Last Update 10 Nov 25

Fair value Increased 0.64%BAER: Revenue Expectations And Fair Value Revisions Will Shape Outlook

Narrative Update on Julius Bär Gruppe

Analysts have increased their price target for Julius Bär Gruppe by CHF 3, citing improved revenue growth expectations and a slightly higher fair value assessment, even though changes in the company's profit margin and discount rate have been modest.

Analyst Commentary

Bullish Takeaways

- Bullish analysts have increased their price target to CHF 72, signaling confidence in the company's growth prospects.

- Improved revenue growth expectations are a key driver for the higher valuation. This reflects positive sentiment towards Julius Bär Gruppe's market positioning.

- The Overweight rating suggests analysts believe the shares are poised to outperform peers, driven by robust execution and solid fundamentals.

- Modest changes in profit margins and discount rates are not seen as enough to offset the positive outlook for future earnings and expansion potential.

What's in the News

- Julius Bär Gruppe has received regulatory approvals to open a dedicated presence of Bank Julius Baer Europe Ltd. in Lisbon, Portugal. Operations are set to begin in the fourth quarter of 2025. (Key Developments)

- The new office on Avenida da Liberdade will focus on servicing ultra-high and high-net-worth clients in Portugal, emphasizing client proximity with a locally based team. (Key Developments)

- The existing team will relocate to the new Lisbon premises at the start of January 2026, maintaining the current leadership for operational continuity. (Key Developments)

Valuation Changes

- Fair Value has risen slightly from CHF 60.81 to CHF 61.20.

- Discount Rate has edged up modestly, moving from 8.87% to 8.91%.

- Revenue Growth expectations have increased from 6.32% to 7.10%.

- Net Profit Margin has decreased from 26.68% to 25.23%.

- Future P/E has increased moderately from 13.53x to 14.17x.

Key Takeaways

- Rising global wealth and operational efficiency are driving sustained profit growth, supporting future revenue and fee-based income expansion.

- Strategic digital transformation and prudent risk management boost client retention, while resumed share buybacks may enhance shareholder value.

- Ongoing credit risks, weak capital flexibility, limited cost savings, and slow expansion make Julius Bär Gruppe vulnerable to stagnation amid rising competition and digital disruption.

Catalysts

About Julius Bär Gruppe- Provides wealth management solutions in Switzerland, Europe, the Americas, Asia, and internationally.

- Strong growth in net new money and significant year-on-year increases in underlying net profit signal that Julius Bär is capturing rising global wealth and intergenerational transfers, which should directly support future revenue and fee-based income expansion.

- Progress in cost efficiency, as evidenced by the lower cost-income ratio and ahead-of-plan CHF 130 million cost savings target, suggests sustained improvement in operational margins and profitability going forward.

- The robust balance sheet and ongoing investment in risk management position the company to capitalize on increased demand for reputable and compliant private banks amid global regulatory scrutiny, aiding client retention and supporting net new money inflows.

- Strategic execution focused on delivering exceptional wealth management services and ongoing digital transformation is expected to enhance client experience, driving sustained advisory revenues and more stable earnings.

- Intentions to resume share buybacks in the future, once timing permits, indicate that capital returns to shareholders could further boost earnings per share over time.

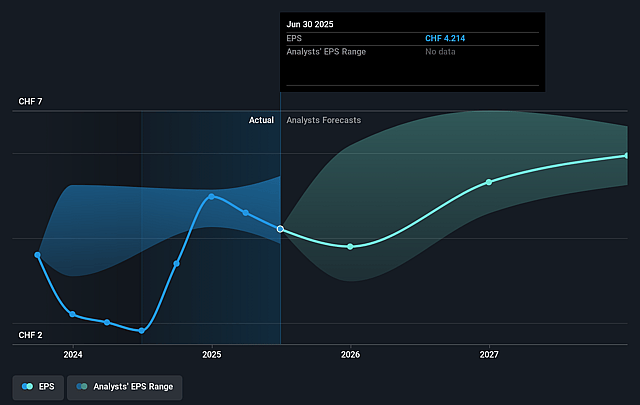

Julius Bär Gruppe Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Julius Bär Gruppe's revenue will grow by 6.3% annually over the next 3 years.

- Analysts assume that profit margins will increase from 23.2% today to 26.7% in 3 years time.

- Analysts expect earnings to reach CHF 1.2 billion (and earnings per share of CHF 6.35) by about September 2028, up from CHF 865.4 million today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as CHF1.0 billion.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.5x on those 2028 earnings, up from 13.4x today. This future PE is lower than the current PE for the GB Capital Markets industry at 16.3x.

- Analysts expect the number of shares outstanding to grow by 0.29% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 8.87%, as per the Simply Wall St company report.

Julius Bär Gruppe Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The significant 35% year-on-year decrease in IFRS net profit, mainly related to loan loss allowances and the sale of the Brazilian onshore business, highlights ongoing credit quality and geographic concentration risks that may continue to negatively impact earnings if not addressed through sustained diversification and risk controls.

- The company's hesitation or inability to commit to a share buyback in the near term, even as investors expected it, may signal constrained capital flexibility or uncertainty about future cash flows, potentially reducing shareholder returns and dampening near

- to medium-term share price appreciation.

- The continuing credit review by the new Chief Risk Officer indicates unresolved risk exposures in the loan book, raising the prospect of further loan loss allowances or write-downs; this undermines confidence in asset quality and could significantly weigh on both net margins and future profitability.

- Achieving CHF 130 million in cost savings by the end of 2025 is essential to improving the cost-income ratio, but sustained cost pressures due to regulatory requirements, compliance, and potential operational inefficiencies may limit success on this front, restricting operating leverage and margin improvement.

- The one-off impact from exiting the Brazilian onshore market, along with a lack of mention of significant expansion into high-growth regions or digital innovation, exposes Julius Bär Gruppe to the risk of stagnation, as it may lag competitors in capturing emerging market growth and adapting to digital disruption-this could hinder long-term net new money inflows and revenue growth.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of CHF60.813 for Julius Bär Gruppe based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CHF70.0, and the most bearish reporting a price target of just CHF52.4.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be CHF4.5 billion, earnings will come to CHF1.2 billion, and it would be trading on a PE ratio of 13.5x, assuming you use a discount rate of 8.9%.

- Given the current share price of CHF56.78, the analyst price target of CHF60.81 is 6.6% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.