Key Takeaways

- Declining demographics and rising demand for alternative credentials threaten traditional enrollment and revenue growth.

- Limited geographic presence and increasing competition expose the company to volatile earnings and shrinking profitability.

- Robust growth in high-demand courses, improved operational efficiency, expanding medical offerings, prudent debt management, and strong cash generation position the company for sustained earnings and financial flexibility.

Catalysts

About Ser Educacional- Develops and manages activities for on-campus and distance-learning undergraduate, graduate, and professional training courses and other education-related areas in Brazil.

- Despite recent enrollment growth, Ser Educacional's core addressable market is facing a long-term reduction due to declining population growth and aging demographics in Brazil, which will likely shrink the pool of prospective university-age students. This negative trend is poised to dampen medium-to-long-term revenue growth for its traditional degree programs.

- The accelerating adoption and legitimacy of alternative, non-degree educational pathways such as micro-credentials, online certifications, and vocational training is expected to erode demand for traditional higher education offerings-especially as employers shift hiring criteria-which will both reduce revenues and put downward pressure on margins.

- Ser Educacional's business remains heavily concentrated in Brazil, leaving it exposed to regional economic downturns, regulatory changes, and persistent socioeconomic volatility in Latin America. This limited geographic diversification could drive earnings volatility and undermine overall earnings stability in the future.

- Technology-driven disruptors and new edtech entrants offering lower-cost, more flexible learning solutions are set to intensify competitive pressures, forcing Ser Educacional to increase spending on student acquisition and retention, discount tuition fees, or invest significantly in digital infrastructure, all of which are likely to erode net margins and profitability.

- The company is at risk of rising regulatory scrutiny and increasing compliance costs as educational standards evolve, particularly for for-profit operators, which is expected to add direct pressure to Ser Educacional's operating costs and further compress net margins over time.

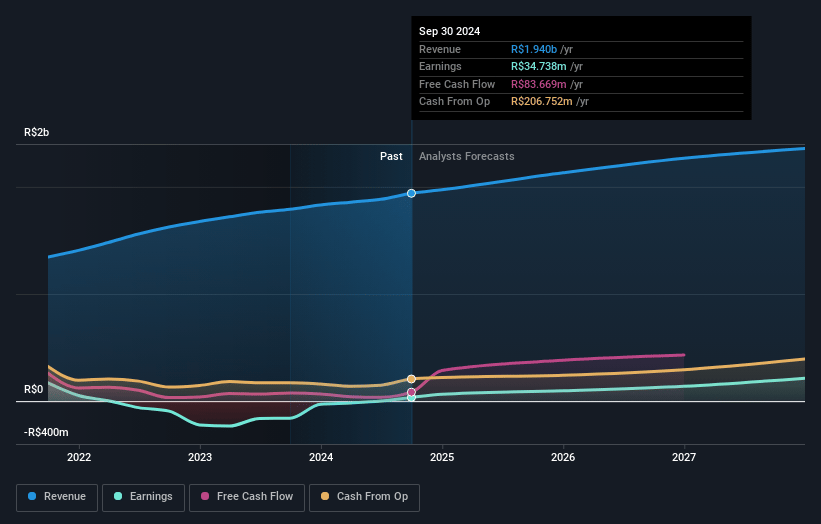

Ser Educacional Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Ser Educacional compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

- The bearish analysts are assuming Ser Educacional's revenue will grow by 5.7% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 2.9% today to 8.2% in 3 years time.

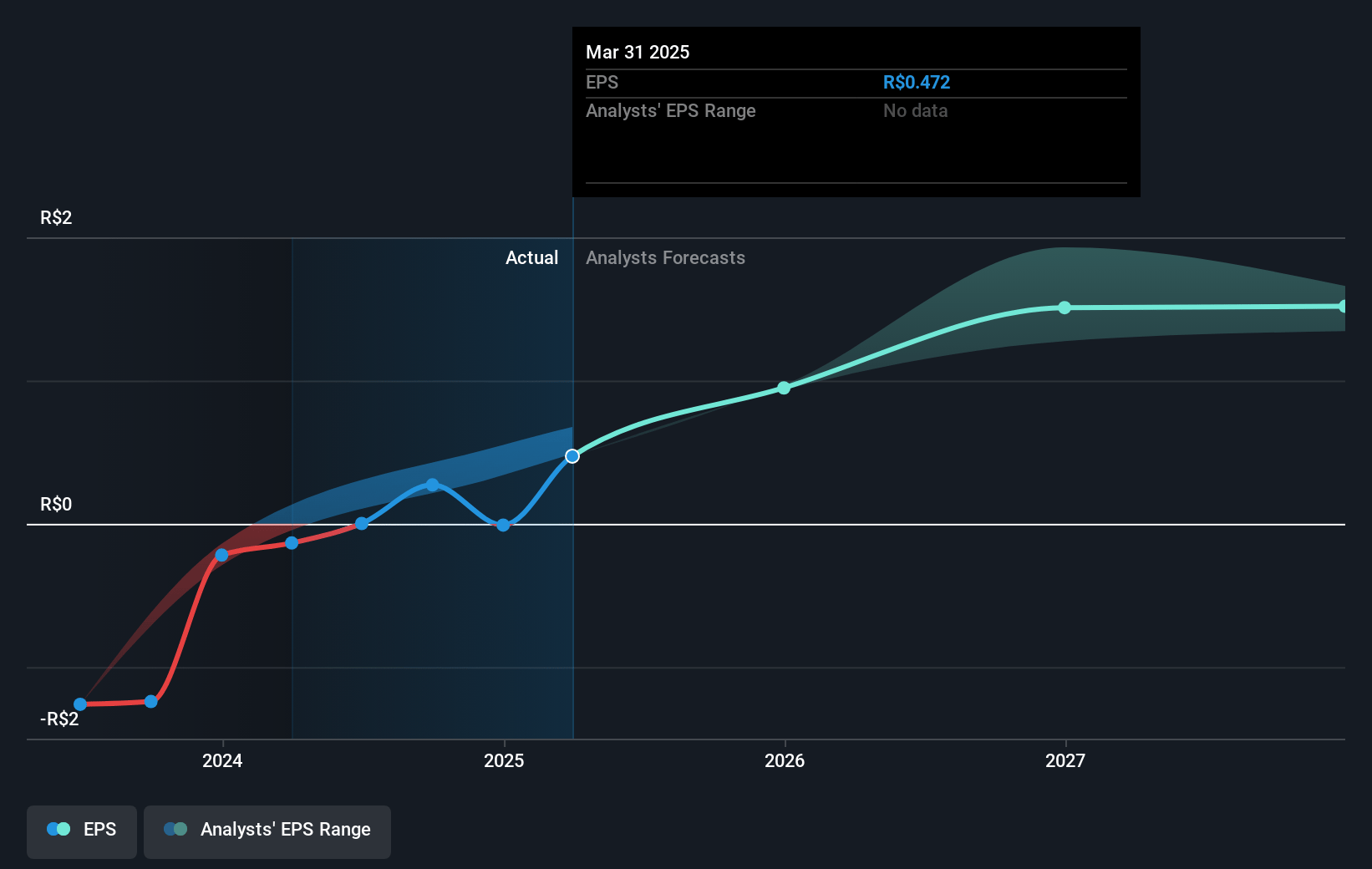

- The bearish analysts expect earnings to reach R$201.1 million (and earnings per share of R$1.58) by about July 2028, up from R$60.0 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 5.5x on those 2028 earnings, down from 17.4x today. This future PE is lower than the current PE for the BR Consumer Services industry at 11.1x.

- Analysts expect the number of shares outstanding to decline by 1.34% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 21.98%, as per the Simply Wall St company report.

Ser Educacional Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Consistent multi-year growth in both student intake and enrollment, particularly in high-demand hybrid and medical courses, indicates a robust demand environment that supports steady or rising revenues over the medium to long term.

- Strengthening operational efficiency, including cost optimization via real estate rationalization and integration of the Ubiqua digital system, is translating into improved EBITDA and expanded net profit margins, which could drive sustained earnings growth even in a competitive market.

- Successful expansion of medical course offerings, with new accreditations and high student demand, positions the company within a premium, high-ticket educational segment, suggesting ongoing margin enhancement and increased revenue visibility as these new student cohorts mature over coming years.

- A solid deleveraging trend, with net debt to adjusted EBITDA reduced to 1.35 times and a clear commitment to further debt reduction, provides greater financial flexibility and the potential to increase shareholder returns through dividends, directly benefiting net income and capital returns.

- Strong improvement in cash generation from operations, supported by enhanced tuition collection and disciplined working capital management, signals healthy underlying business fundamentals that support reinvestment, growth initiatives, and resilience in earnings.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Ser Educacional is R$5.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Ser Educacional's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of R$14.0, and the most bearish reporting a price target of just R$5.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be R$2.4 billion, earnings will come to R$201.1 million, and it would be trading on a PE ratio of 5.5x, assuming you use a discount rate of 22.0%.

- Given the current share price of R$8.24, the bearish analyst price target of R$5.0 is 64.8% lower. Despite analysts expecting the underlying buisness to improve, they seem to believe the market's expectations are too high.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.