Key Takeaways

- Strong cross-selling, operational integration, and advanced cloud-AI product offerings position the company for superior margin expansion and recurring revenue growth.

- Expanded global reach and high customer retention create new growth avenues and earnings diversification, potentially exceeding current market expectations.

- Heavy reliance on proprietary platforms, slow cloud migration, regulatory pressures, and intensifying competition threaten long-term growth, profitability, and market relevance.

Catalysts

About 74Software- Operates as a software company in France.

- Analysts broadly agree the Axway-SBS combination will yield synergies and higher profitability, but this may significantly understate the scale and speed of benefits-management's early success in cross-selling and ongoing operational integration could drive operating margins toward the 20 percent range much faster than currently expected, providing a step-change in earnings power.

- While analyst consensus sees steady recurring SaaS revenue growth from regulatory reporting and digital engagement expansion, there is potential for an accelerated ramp as global regulatory change and rapid cloud adoption force enterprises to transition to 74Software's platforms-meaning revenue growth could far surpass the modest single-digit outlook and drive a marked re-rating in the stock.

- Leveraging industry-wide digital transformation, 74Software's advanced product suite-particularly cloud-native and AI-powered features-positions the company to capitalize on a multi-year wave of enterprise software upgrades, strongly supporting recurring revenue growth and persistent net margin expansion as automation further reduces service delivery costs.

- The group's robust international footprint-including growing strength in North America, U.K., Africa, and expansion into emerging markets-provides significant untapped cross-border upsell and new client acquisition opportunities, which could meaningfully accelerate top-line growth and further diversify earnings streams.

- High customer satisfaction and employee engagement, combined with strong retention and upselling, suggest a sustained increase in net revenue retention and customer lifetime value-boosting long-term earnings quality and financial resilience well beyond what's reflected in current market expectations.

74Software Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more optimistic perspective on 74Software compared to the consensus, based on a Fair Value that aligns with the bullish cohort of analysts.

- The bullish analysts are assuming 74Software's revenue will grow by 20.3% annually over the next 3 years.

- The bullish analysts assume that profit margins will increase from 8.5% today to 10.2% in 3 years time.

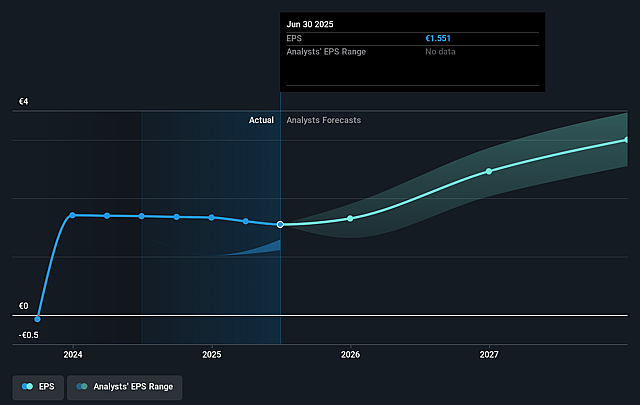

- The bullish analysts expect earnings to reach €82.0 million (and earnings per share of €3.74) by about July 2028, up from €39.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bullish analyst cohort, the company would need to trade at a PE ratio of 28.1x on those 2028 earnings, down from 28.9x today. This future PE is lower than the current PE for the GB Software industry at 29.5x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.52%, as per the Simply Wall St company report.

74Software Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Widespread adoption of open-source solutions remains a risk, as 74Software's businesses are focused on proprietary, niche platforms; this could dilute market demand and reduce the company's pricing power, resulting in downward pressure on both revenue and net margins over time.

- Despite early signs of transformation and some growth, both the Axway and SBS units of 74Software remain heavily reliant on core products within stable sectors, making the company vulnerable to technology disruption, competitive displacement, and overconcentration risk, which could sharply impact top-line revenue if customer preferences or market conditions shift.

- Heightened regulatory scrutiny, especially around privacy, data sovereignty, and new European banking rules like IREF, may require substantial investment in compliance and R&D; these increased operational and development costs would likely compress net margins and limit earnings growth.

- The company's transition to the cloud and recurring SaaS models is progressing slowly, particularly within SBS, where the ramp to revenue recognition for new SaaS deals can take 18 to 24 months, delaying the impact of booked sales and raising execution risk that could cause prolonged periods of low or unpredictable revenue growth and subdued cash flow.

- Ongoing industry consolidation and intensifying competition from both established giants and agile startups in the global enterprise software ecosystem threaten 74Software's ability to defend market share and maintain earnings; integration of software with hardware by cloud hyperscalers could marginalize independent providers like 74Software, leading to revenue contraction and reduced profitability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bullish price target for 74Software is €53.0, which is the highest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of 74Software's future earnings growth, profit margins and other risk factors from analysts on the bullish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €53.0, and the most bearish reporting a price target of just €35.0.

- In order for you to agree with the bullish analysts, you'd need to believe that by 2028, revenues will be €804.6 million, earnings will come to €82.0 million, and it would be trading on a PE ratio of 28.1x, assuming you use a discount rate of 7.5%.

- Given the current share price of €38.9, the bullish analyst price target of €53.0 is 26.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

Have other thoughts on 74Software?

Create your own narrative on this stock, and estimate its Fair Value using our Valuator tool.

Create NarrativeHow well do narratives help inform your perspective?

Disclaimer

AnalystHighTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystHighTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystHighTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.