Key Takeaways

- The EVOLVE+ strategy and strategic M&A activities are set to enhance growth, expand services, and improve margins for Siegfried Holding.

- Investments in new technologies and diversification across portfolios are expected to drive revenue stability and efficiency improvements.

- Currency depreciation and input cost increases threaten revenue and profitability, while new plant operations and contract shifts impact margins and cash flow.

Catalysts

About Siegfried Holding- Engages in contract development and manufacturing of active pharmaceutical ingredient (API) and finished dosage forms worldwide.

- The EVOLVE+ strategy, with a focus on operational excellence, supply reliability, and sustainable growth, is expected to drive Siegfried Holding’s continued profitable growth, potentially impacting revenue and net margins positively.

- Strategic M&A activities, such as the acquisition of the Grafton site, are expected to expand Siegfried's U.S. network and provide end-to-end services, enhancing future revenue growth and potentially improving margins.

- The company's investment in new manufacturing technologies and capacity expansions (e.g., prefilled syringes and spray drying) is anticipated to drive future revenue growth as these projects become operational.

- Diversification across customer and product portfolios reduces reliance on single clients or products, increasing stability and potential for consistent revenue growth.

- The implementation of operational excellence initiatives, including inventory management improvements and process optimizations, is expected to enhance efficiency and positively impact net margins.

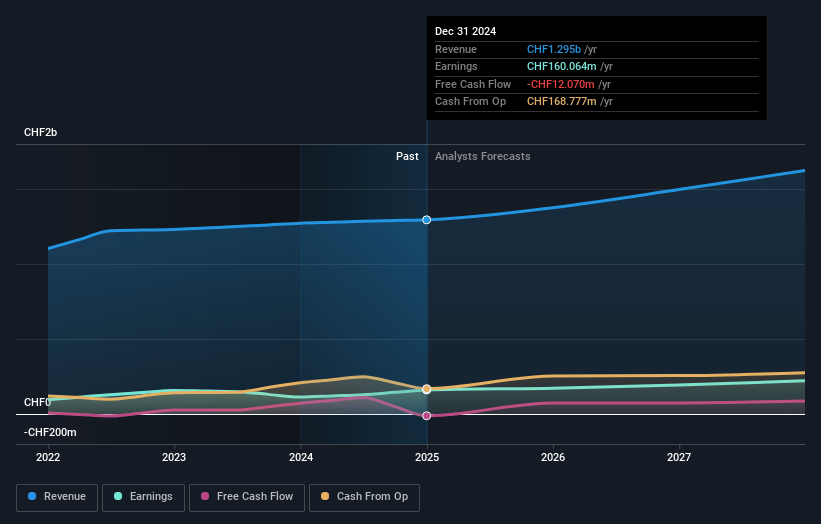

Siegfried Holding Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Siegfried Holding's revenue will grow by 7.2% annually over the next 3 years.

- Analysts assume that profit margins will increase from 12.4% today to 13.5% in 3 years time.

- Analysts expect earnings to reach CHF 215.5 million (and earnings per share of CHF 4.41) by about July 2028, up from CHF 160.1 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 27.4x on those 2028 earnings, up from 24.8x today. This future PE is lower than the current PE for the GB Life Sciences industry at 32.2x.

- Analysts expect the number of shares outstanding to grow by 2.35% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 4.56%, as per the Simply Wall St company report.

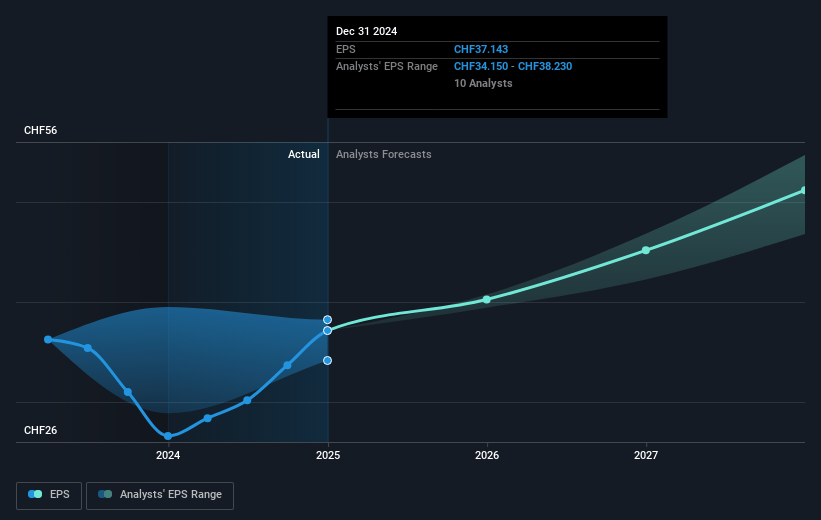

Siegfried Holding Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The phasing out of the vaccines business and ongoing destocking effects indicate potential revenue challenges, with some impact still expected in 2025, potentially affecting top-line growth. (Revenue)

- Continued foreign exchange headwinds, with expected depreciation of the euro and dollar against the Swiss franc, could negatively impact revenue and profitability due to currency translations. (Profitability)

- The effect of the expiration of certain contracts or changes in customer relationships could impact short-term cash flow and necessitate adjustments in financial planning. (Cash Flow)

- Potential increases in depreciation due to new manufacturing plant operations, such as the one in Minden, might affect net margins in the short term until these facilities reach full operational efficiency. (Net Margins)

- Any shift in raw material or input costs could affect gross margins, particularly if these costs rise and cannot be completely passed on to customers through pricing adjustments. (Gross Profit)

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CHF112.42 for Siegfried Holding based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF142.0, and the most bearish reporting a price target of just CHF94.5.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CHF1.6 billion, earnings will come to CHF215.5 million, and it would be trading on a PE ratio of 27.4x, assuming you use a discount rate of 4.6%.

- Given the current share price of CHF90.8, the analyst price target of CHF112.42 is 19.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.