Narratives are currently in beta

Key Takeaways

- Low-yield investments in CBDs may increase acquisition costs, pressuring net margins amid worsening economic conditions.

- Pipeline projects may boost long-term growth, but entail upfront costs and risks, impacting short-term earnings.

- Strong demand in key locations and strategic projects may drive revenue growth, stabilize valuations, and enhance rental income and net margins for PSP Swiss Property.

Catalysts

About PSP Swiss Property- Owns and manages real estate properties in Switzerland.

- The high liquidity and low-yield environment in the core CBDs, such as Zurich, Geneva, and Bern, may encourage PSP Swiss Property to invest at low yields, potentially increasing acquisition costs and pressuring net margins if the economic environment worsens.

- Rising financial expenses, although stabilized, might still incrementally increase by CHF 2-3 million per year, leading to higher interest payments and a potential reduction in net earnings if revenues do not rise parallelly.

- Vacancy rate improvements are partly fueled by the reclassification of properties to development projects, such as Wallisellen, which might introduce execution risks and delay rental income increases, impacting revenue growth.

- Turnover-based rental income is expected to grow, but reliance on specific sectors like hotels and restaurants could introduce volatility in rental revenue, especially in fluctuating economic conditions.

- Additional development projects in the pipeline, such as in Bern, Basel, and Lausanne, while potentially beneficial in the long term, could entail upfront costs and execution risks that might pressure short-term earnings and financials.

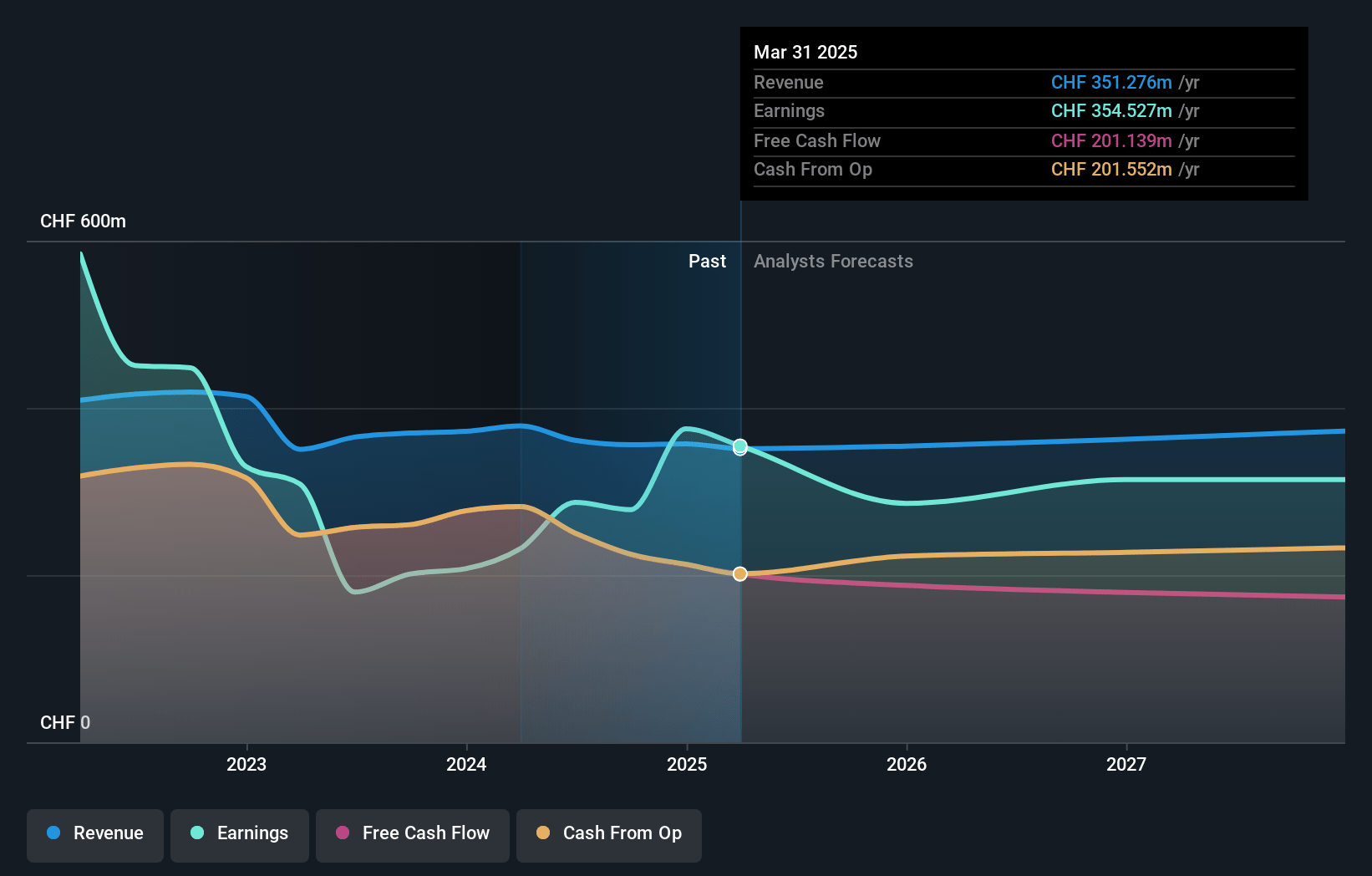

PSP Swiss Property Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming PSP Swiss Property's revenue will grow by 1.4% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 78.2% today to 70.2% in 3 years time.

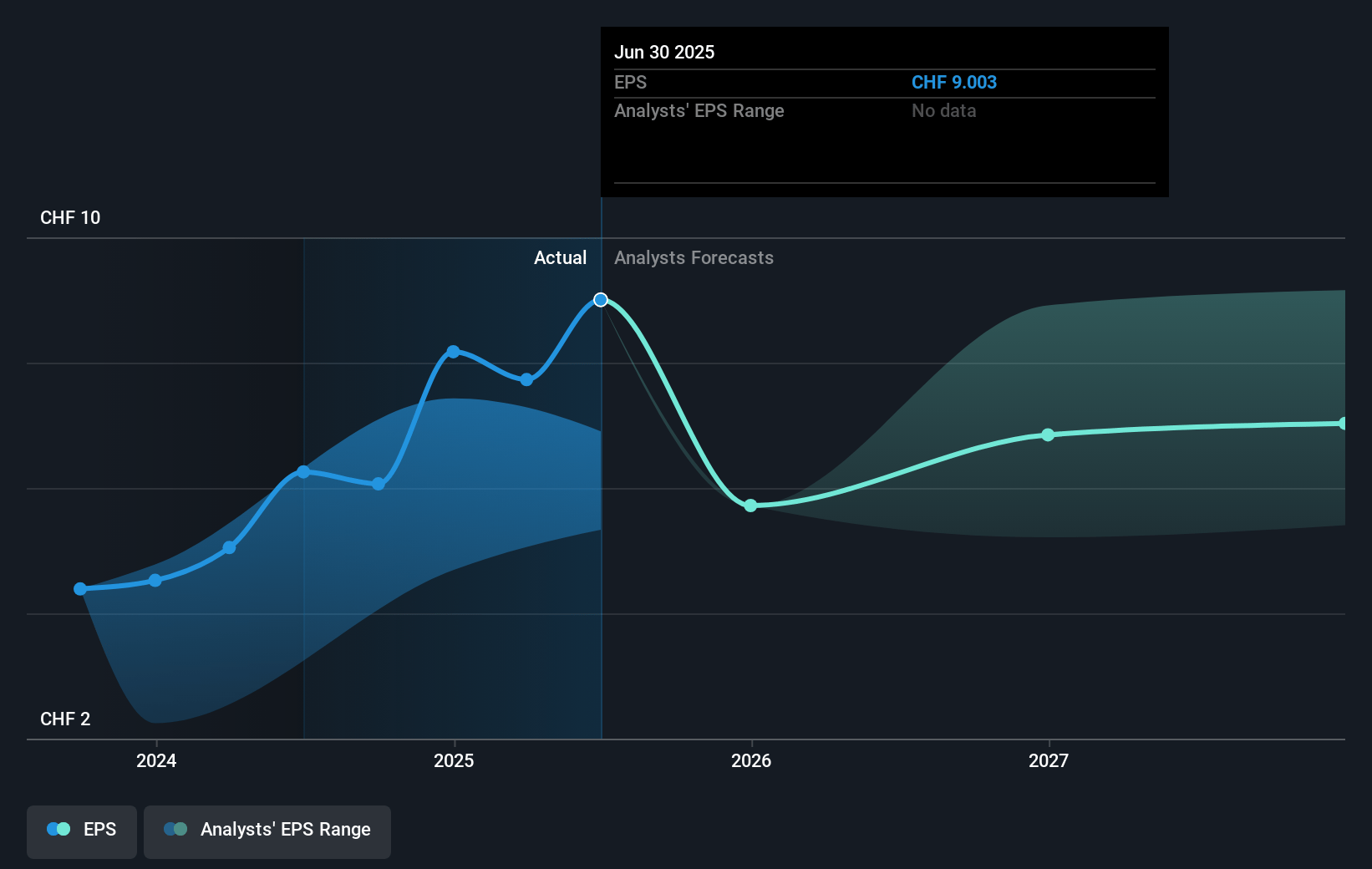

- Analysts expect earnings to reach CHF 260.8 million (and earnings per share of CHF 5.72) by about January 2028, down from CHF 278.2 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CHF 219 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.2x on those 2028 earnings, up from 21.3x today. This future PE is lower than the current PE for the GB Real Estate industry at 27.4x.

- Analysts expect the number of shares outstanding to decline by 0.18% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.17%, as per the Simply Wall St company report.

PSP Swiss Property Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- PSP Swiss Property is experiencing solid demand in key locations such as CBDs of Zurich, Geneva, and Bern, which supports rental income and may lead to favorable rent renewals and revenue growth.

- The transactional evidence of properties in central Zurich is leading to very low yields, suggesting a strong market that may stabilize or increase property valuations and net margins.

- The company reported a 5.8% rise in rental income for the first 9 months of the year, demonstrating consistent revenue growth driven by factors such as indexation and successful property letting strategies.

- PSP Swiss Property continues to maintain a high EBITDA margin of 84-85% by keeping expenses under control, which suggests sustained earnings levels and potentially improved net margins.

- There are ongoing development and repositioning projects, including in Bern and Geneva, which could further boost rental income and enhance earnings opportunities as these projects come to fruition.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CHF 131.7 for PSP Swiss Property based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF 148.0, and the most bearish reporting a price target of just CHF 125.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CHF 371.6 million, earnings will come to CHF 260.8 million, and it would be trading on a PE ratio of 27.2x, assuming you use a discount rate of 6.2%.

- Given the current share price of CHF 128.9, the analyst's price target of CHF 131.7 is 2.1% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

There are no other narratives for this company.

View all narratives