Key Takeaways

- Strategic synergies and sustainability initiatives aim to enhance operational efficiency and future revenue growth in line with global demand.

- Technological integration through joint ventures and efficiency improvements could optimize margins and stabilize earnings.

- Ongoing challenges in key markets, infrastructure gaps for electric trucks, and foreign exchange risks threaten Daimler Truck's profitability and future earnings.

Catalysts

About Daimler Truck Holding- Manufactures and sells light, medium- and heavy-duty trucks and buses in Europe, North America, Asia, Latin America, and internationally.

- Daimler Truck aims to leverage synergies and optimize its global portfolio, which could improve operational efficiency and expand market share, impacting revenue positively.

- The push towards sustainability, including the introduction of new low-carbon and battery electric trucks, is expected to align with global trends and customer demand, positioning the company for future revenue growth.

- The joint venture with Volvo Group to build a software-defined vehicle platform suggests a forward-looking shift towards integrating technology, enhancing product offerings and potentially increasing net margins through more efficient operations.

- The efficiency push at Mercedes-Benz Trucks, targeting cost reduction and process optimization, could enhance resilience and improve net margins in challenging market conditions.

- The planned cash flow improvements, through inventory reductions and optimization of production schedules, indicate a strategic focus on liquidity management, supporting earnings stabilization and potential growth.

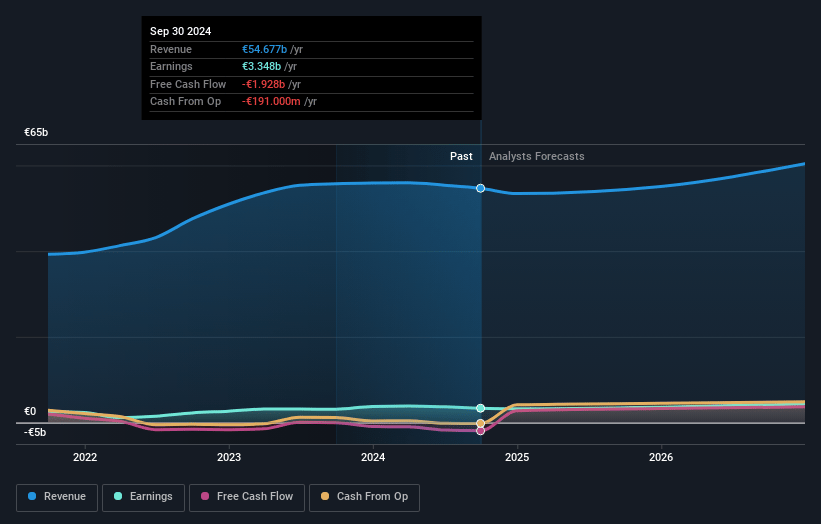

Daimler Truck Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Daimler Truck Holding's revenue will grow by 3.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 6.1% today to 7.3% in 3 years time.

- Analysts expect earnings to reach €4.4 billion (and earnings per share of €4.86) by about January 2028, up from €3.3 billion today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting €4.9 billion in earnings, and the most bearish expecting €3.2 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 11.8x on those 2028 earnings, up from 9.9x today. This future PE is lower than the current PE for the DE Machinery industry at 16.6x.

- Analysts expect the number of shares outstanding to grow by 4.85% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.0%, as per the Simply Wall St company report.

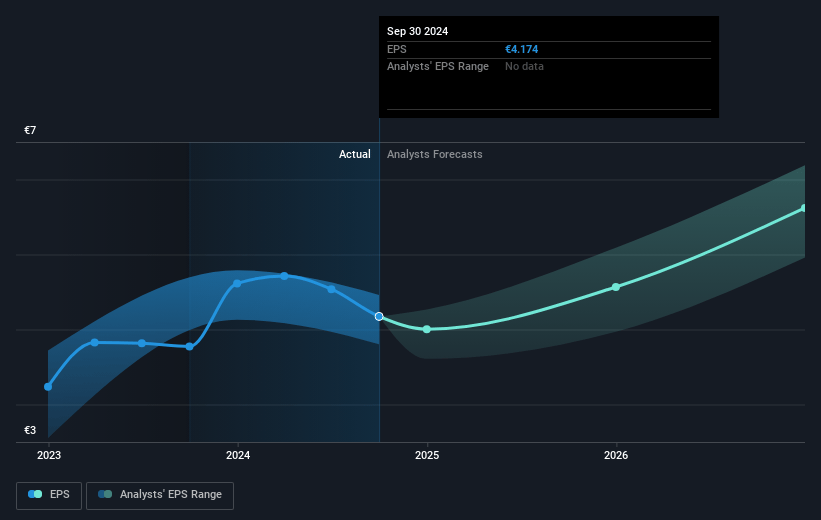

Daimler Truck Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- There is a clear challenge in the European market with demand continuing to be weak, which could negatively impact revenue and profitability, particularly in the Mercedes-Benz Trucks segment.

- The decrease in unit sales and the unfavorable sales mix, especially in North America, creates financial pressure, reducing EBIT, which may affect net margins and earnings.

- Although Daimler Truck is pushing for a shift towards zero-emission vehicles, the lack of necessary infrastructure for electric trucks poses a significant risk, potentially hindering revenue growth in this segment.

- The current freight recession in the U.S. poses a risk through adverse impacts on the valuation of provisions and potential credit losses in Financial Services, affecting net income.

- Exposure to foreign exchange risks and underutilization challenges, particularly in Europe and China, present financial uncertainties that could adversely affect net margins and future earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of €46.83 for Daimler Truck Holding based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of €56.0, and the most bearish reporting a price target of just €33.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be €59.7 billion, earnings will come to €4.4 billion, and it would be trading on a PE ratio of 11.8x, assuming you use a discount rate of 7.0%.

- Given the current share price of €42.37, the analyst's price target of €46.83 is 9.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives