Key Takeaways

- Increased European equity flows and integration of EU capital markets are set to boost Deutsche Börse's cash equities and Trading and Clearing revenues.

- Organic growth in Software Solutions and successful financial derivatives expansion are likely to enhance net revenue and margins.

- Dependency on external market conditions and SaaS transition risks could impact revenue stability and margin improvements amid geopolitical and macroeconomic challenges.

Catalysts

About Deutsche Börse- Operates as an international exchange organization in Germany, rest of Europe, the United States, and the Asia-Pacific.

- The resurgence of flows into European equities and funds, driven by a rotation from the U.S. to European markets due to geopolitical uncertainty and macroeconomic and valuation differentials, is expected to support Deutsche Börse’s cash equities business and the Fund Services segment, positively impacting net revenue growth.

- The structural medium-term driver from increased German and European defense and infrastructure investments, coupled with rising amounts of debt outstanding, is anticipated to benefit Deutsche Börse’s Securities Services and financial derivatives business, likely enhancing net revenue and cash flow over time.

- The Savings and Investment Union initiative by the European Commission, aiming to integrate EU capital markets and increase retail investor participation, is foreseen to drive demand for products offered by Deutsche Börse, potentially boosting Trading and Clearing revenues and overall earnings.

- The strong organic growth trajectory in the Software Solutions business, with a 15% year-on-year increase in annual recurring revenue driven by significant customer wins in North America, including a large U.S. asset manager and a major public pension fund, is expected to maintain double-digit net revenue growth, enhancing overall earnings.

- The successful execution of the fixed income roadmap, evidenced by 11% net revenue growth in financial derivatives and new product introductions like EU bond futures, positions Deutsche Börse to capitalize on continued demand in this space, potentially increasing revenue and net margins.

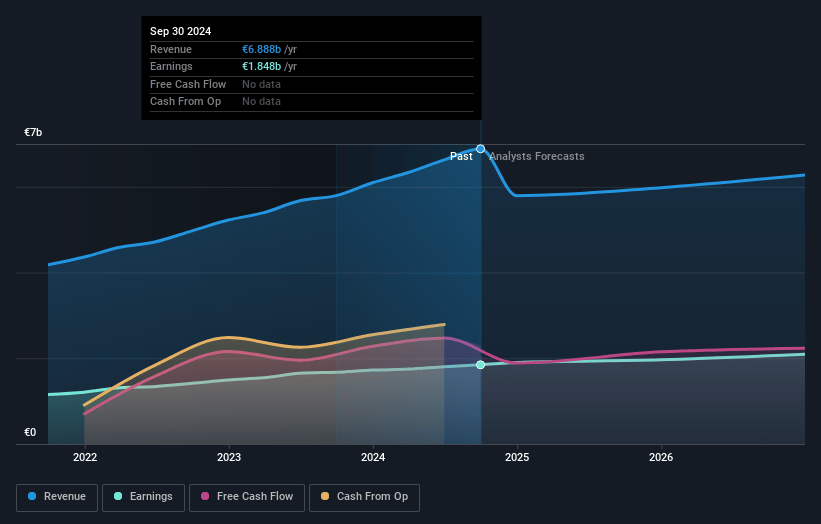

Deutsche Börse Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Deutsche Börse's revenue will grow by 4.6% annually over the next 3 years.

- Analysts assume that profit margins will increase from 33.2% today to 34.4% in 3 years time.

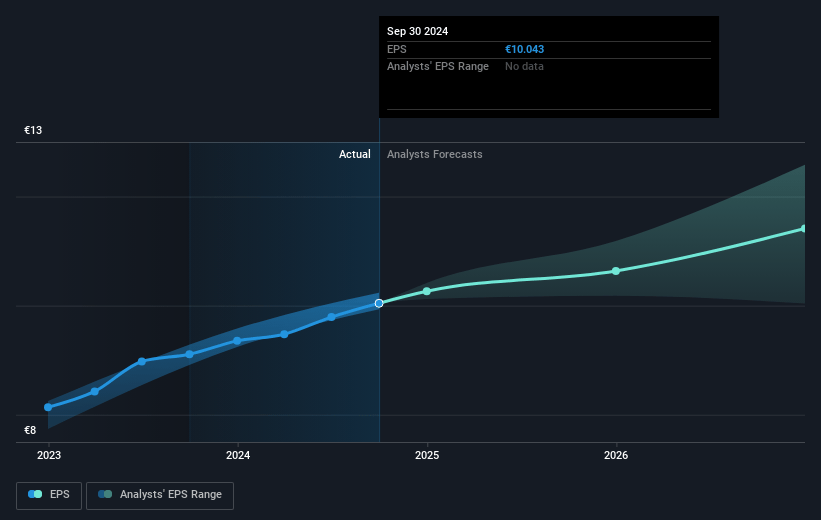

- Analysts expect earnings to reach €2.3 billion (and earnings per share of €12.8) by about July 2028, up from €2.0 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 25.7x on those 2028 earnings, up from 24.2x today. This future PE is greater than the current PE for the GB Capital Markets industry at 21.2x.

- Analysts expect the number of shares outstanding to grow by 0.1% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.25%, as per the Simply Wall St company report.

Deutsche Börse Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The volatility in quarterly revenue due to the point-in-time recognition of software sales, despite strong ARR growth, may lead to inconsistent short-term financial performance, impacting revenue forecasts and market confidence.

- Higher-than-expected operating costs, driven by provisions for share-based compensation and unfavorable currency impacts, could put pressure on net margins if cost control measures are not effectively implemented.

- The dependency on external market conditions, such as market volatility and interest rate changes, introduces uncertainty in revenue projections for trading and clearing segments, which could affect earnings stability.

- The strategy of transitioning clients to SaaS from on-premise systems introduces risks related to the speed and cost of transition, potentially affecting revenue growth and margin improvement if clients are slow to adopt the new model.

- Despite investor confidence in European market opportunities, geopolitical tensions and macroeconomic shifts, particularly in European debt markets, may affect expected revenue gains from equities and securities services.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €272.5 for Deutsche Börse based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €309.0, and the most bearish reporting a price target of just €220.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €6.8 billion, earnings will come to €2.3 billion, and it would be trading on a PE ratio of 25.7x, assuming you use a discount rate of 6.2%.

- Given the current share price of €260.1, the analyst price target of €272.5 is 4.6% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.