Last Update01 May 25Fair value Decreased 0.062%

Key Takeaways

- Diversification through acquisitions and expanding investment offerings strengthens revenue base and enhances growth potential across global markets.

- Strategic focus on performance fee-eligible assets and growth opportunities positions company for scalable earnings and improved net margins.

- Reliance on performance fees, acquisition strategy, and competition for clients could introduce volatility and pressure on revenue growth and margins.

Catalysts

About Regal Partners- A privately owned hedge fund sponsor.

- Record net inflows of $1.9 billion in 2024, with 30% coming from offshore investors, signifies a sustained demand for Regal Partners' investment offerings. This development indicates potential future revenue growth from expanding global exposure and increased performance fee eligibility.

- The acquisition of Merricks Capital and Argyle has diversified the company's asset classes and increased its Funds Under Management (FUM) to $18 billion. The expansion and diversification potentially strengthen the revenue base while enhancing net margins through a broader range of income sources.

- Regal Partners' strategic focus on growing performance fee eligible assets, with $8.7 billion of FUM close to high watermark, positions the company to capture more performance fees, positively impacting future earnings.

- The company is proactively pursuing further organic and inorganic growth opportunities, which could bolster FUM and revenues. This strategic approach may lead to increased scalability and improved net margins over time.

- The launch of new strategies and discrete mandates since listing has added $2.2 billion to current FUM. Continued innovation in product offerings may sustain or enhance near-term revenue and earnings growth.

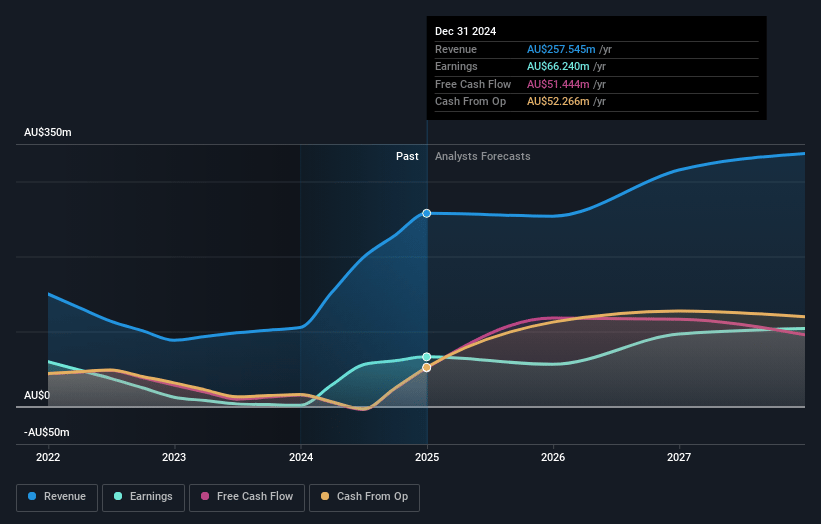

Regal Partners Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- Analysts are assuming Regal Partners's revenue will grow by 9.4% annually over the next 3 years.

- Analysts assume that profit margins will increase from 25.7% today to 30.8% in 3 years time.

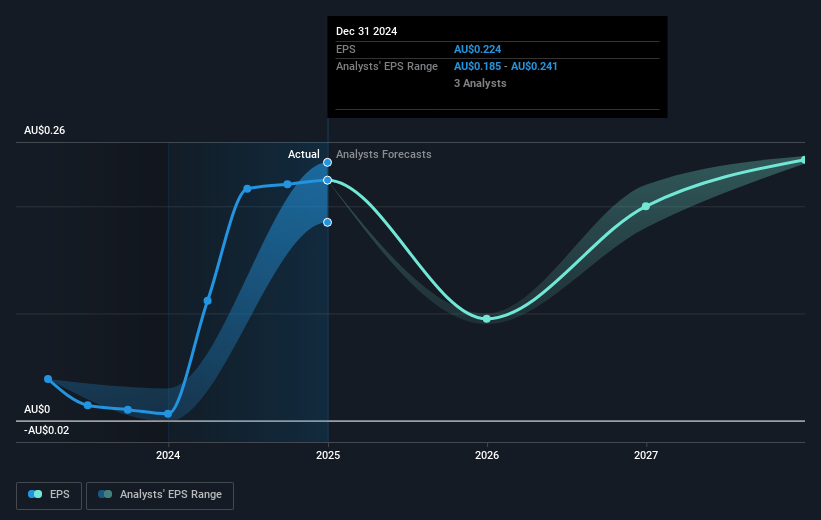

- Analysts expect earnings to reach A$103.9 million (and earnings per share of A$0.24) by about May 2028, up from A$66.2 million today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the analysts price target, the company would need to trade at a PE ratio of 19.6x on those 2028 earnings, up from 9.5x today. This future PE is greater than the current PE for the AU Capital Markets industry at 14.4x.

- Analysts expect the number of shares outstanding to grow by 7.0% per year for the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 7.11%, as per the Simply Wall St company report.

Regal Partners Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- The company's reliance on performance fees, which contributed significantly to revenue in 2024, can introduce volatility to earnings if future performance does not meet expectations or market conditions change. (Earnings)

- The decrease in average management fees from the second half of 2024 due to product mix diversification and acquisitions may indicate pressure on future revenue growth from this stream unless volume offsets the rate decline. (Revenue)

- There is a risk that the company’s ambitious acquisition strategy, while offering growth opportunities, might lead to integration challenges and hidden costs that could impact overall profitability. (Net Margins)

- The competition for offshore clients, despite successful fundraising efforts, may lead to longer gestation periods and increased expenses in marketing and distribution efforts, which could put downward pressure on margins. (Net Margins)

- Continued acquisitions, while beneficial for diversification, may lead to increased intangible asset values and potential goodwill impairments if anticipated synergies or market conditions do not materialize as expected. (Earnings)

Valuation

How have all the factors above been brought together to estimate a fair value?- The analysts have a consensus price target of A$4.037 for Regal Partners based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of A$5.9, and the most bearish reporting a price target of just A$3.3.

- In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$337.4 million, earnings will come to A$103.9 million, and it would be trading on a PE ratio of 19.6x, assuming you use a discount rate of 7.1%.

- Given the current share price of A$1.88, the analyst price target of A$4.04 is 53.6% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystConsensusTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystConsensusTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystConsensusTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.