Key Takeaways

- Covestro's initiatives to reduce CO2 emissions and enhance renewable energy use aim to cut costs and improve margins.

- Increasing production reliability and potential synergies from transactions indicate promising long-term revenue and EBITDA growth.

- Declines in sales due to low prices, high working capital, and industry downturns could strain Covestro's liquidity and profitability, while leverage risks might affect future growth financing.

Catalysts

About Covestro- Supplies high-tech polymer materials and application solutions.

- The installation of a new catalyst in Covestro's nitric acid plant in China is expected to significantly reduce CO2 emissions by 60,000 tons per year by the end of 2024, potentially reducing operational costs and improving net margins.

- The shift towards renewable energy, as evidenced by the new PPA with BP for solar power, is expected to lower energy costs and enhance net margins by reducing dependency on fossil fuels.

- The introduction of an innovative heat battery by Rondo Energy at the Brunsbüttel site in Germany by 2026 is anticipated to decrease CO2 emissions by 13,000 tons annually, lowering operational expenses and potentially boosting earnings over time.

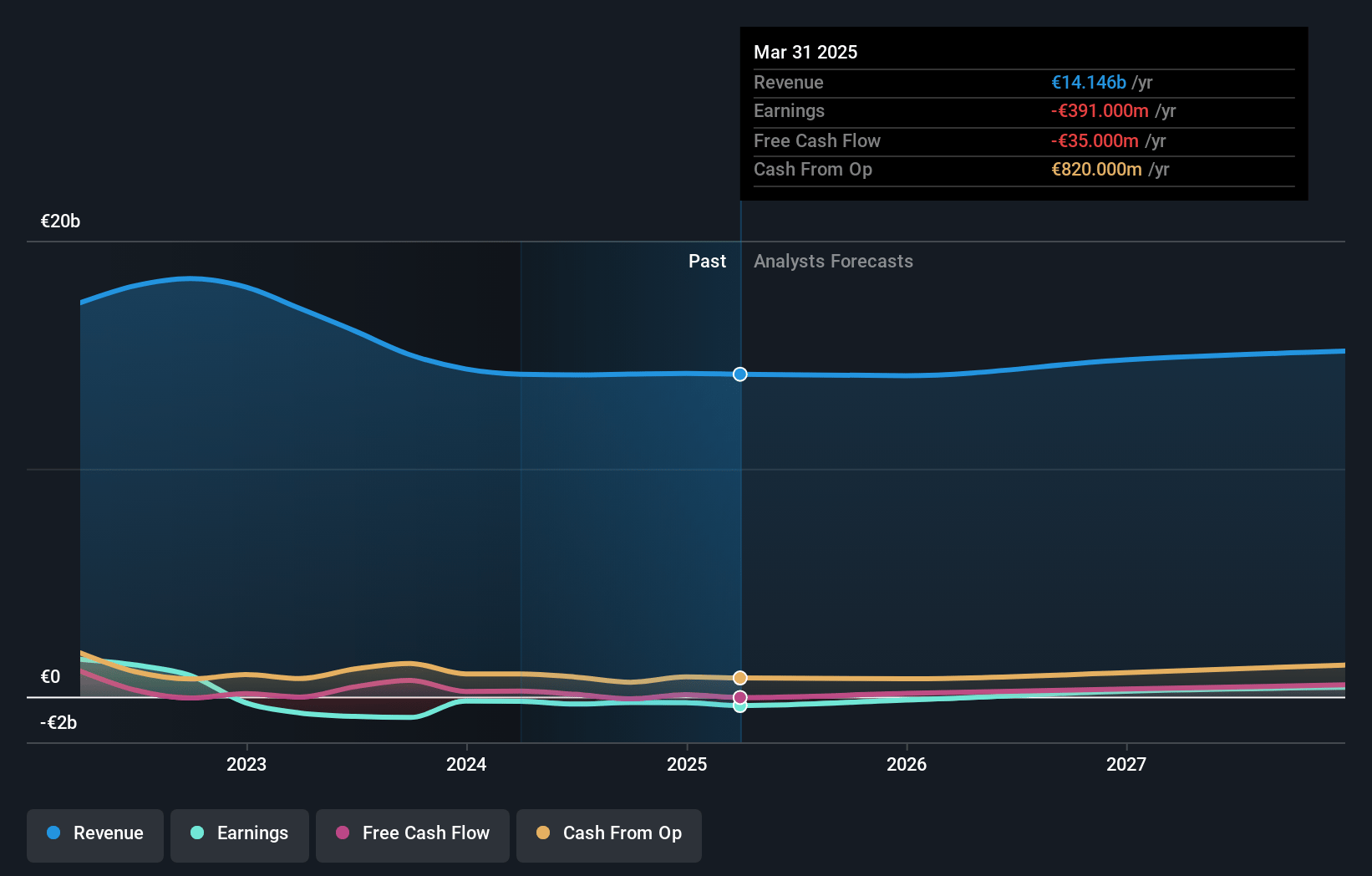

- Continuous volume growth (6.1% year-on-year) driven by improved demand and production reliability suggests potential for future revenue growth as internal availability issues are resolved.

- Ongoing improvements in production reliability and potential operational synergies from the ADNOC transaction are expected to positively impact revenue and EBITDA in the long term.

Covestro Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Covestro's revenue will grow by 4.1% annually over the next 3 years.

- Analysts assume that profit margins will increase from -1.8% today to 4.8% in 3 years time.

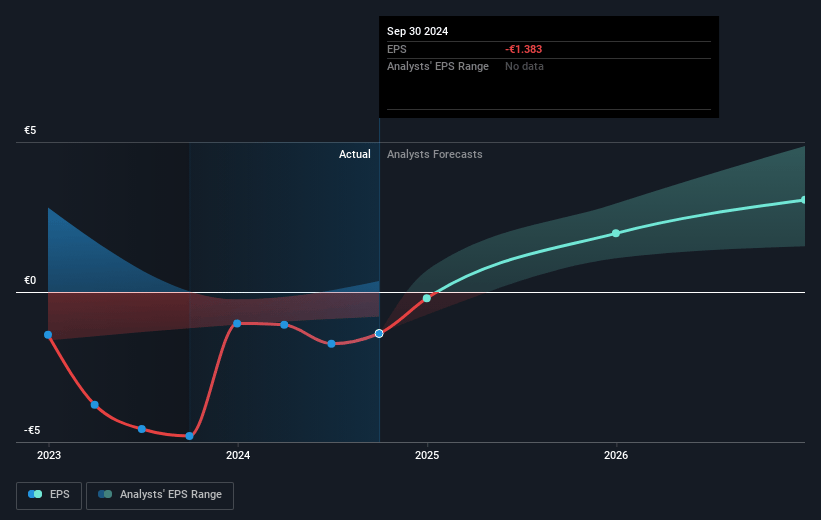

- Analysts expect earnings to reach €757.2 million (and earnings per share of €3.64) by about January 2028, up from €-261.0 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as €435.1 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.9x on those 2028 earnings, up from -41.4x today. This future PE is lower than the current PE for the GB Chemicals industry at 25.4x.

- Analysts expect the number of shares outstanding to grow by 3.31% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 5.4%, as per the Simply Wall St company report.

Covestro Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's sales were negatively affected by lower prices, which led to an unfavorable price environment impacting their revenues and EBITDA.

- A continuation of high working capital due to inventory buildup could strain liquidity, potentially impacting free cash flow and overall financial health.

- Declines in key industry sectors such as Automotive and Construction, combined with negative market outlooks, suggest potential challenges in driving sustained revenue growth.

- The historical trend of negative growth in specific segments raises concerns over persistent low margins that could affect profitability.

- The company's net debt situation, with a total net debt-to-EBITDA ratio at 3.0x, suggests potential leverage risks that may impact their ability to finance future growth initiatives or maintain investment-grade credit ratings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €61.8 for Covestro based on their expectations of its future earnings growth, profit margins and other risk factors.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €15.9 billion, earnings will come to €757.2 million, and it would be trading on a PE ratio of 19.9x, assuming you use a discount rate of 5.4%.

- Given the current share price of €57.2, the analyst's price target of €61.8 is 7.4% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives