earnings will come to £2.0 billion, and it would be trading on a PE ratio of 16.8x, assuming you use a discount rate of 7.8%.

- Given the current share price of £4.31, the analyst price target of £4.29 is 0.4% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.