Key Takeaways

- Declining alcohol consumption, regulatory pressures, and increased competition threaten Ambev's revenue, margins, and ability to premiumize its brand portfolio.

- Heavy reliance on Brazil exposes Ambev to currency and political risks, while underperforming flagship brands signal potential long-term market share losses.

- Strong brand portfolio, digital transformation, disciplined management, and favorable demographics position Ambev for continued growth in revenue, margins, and shareholder returns despite competitive pressures.

Catalysts

About Ambev- Through its subsidiaries, engages in the production, distribution, and sale of beer, draft beer, carbonated soft drinks, malt and food, other alcoholic beverages, and non-alcoholic and non-carbonated products in Brazil, Central America and Caribbean, Latin America South, and Canada.

- Structural declines in alcohol consumption, especially among younger consumers across Latin America, are accelerating, undermining Ambev's core revenue base and threatening long-term top-line growth as the health and wellness trend intensifies.

- Escalating regulatory and taxation pressures on alcoholic beverages in key markets such as Brazil and Argentina will drive up production and distribution costs, directly compressing gross and net margins even as the company invests in efficiency.

- Ambev's heavy dependence on the Brazilian market exposes it to persistent currency volatility and unpredictable economic or political shocks, creating a significant risk of sharp revenue and earnings swings that cannot be mitigated by portfolio performance alone.

- The persistent underperformance and failure to reverse declining momentum in legacy flagship brands like Skol, despite management interventions, indicate potential long-term market share erosion, limiting pricing power, and stalling premiumization-driven ASP growth.

- Intensifying competition from global brewers, local craft entrants, and the rapid consumer shift towards low

- and no-alcohol alternatives are expected to erode Ambev's market share in its strongest segments, constraining both volume growth and EBITDA margin expansion over the next several years.

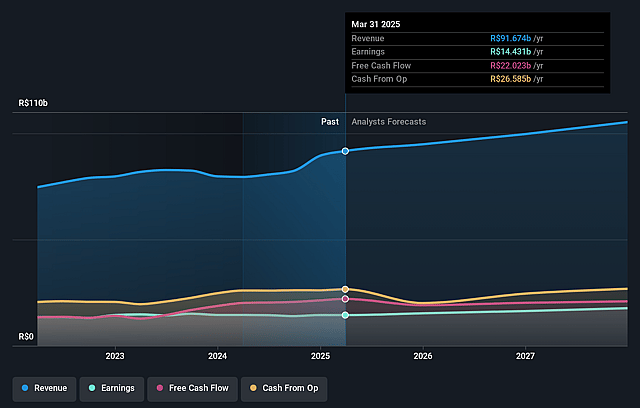

Ambev Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Ambev compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Ambev's revenue will grow by 4.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 15.7% today to 16.0% in 3 years time.

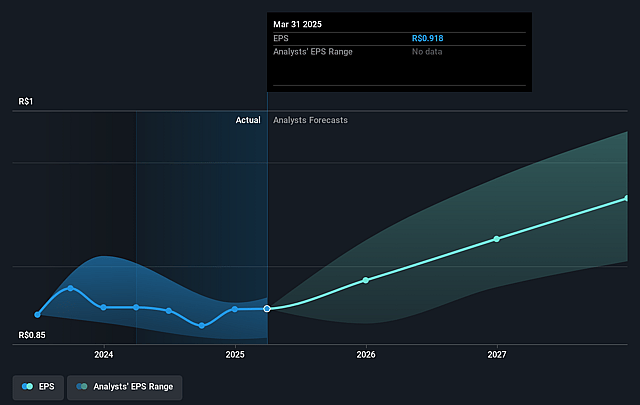

- The bearish analysts expect earnings to reach R$16.6 billion (and earnings per share of R$1.06) by about July 2028, up from R$14.4 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 11.4x on those 2028 earnings, down from 14.5x today. This future PE is lower than the current PE for the US Beverage industry at 14.5x.

- Analysts expect the number of shares outstanding to decline by 0.5% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 17.32%, as per the Simply Wall St company report.

Ambev Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Resilient volume growth and record volumes in key markets like Brazil, combined with strong double-digit increases in premium and non-alcoholic brands, point to a robust demand environment that could support sustained revenue and EBITDA growth over the long term.

- Continued investment and success in digital transformation-with platforms like BEES and Zé Delivery driving higher customer engagement, improved data analytics, and direct-to-consumer innovation-strengthen Ambev's competitive edge and could expand both revenue and operating margins over time.

- Strategic focus on portfolio diversification, including premiumization and the growth of non-alcoholic and above-core brands, increases addressable markets and creates pricing power, which can drive higher average selling prices and support gross margin expansion.

- Financial discipline reflected by strong cash flow generation, prudent capital allocation (with substantial dividends and share buybacks), and ongoing focus on operational productivity increases the likelihood of steady or improving net income and earnings per share, even amid cost headwinds.

- Positive secular and demographic trends in core Latin American markets, such as a youthful population, rising middle class, and continued cultural relevance of beverage consumption, suggest sustained high single-digit top-line growth potential that could contradict expectations of a declining share price.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Ambev is R$7.62, which represents two standard deviations below the consensus price target of R$13.7. This valuation is based on what can be assumed as the expectations of Ambev's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$17.0, and the most bearish reporting a price target of just R$3.12.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be R$104.2 billion, earnings will come to R$16.6 billion, and it would be trading on a PE ratio of 11.4x, assuming you use a discount rate of 17.3%.

- Given the current share price of R$13.4, the bearish analyst price target of R$7.62 is 75.8% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.