Key Takeaways

- Long-term gold demand faces pressure from rising ESG trends and alternative investments, threatening sustained revenue growth and market competitiveness.

- Heightened regulatory, environmental, and capital challenges increase costs and operational risks, potentially constraining margins and shareholder returns.

- Strategic project execution, sustained gold prices, operational improvements, and disciplined capital allocation collectively support stronger cash flow, margin expansion, and resilient long-term shareholder value.

Catalysts

About Eldorado Gold- Engages in the mining, exploration, development, and sale of mineral products primarily in Turkey, Canada, and Greece.

- Despite recent record-high gold prices which have buoyed Eldorado Gold's revenue and profitability, the accelerating global shift toward renewable energy and alternative investment vehicles may erode long-term demand for gold, capping price growth and directly limiting Eldorado's ability to sustain top-line revenue growth over the coming decade.

- Persistent and increasing policy and regulatory pressure on environmental emissions and sustainability, particularly in key jurisdictions like Greece and Turkey, may result in higher compliance costs, operational delays, or restrictions, constraining Eldorado's profitability and putting significant pressure on operating margins.

- The company's ongoing capital intensity for mine development-especially the substantial expenditures for the Skouries project and sustaining capital at operating mines-could strain free cash flow for years, increasing the risk of higher leverage or dilution through future equity raises, ultimately weighing on earnings per share and net margins.

- Rising global mine reserve depletion and declining ore grades are expected to push extraction costs even higher, while heightened competition from low-cost producers and increased gold recycling can limit Eldorado's market share, eroding margins and threatening the company's long-term competitive position and profitability.

- With global capital flows increasingly favoring ESG-friendly sectors over resource extraction, Eldorado Gold may face reduced access to premium financing and less favorable shareholder returns, which, coupled with a tightening social license to operate and heightened opposition to new projects, could further dampen valuation and future growth prospects.

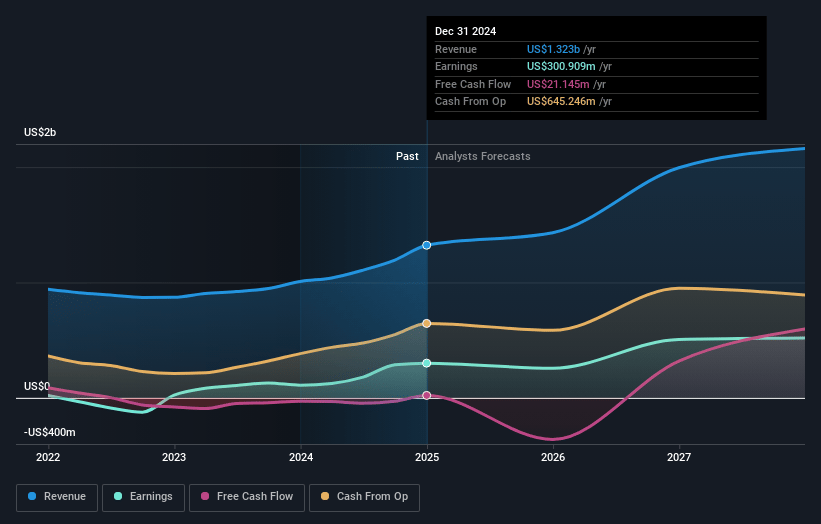

Eldorado Gold Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Eldorado Gold compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Eldorado Gold's revenue will grow by 22.9% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 23.9% today to 25.9% in 3 years time.

- The bearish analysts expect earnings to reach $682.9 million (and earnings per share of $3.39) by about July 2028, up from $339.7 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 7.2x on those 2028 earnings, down from 12.4x today. This future PE is lower than the current PE for the US Metals and Mining industry at 16.7x.

- Analysts expect the number of shares outstanding to grow by 0.34% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.99%, as per the Simply Wall St company report.

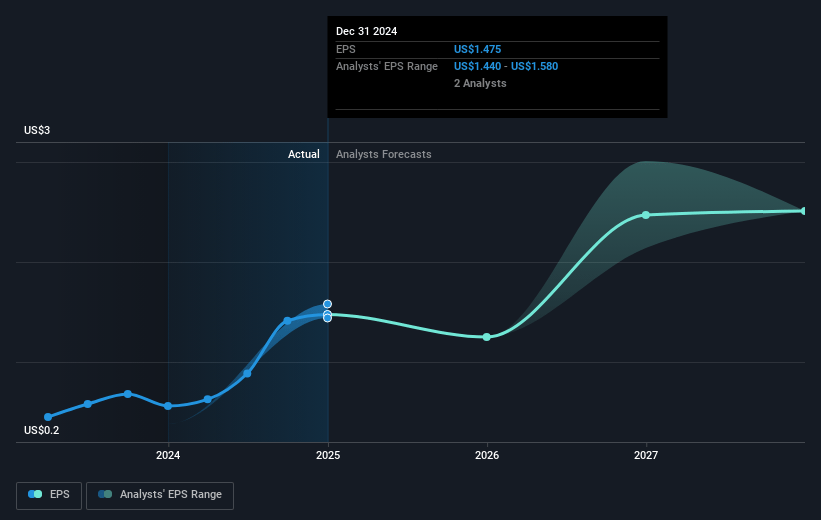

Eldorado Gold Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The successful ramp-up and on-schedule progress at the Skouries project, with disciplined contingency planning for labor and equipment, positions Eldorado Gold to meaningfully grow production and transition to free cash flow generation over the next year, which could positively impact both revenue and margins.

- Sustained high gold prices, currently at record levels, have allowed Eldorado to offset higher production costs and maintain strong profitability, suggesting that if this pricing environment persists due to global macro trends, Eldorado's future earnings and free cash flow may remain robust.

- The company's ongoing capital investments at operating mines and continuous operational optimizations-including cost control at Kisladag and Lamaque-are facilitating higher throughput and efficiency improvements, which have the potential to reduce costs per ounce and improve net margins in the long term.

- Enhanced financial flexibility from a strong liquidity position and proactive capital allocation strategies, such as the expanded normal course issuer bid (NCIB) for share buybacks, demonstrate management's confidence in undervaluation and the long-term value proposition, directly benefiting shareholder returns and potentially supporting share price appreciation.

- The company's demonstrated ability to resolve operational disruptions, as seen by the quick recovery at Olympias and targeted process improvements across sites, highlights resilient asset management that could lead to more stable or rising production and more consistent earnings performance going forward.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Eldorado Gold is CA$26.58, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Eldorado Gold's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$40.73, and the most bearish reporting a price target of just CA$26.58.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be $2.6 billion, earnings will come to $682.9 million, and it would be trading on a PE ratio of 7.2x, assuming you use a discount rate of 7.0%.

- Given the current share price of CA$28.01, the bearish analyst price target of CA$26.58 is 5.4% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.