Key Takeaways

- Strategic acquisitions and investments in innovation bolster revenue growth and strengthen Ashtead Technology’s market position across energy sectors.

- Geographic flexibility and strong customer backlogs ensure stable revenue streams and margin resilience, driving long-term earnings stability.

- Heavy reliance on acquisitions for growth might mask organic growth challenges, increasing financial risks, and impacting margins and earnings.

Catalysts

About Ashtead Technology Holdings- Provides subsea equipment rental solutions for the offshore energy sector in Europe, the Americas, the Asia-Pacific, and the Middle East.

- The acquisition of Seatronics and J2 Subsea is anticipated to enhance Ashtead Technology's integrated capabilities, providing opportunities for increased revenue through cross-selling and fleet utilization across both oil and gas and renewables markets. This supports revenue growth.

- Structural market tailwinds associated with energy security, affordability, and the transition to varied energy sources are projected to grow the total addressable market significantly, offering Ashtead Technology a stable environment to maintain double-digit organic revenue growth. This underpins long-term revenue expansion.

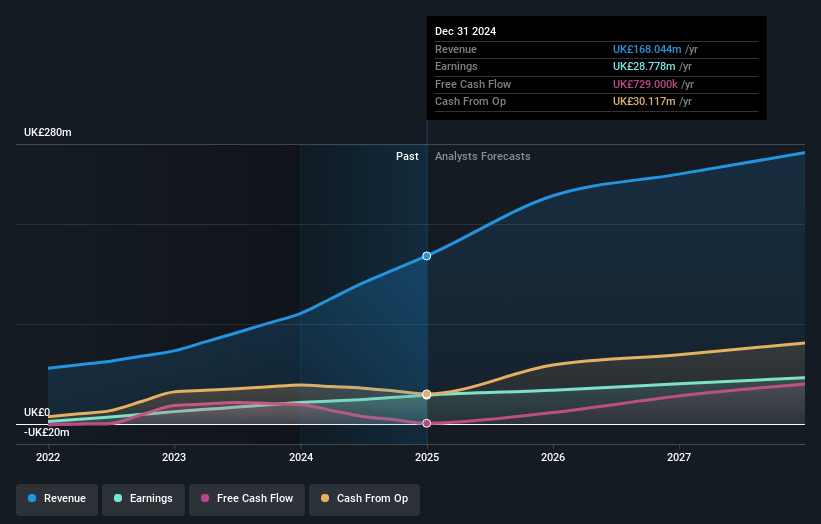

- Record multiyear customer backlogs offer better visibility and secure future revenue streams, giving Ashtead Technology confidence in its growth outlook and robust cash flow generation, which contributes to future earnings and margin stability.

- The company’s ongoing focus on geographic and equipment flexibility allows it to adapt to varying market opportunities globally, enhancing operational resilience and providing a strong basis for sustainable revenue and profit margin growth.

- Continuous investment in innovative solutions and enhanced fleet capabilities is expected to further cement Ashtead Technology's market position and drive margin improvements, supporting future earnings resilience and growth.

Ashtead Technology Holdings Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ashtead Technology Holdings's revenue will grow by 17.3% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 17.1% today to 17.0% in 3 years time.

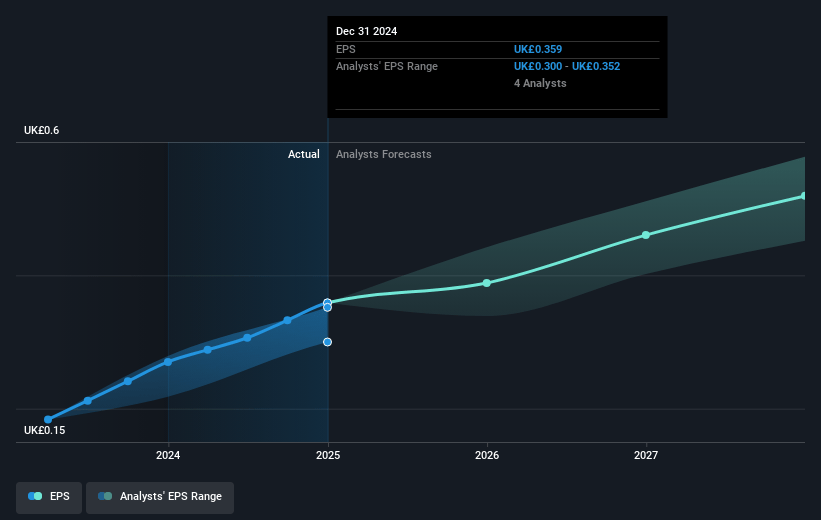

- Analysts expect earnings to reach £46.2 million (and earnings per share of £0.52) by about July 2028, up from £28.8 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 17.9x on those 2028 earnings, up from 12.6x today. This future PE is greater than the current PE for the GB Trade Distributors industry at 13.9x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.99%, as per the Simply Wall St company report.

Ashtead Technology Holdings Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The reliance on inorganic growth, with 39% of revenue growth attributed to acquisitions, might mask underlying organic growth challenges and could strain the balance sheet (increasing leverage), potentially impacting net margins and earnings.

- Increased pro forma leverage to 1.6x due to acquisitions demonstrates financial risk, which, if further increased, could affect financial stability and net earnings due to interest expenses.

- Future revenue growth is heavily dependent on the oil and gas and renewables sectors, which can be volatile and subject to political and regulatory changes that could impact projected revenues and net margins.

- Although the company claims strong prospects in subsea markets, any failures in integrating acquisitions or changes in market demand could affect revenues and EBIT margins negatively.

- The focus on maintaining a wide-range fleet could lead to high ongoing CapEx requirements that may cut into free cash flows, impacting the company’s ability to sustain its growth strategy without affecting earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of £8.011 for Ashtead Technology Holdings based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of £8.6, and the most bearish reporting a price target of just £6.6.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be £271.4 million, earnings will come to £46.2 million, and it would be trading on a PE ratio of 17.9x, assuming you use a discount rate of 9.0%.

- Given the current share price of £4.5, the analyst price target of £8.01 is 43.8% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.