Key Takeaways

- Innovative insurance products for conservation areas and non-financed equipment could expand the customer base and boost revenue.

- Digital transformation investments enhance efficiency and distribution, supporting net margin and revenue growth.

- Volatile interest rates and macroeconomic shifts are impacting net financial income, potentially hindering profitability and growth in net earnings due to increased costs and declining revenues.

Catalysts

About BB Seguridade Participações- Through its subsidiaries operates in the insurance, pension plans, and bonds, businesses in Brazil.

- BB Seguridade is innovating in new insurance products, like insurance for natural conservation areas and insurance for non-financed equipment, which could boost revenue by expanding the customer base and offering unique products.

- The company is focused on improving the customer experience and retention, as evidenced by the reduction in churn by 15.2% and the increase in customers with multiple products by 9.5%, which could enhance revenue and net margins by increasing customer lifetime value.

- Continued strong performance in higher-margin insurance lines like credit life and crop insurance, combined with historically low loss ratios, could further improve net margins and earnings.

- Investment in digital transformation and analytical maturity should enhance operational efficiencies and distribution capabilities, potentially improving net margins and driving revenue growth.

- The anticipated stabilization of interest rates and associated financial markets could lead to improved financial income and lower volatility, potentially boosting overall net income and earnings per share.

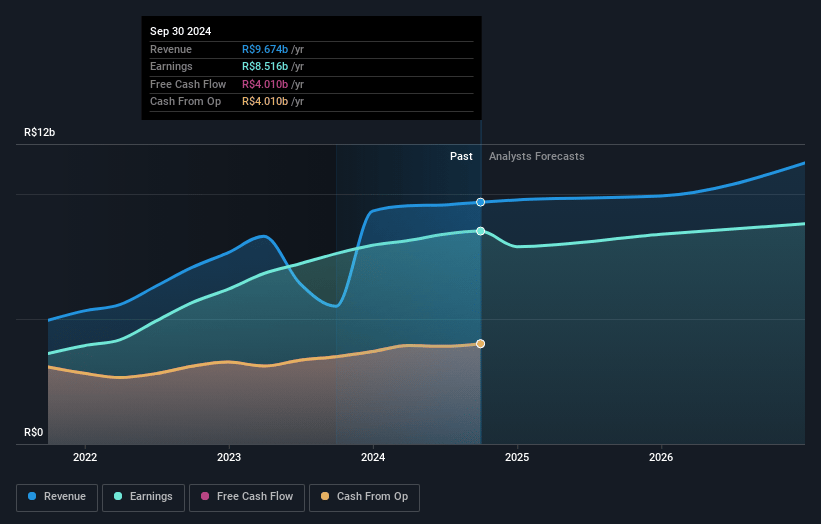

BB Seguridade Participações Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming BB Seguridade Participações's revenue will grow by 5.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from 88.0% today to 88.3% in 3 years time.

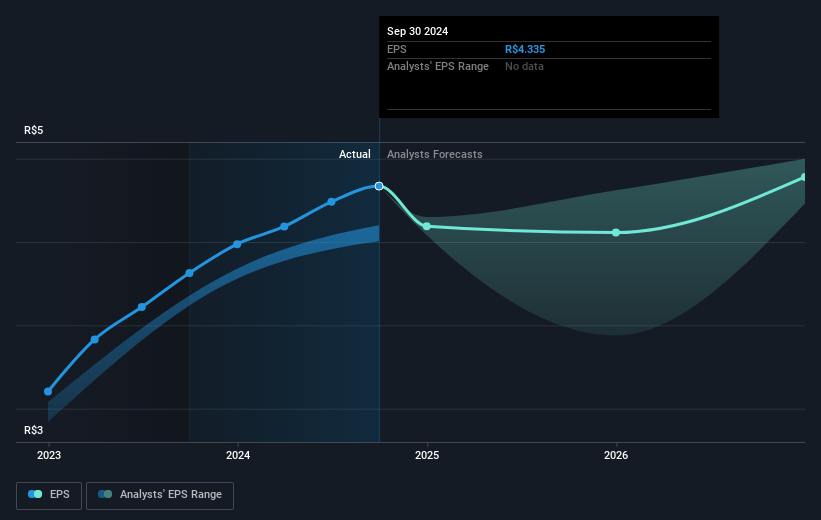

- Analysts expect earnings to reach R$9.9 billion (and earnings per share of R$4.97) by about January 2028, up from R$8.5 billion today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.1x on those 2028 earnings, up from 8.9x today. This future PE is greater than the current PE for the BR Insurance industry at 8.9x.

- Analysts expect the number of shares outstanding to grow by 0.81% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 16.64%, as per the Simply Wall St company report.

BB Seguridade Participações Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The financial results were negatively impacted by the opening in interest rate structures, which caused a mark-to-market loss on assets linked to inflation. This adversely affected financial revenues, decreasing them by 16% year-on-year. This could lead to decreased net earnings if this trend continues.

- The rural insurance segment, a significant part of the premiums written, saw a decline with crop insurance dropping by 32%. This underperformance in rural insurance could hinder revenue growth if it persists into following periods.

- There were more expenses associated with commission payments, which, while beneficial for brokerage revenues, can decrease net margins as higher commissions translate into higher costs for the insurance firm.

- Volatility in interest rates led to increased financial expenses, particularly affecting net financial income tied to long-term planning products. This could continue to impact earnings negatively if the volatile interest rate environment persists.

- The drop in net financial income was linked to shifts in the macroeconomic environment, such as interest rate and inflation dynamics. A continuation of this could put pressure on the company’s profitability and impact its ability to maintain previous growth in net income.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of R$41.0 for BB Seguridade Participações based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$46.0, and the most bearish reporting a price target of just R$34.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be R$11.2 billion, earnings will come to R$9.9 billion, and it would be trading on a PE ratio of 13.1x, assuming you use a discount rate of 16.6%.

- Given the current share price of R$39.03, the analyst's price target of R$41.0 is 4.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

Warren A.I. is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by Warren A.I. are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that Warren A.I.'s analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Read more narratives

AV

AvelinoMorais

Community Contributor

Valor justo

Narrativa do Valor Justo O valor justo da BB Seguridade reflete sua posição de destaque no setor de seguros no Brasil e sua capacidade de continuar a gerar fluxos de caixa sólidos. A empresa está bem posicionada para se beneficiar da crescente demanda por seguros e produtos de previdência, mas deve navegar com cuidado em um ambiente regulatório e econômico desafiador.

View narrativeR$47.94

FV

16.9% undervalued intrinsic discount18.83%

Revenue growth p.a.

0users have liked this narrative

0users have commented on this narrative

0users have followed this narrative

6 months ago author updated this narrative