Last Update 22 Aug 25

Fair value Increased 16%The upward revision in Ridley’s price target reflects increased analyst optimism driven by higher forecast revenue growth and an expanded future P/E multiple, resulting in a new consensus fair value of A$3.21.

What's in the News

- Ridley Corporation announced a fully franked ordinary dividend of AUD 0.05 per share for the six months ended June 30, 2025.

- The company repurchased zero shares and spent AUD 0 million on share buybacks in the first half of 2025, completing no share repurchases under the previously announced buyback.

- CFO Richard Betts will step back from full-time executive roles, with Chris Opperman set to be appointed CFO after supporting the integration of the Incitec Pivot Fertilisers acquisition; Opperman brings extensive experience from Incitec Pivot and Energy Australia.

Valuation Changes

Summary of Valuation Changes for Ridley

- The Consensus Analyst Price Target has risen from A$3.00 to A$3.21.

- The Future P/E for Ridley has significantly risen from 20.38x to 24.65x.

- The Consensus Revenue Growth forecasts for Ridley has risen from 24.2% per annum to 25.5% per annum.

Key Takeaways

- Diversification through fertilizer and premium pet food, plus portfolio streamlining, strengthens revenue stability, margin growth, and operational efficiency.

- Strategic focus on innovation, regulatory compliance, and international expansion positions Ridley for sustained market share gains and elevated earnings.

- Expansion into fertilizers and volatile agribusiness markets heightens operational complexity, supply risk, and margin pressure, while persistent industry headwinds challenge sustained earnings growth.

Catalysts

About Ridley- Engages in the provision of animal nutrition solutions in Australia the United States, New Zealand, and Thailand.

- Ridley's expansion into fertilizer distribution through the acquisition of Incitec Pivot Fertilisers and its integration plans will further diversify revenue streams, strengthen supply chain resilience, and increase exposure to domestic food security initiatives, supporting long-term revenue growth and margin stability.

- Structural growth in protein demand from rising middle classes in Asia and Africa, combined with Ridley's focus on value-added feed products (including recent innovations and international market expansion, such as new pet food opportunities in Asia), is likely to drive sustained volume and margin growth across key segments.

- The company's deliberate portfolio reset-exiting lower-return operations, streamlining costs, and reinvesting in modernization (including a new OMP facility and supply chain efficiencies)-will enhance operating leverage and net margins in future periods.

- Ongoing momentum towards premiumization in pet food, combined with capacity repurposing at Narangba and the launch of Oceania Petfood Solutions, will shift more sales to higher-margin products, supporting margin expansion and top-line growth.

- Sector-wide trends favoring established players with compliance records-such as rising regulatory standards in feed safety and increasing ESG scrutiny-position Ridley to consolidate share and secure premium pricing, benefitting long-term earnings and net margins.

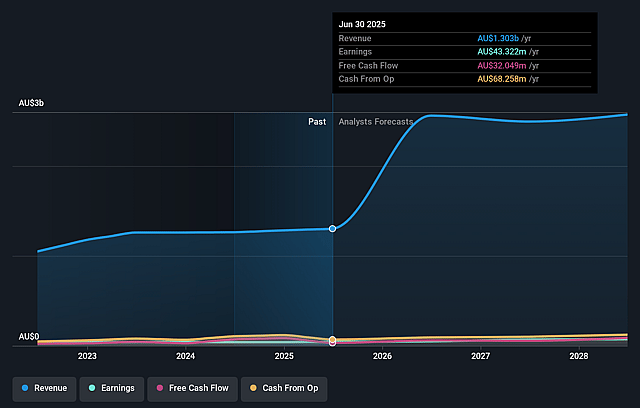

Ridley Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Ridley's revenue will grow by 36.1% annually over the next 3 years.

- Analysts assume that profit margins will shrink from 3.3% today to 2.5% in 3 years time.

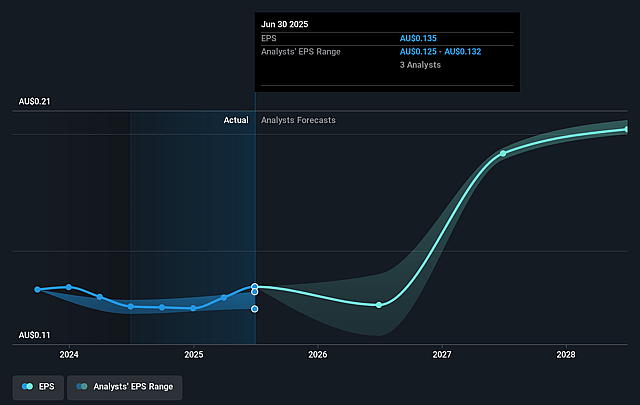

- Analysts expect earnings to reach A$80.6 million (and earnings per share of A$0.22) by about September 2028, up from A$43.3 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 24.0x on those 2028 earnings, down from 28.5x today. This future PE is greater than the current PE for the AU Food industry at 14.6x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 6.48%, as per the Simply Wall St company report.

Ridley Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The integration of Incitec Pivot Fertilisers entails significant supply chain complexity and longer commodity shipping cycles compared to Ridley's core feed business; this exposes the company to elevated price and supply volatility in global fertilizer markets, which could negatively affect long-term revenue stability and net margins.

- Ongoing depressed prices for poultry meal and meat and bone meal due to export restrictions and domestic oversupply are creating earnings headwinds-there is no clear timeline for market normalization, suggesting that ingredient recovery margins and Packaged and Ingredients segment earnings remain under pressure in the medium term.

- Revenue growth in Bulk Stockfeeds during FY '25 was heavily aided by supplementary feeding demand driven by drought conditions in southern Australia-this supplementary demand is highly variable and not a reliable long-term earnings driver, increasing the risk of revenue and EBITDA decline if weather returns to more typical conditions.

- Company-acknowledged operational constraints, such as limited processing capacity following volume gains from partners like A.J. Bush and the need for ongoing debottlenecking investments, introduce risks of underutilised assets and operational inefficiencies, which can weigh on net margins if not fully resolved.

- The business model's expansion into fertilizer distribution increases Ridley's exposure to geopolitical, macroeconomic, and regulatory risks affecting global fertilizer trade (e.g., import disruptions, compliance costs, environmental regulation changes), potentially leading to input cost inflation, higher working capital demands, and reduced overall earnings predictability.

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$3.493 for Ridley based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$4.0, and the most bearish reporting a price target of just A$3.0.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$3.3 billion, earnings will come to A$80.6 million, and it would be trading on a PE ratio of 24.0x, assuming you use a discount rate of 6.5%.

- Given the current share price of A$3.29, the analyst price target of A$3.49 is 5.8% higher. The relatively low difference between the current share price and the analyst consensus price target indicates that they believe on average, the company is fairly priced.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.