Key Takeaways

- Zalando's expanded ecosystem and loyalty program aim to enhance customer retention, engagement, and top-line growth.

- New fulfillment centers and B2B initiatives focus on market share capture, logistics efficiency, and revenue growth.

- Elevated marketing expenses, delayed fulfillment centers, and inventory overstock could compress Zalando's net margins amid heightened competition and loyalty program changes.

Catalysts

About Zalando- Operates an online platform for fashion and lifestyle products.

- Zalando's updated ecosystem strategy, including the planned loyalty program expansion, aims to boost customer retention and engagement, which should drive top-line growth and potentially increase future revenues.

- The company's focus on double-digit growth in the B2B segment through initiatives like ZEOS, enabling multi-platform fulfillment, positions Zalando to capture a larger market share and drive revenue growth in this segment.

- The launch of new fulfillment centers, including the recent opening in Paris and another planned for Frankfurt in 2026, aims to improve logistics efficiency, supporting revenue growth by enhancing customer satisfaction through faster delivery times.

- Zalando is investing in creating more engaging and entertaining shopping experiences, such as self-produced content and leveraging its tech hub in China, which could enhance customer loyalty and support long-term revenue growth.

- Strategic marketing investments, aiming for increased brand and performance marketing, are intended to strengthen customer acquisition and retention, supporting sustained revenue growth and potentially improving operating margins over time.

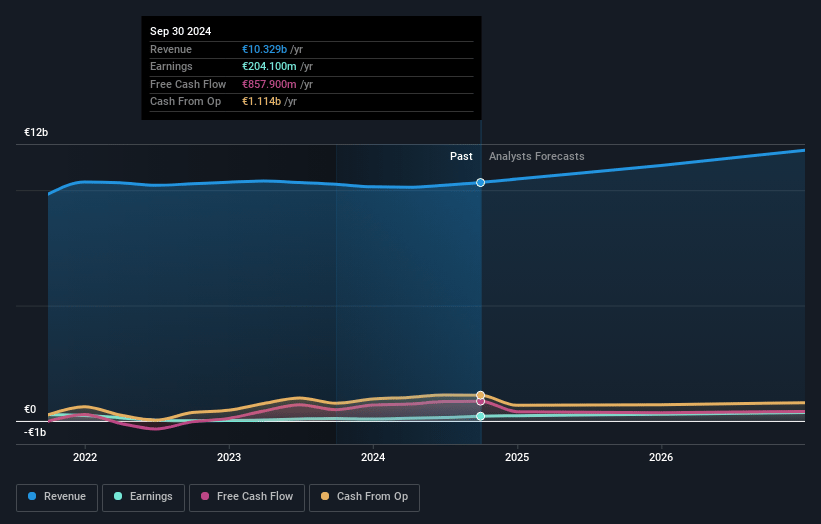

Zalando Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Zalando's revenue will grow by 7.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from 2.0% today to 3.7% in 3 years time.

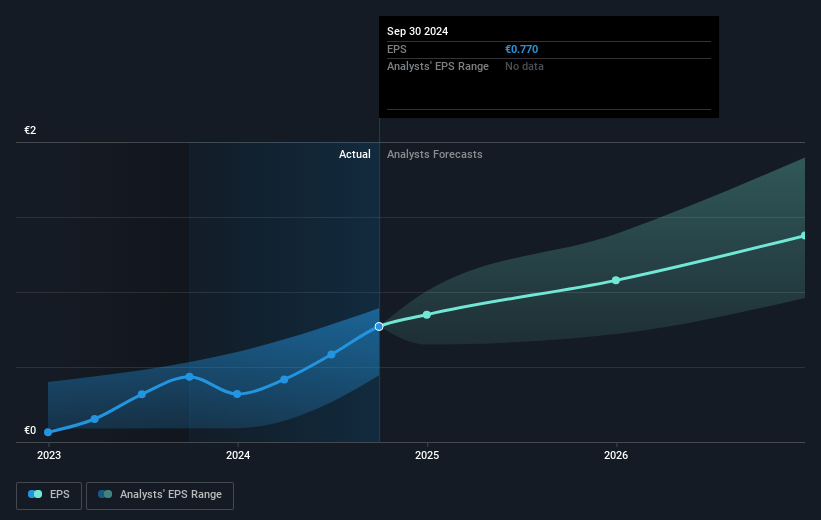

- Analysts expect earnings to reach €463.0 million (and earnings per share of €1.75) by about January 2028, up from €204.1 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as €253.2 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.5x on those 2028 earnings, down from 44.1x today. This future PE is greater than the current PE for the GB Specialty Retail industry at 22.1x.

- Analysts expect the number of shares outstanding to grow by 1.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.46%, as per the Simply Wall St company report.

Zalando Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The significant increase in inventory levels quarter-on-quarter could raise concerns about potential overstocking. This situation may pressure Zalando to sell inventory at discounted prices, which could hurt future revenue and reduce net margins.

- The shift from a paid membership program to a free loyalty-based system in the Plus program might affect revenue recognition due to a revenue deferral during rollout. It could also result in upfront costs related to reimbursing existing members, potentially impacting immediate net earnings.

- Delays in the opening of new fulfillment centers, such as the Frankfurt warehouse now pushed to 2026, may interrupt logistical efficiency and growth plans. This delay could result in elevated operational costs and limit the company’s capacity to scale profitably, thus impacting net margins.

- Increased marketing expenses, particularly through performance and brand marketing, without a proportionate increase in customers or revenue growth, could lead to tighter net margins if the customer acquisition cost exceeds the anticipated customer lifetime value.

- Heightened competition in key markets, despite some observed easing in advertising costs, may still pressure Zalando to spend more on marketing to sustain market share, potentially compressing profit margins if market conditions do not improve.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €37.92 for Zalando based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €50.0, and the most bearish reporting a price target of just €19.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €12.7 billion, earnings will come to €463.0 million, and it would be trading on a PE ratio of 25.5x, assuming you use a discount rate of 5.5%.

- Given the current share price of €35.02, the analyst's price target of €37.92 is 7.7% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

AN

andreas_eliades

Community Contributor

A Top Pick In A Struggling Industry

Investors have never been more pessimistic about Zalando's prospects, indicated by a near all-time low P/S ratio. The company is a market leader with approximately 12% of the European market share, benefiting from economies of scale.

View narrative€41.58

FV

10.8% undervalued intrinsic discount7.00%

Revenue growth p.a.

0users have liked this narrative

0users have commented on this narrative

2users have followed this narrative

4 months ago author updated this narrative