Key Takeaways

- Transitioning to a SaaS model is driving strong recurring revenue growth and positively impacting revenue and cash flow.

- Integration and international expansion strategies enhance revenue potential, improve margins, and support organic growth in key segments.

- The shift to a subscription model and economic challenges may impact revenue growth, with risks from the GoCanvas acquisition affecting margins and profitability.

Catalysts

About Nemetschek- Provides software solutions for architecture, engineering, construction, media, and entertainment markets in Germany, rest of Europe, the Americas, the Asia Pacific, and internationally.

- Nemetschek's successful transition to a subscription and SaaS-centric business model is expected to drive strong recurring revenue growth, evidenced by the substantial increase in annual recurring revenue (ARR), which is likely to positively impact both revenue and cash flow growth in the coming 12 months.

- The integration and cross-selling opportunities between GoCanvas and Bluebeam aim to create a unique ecosystem in the construction industry, presenting significant growth potential and synergy realization, expected to enhance revenue and EBITDA margins over time.

- The strategic focus on internationalization, particularly the expansion of Bluebeam in Europe and other global markets, is anticipated to boost user growth and thereby bolster revenue expansion, aligning with forecasts for strong organic growth in the Build segment.

- Scheduled new product releases and continuous enhancements in the Design segment’s offerings (e.g., Allplan 2025, Archicad 28, Vectorworks 2025) are designed to maintain high customer satisfaction and subscription renewals, which are crucial for consistent revenue growth.

- Operational efficiencies and product integration from recent acquisitions, such as GoCanvas, are expected to allow Nemetschek to generate higher operational leverage and improved profitability, thereby positively influencing net margins and earnings growth.

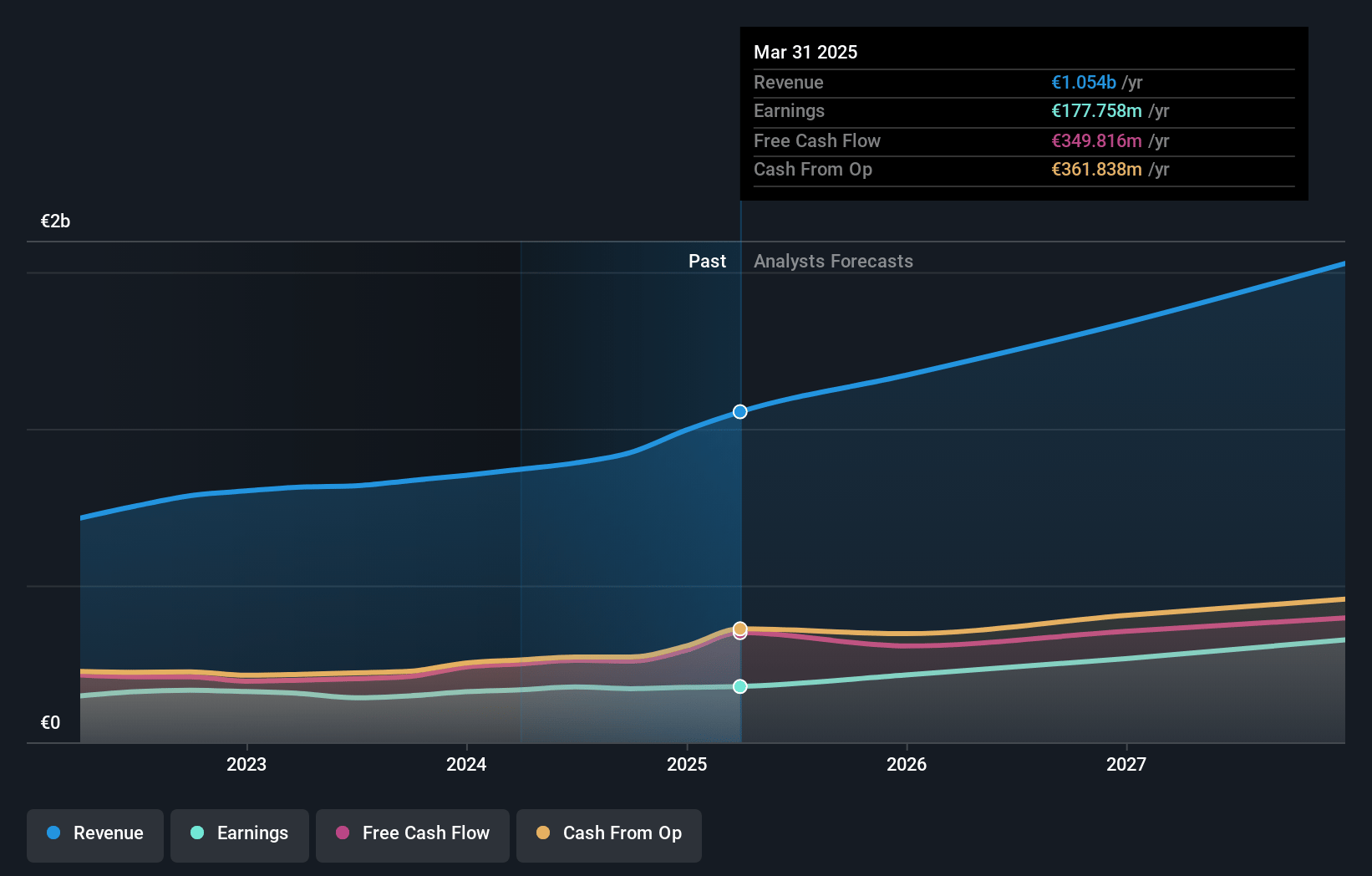

Nemetschek Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Nemetschek's revenue will grow by 16.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 18.5% today to 22.4% in 3 years time.

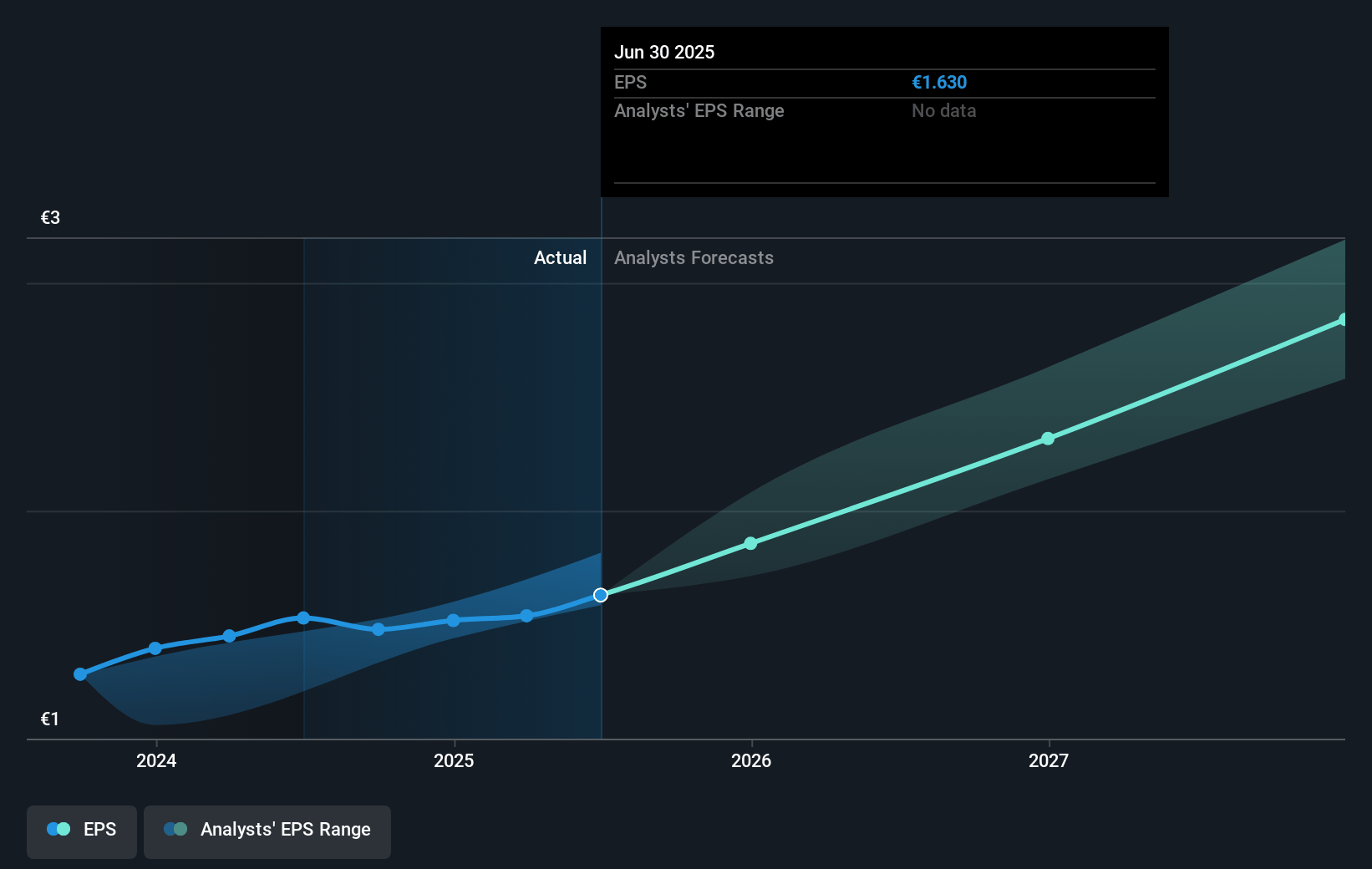

- Analysts expect earnings to reach €327.8 million (and earnings per share of €2.68) by about January 2028, up from €170.9 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 46.0x on those 2028 earnings, down from 78.1x today. This future PE is greater than the current PE for the GB Software industry at 22.8x.

- Analysts expect the number of shares outstanding to grow by 1.93% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.4%, as per the Simply Wall St company report.

Nemetschek Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The transition to a subscription and SaaS-centric business model has resulted in short-term accounting burdens, which have negatively impacted reported revenue and earnings. This is a potential risk factor if not managed effectively in the near term, impacting net margins.

- The Design segment experienced a temporary slowdown in revenue growth due to the high comparison base from the previous year, indicating potential volatility in revenue streams. This could continue to challenge top-line growth.

- The economic environment remains challenging, particularly in European markets, with uncertainties affecting customer decision-making and delaying project initiations. This could hinder revenue growth in regions like Germany.

- The integration of GoCanvas presents risks in realizing the full potential of the acquisition due to IFRS-related revenue haircuts and increased expenses. This has already led to a dilution in earnings per share, impacting overall profitability.

- Higher interest expenses from the GoCanvas acquisition have begun to weigh on net earnings, and there is also the potential risk of increased amortization charges, both of which could further pressure net margins and net earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €105.6 for Nemetschek based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €135.0, and the most bearish reporting a price target of just €68.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €1.5 billion, earnings will come to €327.8 million, and it would be trading on a PE ratio of 46.0x, assuming you use a discount rate of 5.4%.

- Given the current share price of €115.6, the analyst's price target of €105.6 is 9.5% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives