Last Update01 May 25

Key Takeaways

- Strategic expansion in production capacities and collaboration with the U.S. Department of Defense could bolster long-term revenue and market diversification.

- Focus on specialty chemicals and a share buyback program can enhance profitability and earnings, boosting investor confidence and market visibility.

- Intense competition, geopolitical pressures, and uncertainty in government funding could threaten AlzChem's profit margins, financial stability, and revenue, especially in key segments.

Catalysts

About AlzChem Group- Develops, produces, and trades chemical products in Germany, European Union, rest of Europe, Asia, NAFTA region, and internationally.

- The strategic expansion of Guanidine Salts and Nitroguanidine production capacities, both in Germany and potentially in the U.S., is expected to generate additional revenues and earnings growth, particularly in the Specialties segment, by capitalizing on demand in defense and other industries. This expansion could significantly boost revenue and earnings from 2026 onwards.

- The company's inclusion in the SDAX and the subsequent increase in investor interest can provide greater market visibility and potentially improve stock liquidity. This increased focus could positively affect valuation and investor confidence, impacting earnings per share positively.

- Continued growth in the Specialty Chemicals segment, highlighted by the performance of products such as Creapure and Creamino, is likely to sustain and potentially expand the existing 26% EBITDA margin. This focus on higher-margin, specialized products should boost overall group profitability.

- The implementation of a €6 million share buyback program can enhance earnings per share by reducing the number of shares outstanding and using shares as acquisition currency could lead to strategic opportunities that further drive growth and profitability.

- Successful cooperation with the U.S. Department of Defense, including the possibility of a new U.S. production plant for Nitroguanidine, could not only diversify AlzChem's production footprint but also open up new revenue streams and strengthen its position in the lucrative defense sector, potentially increasing future revenues and net margins.

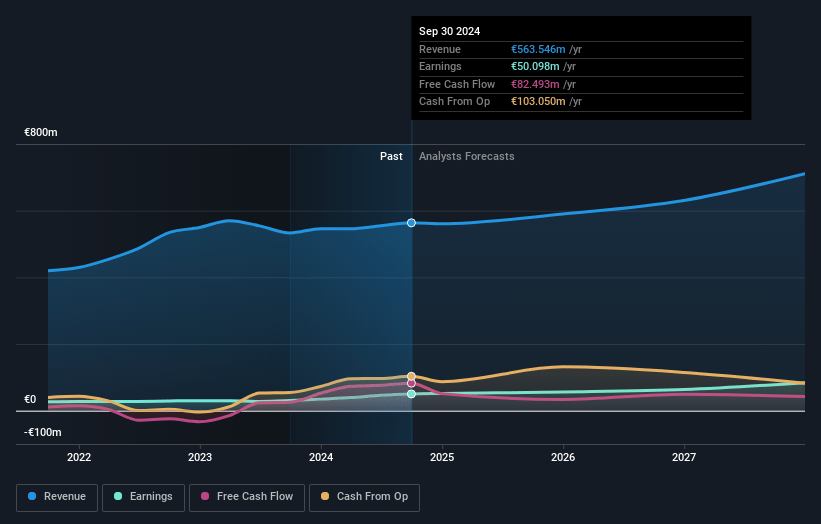

AlzChem Group Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming AlzChem Group's revenue will grow by 7.7% annually over the next 3 years.

- Analysts assume that profit margins will increase from 9.6% today to 11.6% in 3 years time.

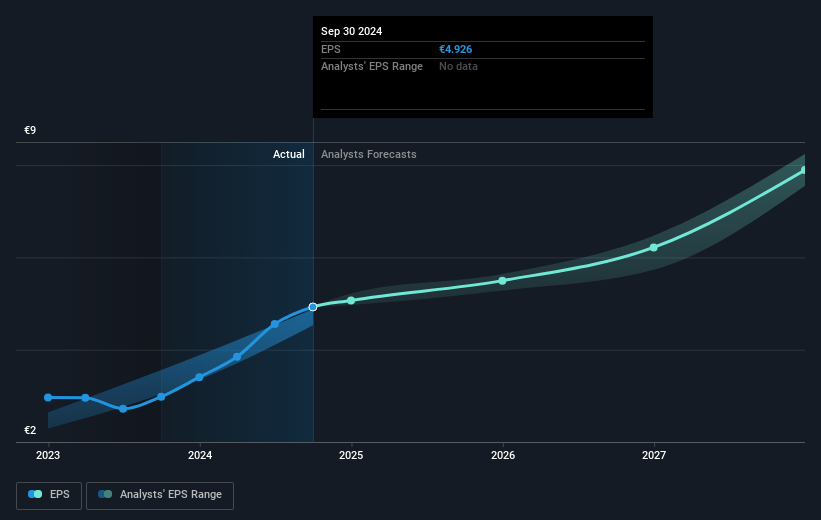

- Analysts expect earnings to reach €81.4 million (and earnings per share of €8.0) by about May 2028, up from €54.1 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as €70 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 14.6x on those 2028 earnings, down from 21.2x today. This future PE is lower than the current PE for the DE Chemicals industry at 17.2x.

- Analysts expect the number of shares outstanding to decline by 0.25% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.14%, as per the Simply Wall St company report.

AlzChem Group Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Uncertainty in government funding due to potential budgetary constraints could affect CO2 compensation, which might impact net margins if such subsidies are curtailed.

- Declining sales in certain segments, particularly Basics & Intermediates due to price and volume effects and competitive pricing pressures from Asia, could negatively impact revenue and overall earnings.

- The need for interim financing suggests potential liquidity challenges, which could affect AlzChem's ability to maintain its financial stability and impact net earnings.

- High competition and pricing pressure, particularly from Asian markets, in segments like NITRALZ and the broader Basic Intermediates, could adversely impact profit margins and revenue levels in these areas.

- Potential geopolitical pressures, such as tariffs and political changes in the US and Europe, could result in increased costs or reduced competitiveness, affecting revenue and net margins, especially concerning AlzChem’s U.S. expansion plans.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €102.38 for AlzChem Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €120.0, and the most bearish reporting a price target of just €86.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €703.9 million, earnings will come to €81.4 million, and it would be trading on a PE ratio of 14.6x, assuming you use a discount rate of 5.1%.

- Given the current share price of €113.0, the analyst price target of €102.38 is 10.4% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.