Key Takeaways

- Expansion in the U.K. and Ireland and new product categories aim to drive revenue growth and increase market engagement.

- Digital initiatives and enhanced manufacturing could improve margins and shareholder value through efficiencies and a share buyback program.

- Challenging macroeconomic conditions, cost inflation, competitive pressures, and international expansion hurdles threaten Howden Joinery Group's revenue, margins, and market share stability.

Catalysts

About Howden Joinery Group- Supplies various kitchen, joinery, and hardware products in the United Kingdom, France, Belgium, and the Republic of Ireland.

- Continued expansion with plans to add around 20 new depots in the U.K. and 5 in the Republic of Ireland in 2025 is expected to drive revenue growth and increase market reach.

- Enhanced manufacturing capability, such as expanding the Runcorn facility and increasing in-house production from 36% of COGS, could lead to better supply chain control, benefitting gross margins.

- The introduction of new product categories, such as fitted bedrooms, and enhancements in existing categories are likely to contribute positively to revenue growth and customer engagement.

- Digital initiatives like the Live-Stock management and Click and Collect service are expected to improve operational efficiencies and customer convenience, potentially positively impacting net margins.

- The announcement of a £100 million share buyback program indicates a commitment to returning value to shareholders, which could support EPS growth in the short to medium term.

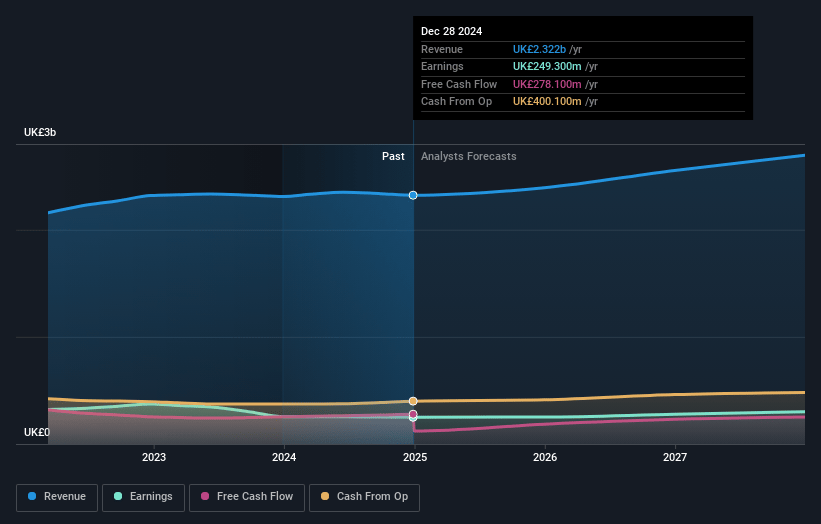

Howden Joinery Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Howden Joinery Group's revenue will grow by 5.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 10.7% today to 11.1% in 3 years time.

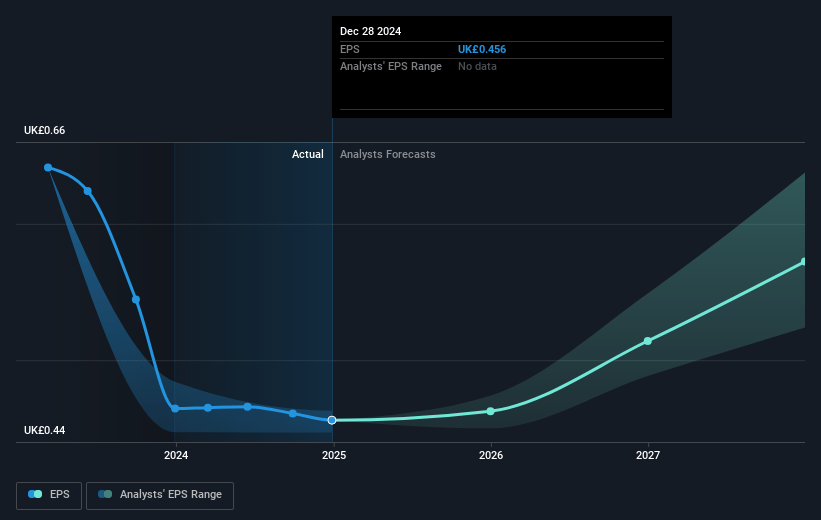

- Analysts expect earnings to reach £300.5 million (and earnings per share of £0.57) by about March 2028, up from £249.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 21.9x on those 2028 earnings, up from 17.0x today. This future PE is greater than the current PE for the GB Trade Distributors industry at 12.5x.

- Analysts expect the number of shares outstanding to grow by 0.58% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.98%, as per the Simply Wall St company report.

Howden Joinery Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The macroeconomic environment is expected to remain challenging, which could impact Howden Joinery Group's overall market size and revenue. Given the likelihood that the total market may contract, maintaining revenue could be difficult.

- There are risks associated with cost inflation, including increased contributions to Employers National Insurance and the rise in the National Minimum Wage. These costs could weigh on operating expenses, affecting net margins.

- Howden's expansion into international markets, such as France, faces hurdles. Progress on reducing losses and achieving breakeven may be delayed, impacting future earnings if international operations don't improve as planned.

- Fluctuations in demand due to changes in consumer behavior, such as trading down in price points, and a shift in the kitchen market towards more entry-level products, could pressure gross margins and affect profit levels.

- Intense competition in the market, particularly from independents, and potential disruptions from the competitive landscape could affect Howden's ability to maintain its current market share, impacting revenue stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £9.334 for Howden Joinery Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £12.1, and the most bearish reporting a price target of just £8.2.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be £2.7 billion, earnings will come to £300.5 million, and it would be trading on a PE ratio of 21.9x, assuming you use a discount rate of 8.0%.

- Given the current share price of £7.73, the analyst price target of £9.33 is 17.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives