Key Takeaways

- Expansion of core operations and exploration success are set to drive output growth and strengthen future cash flow.

- Shifting to resilient, high-margin underground mining and disciplined cost management should boost profit margins and long-term stability.

- Overreliance on high-cost operations, project uncertainties, and limited geographic diversification expose future earnings and production to operational, regulatory, and industry-related risks.

Catalysts

About Regis Resources- Engages in the exploration, evaluation, and development of gold projects in Australia.

- Sustained investor demand for gold amid global inflationary pressures and geopolitical instability is likely to support higher realized gold prices over the long term, which directly benefits Regis Resources' top-line revenue and earnings potential.

- Advancing production ramp-up at core operations like Duketon and Tropicana, combined with ongoing exploration success at Rosemont and near-term contributions from new satellite pits, positions the company for incremental output growth and enhanced cash flow over coming years.

- Transition toward more resilient, high-margin underground production and disciplined cost control is expected to improve the company's all-in sustaining cost (AISC) profile, supporting margin expansion and profitability as higher-grade underground mines come online.

- Successful resolution or permitting of the McPhillamys Gold Project could unlock a major, long-life, low-cost asset, significantly raising future production visibility and adding stability to long-term free cash flow generation.

- The sector-wide scarcity of new gold discoveries and declining global reserve bases may increase the strategic value of Regis Resources' expanding reserve inventory, providing potential upside to asset valuations and underlying net asset value per share.

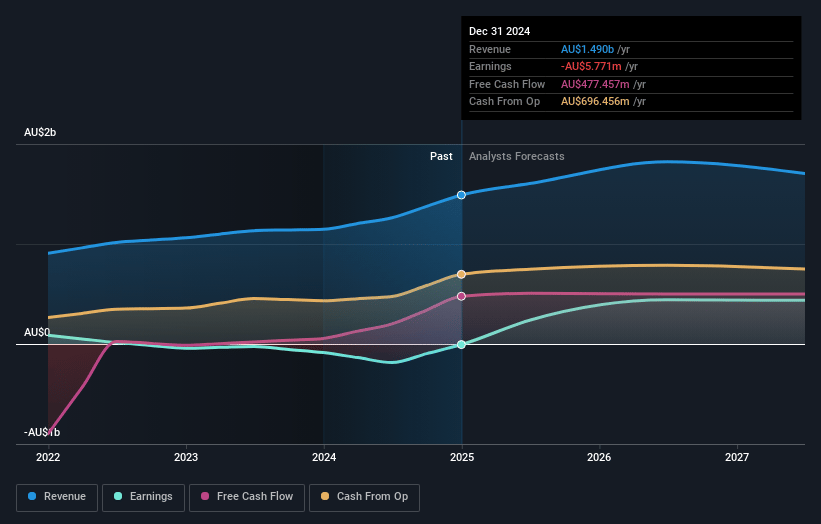

Regis Resources Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Regis Resources's revenue will grow by 5.0% annually over the next 3 years.

- Analysts assume that profit margins will increase from -0.4% today to 23.2% in 3 years time.

- Analysts expect earnings to reach A$400.6 million (and earnings per share of A$0.56) by about July 2028, up from A$-5.8 million today. However, there is a considerable amount of disagreement amongst the analysts with the most bullish expecting A$590.9 million in earnings, and the most bearish expecting A$119.9 million.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 10.4x on those 2028 earnings, up from -584.1x today. This future PE is lower than the current PE for the AU Metals and Mining industry at 13.1x.

- Analysts expect the number of shares outstanding to grow by 0.08% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.21%, as per the Simply Wall St company report.

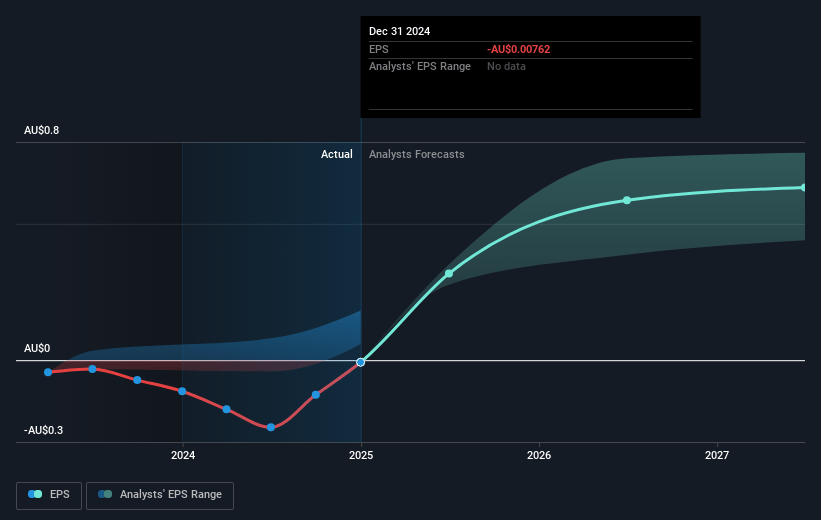

Regis Resources Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Ongoing industry-wide inflationary pressures, with cost escalation cited at 4–5%, are driving Regis' all-in sustaining cost (AISC) guidance higher, especially as the company exploits opportunistic, higher-cost ounces-pressuring net margins and exposing earnings to any stagnation or decline in the gold price.

- Heavy near-term reliance on processing stockpiles and small, high-cost satellite pits at Duketon, many of which are approaching depletion within 2 years, risks a drop in production volumes, and unless backed by new discoveries or successful exploration, could negatively impact future revenues and cash flow.

- The regulatory and permitting uncertainty at the McPhillamys project remains a material risk; prolonged legal challenges or unfavorable outcomes could stall or eliminate a major long-life growth asset, reducing long-term production visibility and growth in earnings.

- ESG-related challenges, exemplified by McPhillamys' permitting delays and ongoing efforts to seek alternative tailings solutions, are likely to intensify industry scrutiny and compliance requirements, potentially raising future capital costs, delaying project approvals, and compressing profit margins.

- High asset concentration in Western Australia, with key projects such as Duketon and Tropicana, leaves Regis vulnerable to local operational, regulatory or environmental disruptions, resulting in greater revenue volatility and long-term earnings risk compared to more geographically diversified peers.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$4.445 for Regis Resources based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$5.3, and the most bearish reporting a price target of just A$3.1.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$1.7 billion, earnings will come to A$400.6 million, and it would be trading on a PE ratio of 10.4x, assuming you use a discount rate of 7.2%.

- Given the current share price of A$4.46, the analyst price target of A$4.44 is 0.3% lower. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.