Key Takeaways

- Expansion into the U.K. and U.S. markets and strategic partnerships aim to boost revenue growth and market share.

- AI integration and innovative media partnerships target increased efficiency, brand recognition, and reduced marketing costs.

- Heavy reliance on media partnerships and expansion costs in key markets pose risks to revenue growth and net earnings stability.

Catalysts

About Airtasker- Engages in the provision of technology-enabled online marketplaces for local services in Australia.

- Airtasker's expansion into the U.K. and U.S. markets represents a significant growth opportunity, with both regions experiencing substantial revenue growth. This expansion is expected to drive future revenue and potentially enhance long-term earnings as the company gains market share in these new territories.

- The innovative media partnerships Airtasker has secured offer a scalable way to boost brand recognition without upfront cash outflows, thus enhancing marketing efficiency and potentially leading to increased revenue growth as these investments begin to pay off.

- Recent investments in brand awareness and marketplace trust have started to demonstrate positive impacts, with increases in brand awareness and customer consideration. These efforts are expected to provide long-term revenue growth by reducing dependency on costly performance advertising channels like Google.

- Airtasker's collaboration with OpenAI to integrate AI into customer service and marketplace operations aims to enhance customer experience and operational productivity. Effectively leveraging AI could improve operating margins by increasing efficiency and reducing costs.

- The strategic partnership with the VCARB Formula One team is designed to increase Airtasker's global brand presence. This partnership is likely to drive higher customer engagement and, subsequently, revenue growth across key markets, given the large viewership and publicity associated with Formula One.

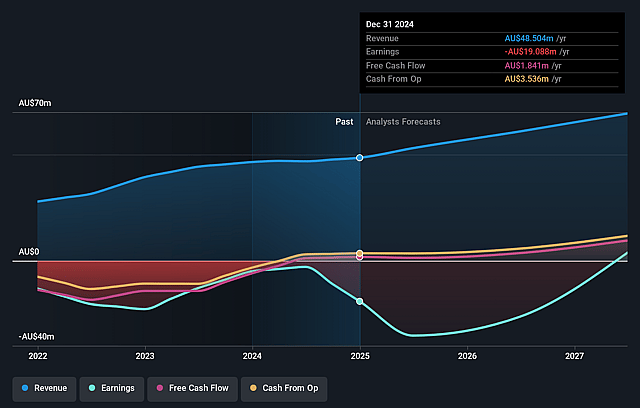

Airtasker Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Airtasker's revenue will grow by 15.4% annually over the next 3 years.

- Analysts are not forecasting that Airtasker will become profitable in next 3 years. To represent the Analyst Price Target as a Future PE Valuation we will estimate Airtasker's profit margin will increase from -39.4% to the average AU Interactive Media and Services industry of 29.7% in 3 years.

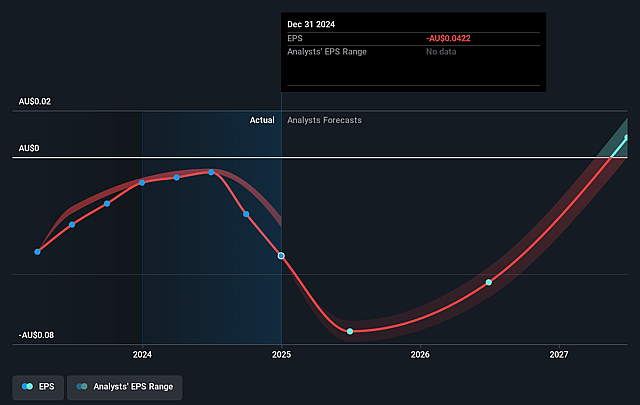

- If Airtasker's profit margin were to converge on the industry average, you could expect earnings to reach A$22.1 million (and earnings per share of A$0.05) by about August 2028, up from A$-19.1 million today.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 13.3x on those 2028 earnings, up from -9.0x today. This future PE is lower than the current PE for the AU Interactive Media and Services industry at 51.7x.

- Analysts expect the number of shares outstanding to grow by 0.23% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.62%, as per the Simply Wall St company report.

Airtasker Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The significant EBITDA loss due to the mark-to-market valuation of media partnership obligations, coupled with the impact of foreign currency fluctuations, represents a financial risk that could affect net earnings if these liabilities further increase.

- The heavy reliance on media partnerships and the associated variable marketing spend might create uncertainty in future revenue growth if media campaigns do not deliver expected results, impacting revenue expectations.

- The U.K. and U.S. market expansions are currently unprofitable, with negative EBITDA driven by marketing investments, indicating risk to net margins if these markets do not reach profitability within a reasonable timeframe.

- The competitive landscape, especially in Australia, and the evolving nature of digital advertising costs could pressure Airtasker's margins if unaided brand awareness does not convert into sustainable organic growth, thus affecting earnings.

- The share purchase liabilities and potential fluctuations in revenue multiples present financial uncertainty, leading to volatility in financial reporting and creating risk to net earnings stability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$0.515 for Airtasker based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$0.75, and the most bearish reporting a price target of just A$0.23.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$74.5 million, earnings will come to A$22.1 million, and it would be trading on a PE ratio of 13.3x, assuming you use a discount rate of 7.6%.

- Given the current share price of A$0.38, the analyst price target of A$0.52 is 26.2% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.