Key Takeaways

- Ongoing economic volatility, inflation, and dollarization threaten loan growth, deposit stability, and recurring revenue despite regulatory reforms and macroeconomic improvements.

- Digital transformation boosts efficiency and customer growth, but fierce fintech competition and changing client behavior may limit future income and market expansion.

- Persistent macroeconomic volatility, credit risks, increasing fintech competition, and regulatory uncertainty threaten profitability, margin stability, and future growth prospects for the bank.

Catalysts

About Banco BBVA Argentina- Provides various banking products and services to individuals and companies in Argentina.

- While macroeconomic stabilization and regulatory reforms are expected to improve Argentina's financial environment and stimulate greater demand for formal banking, the persistent risk of renewed economic volatility and high inflation could continue to erode real asset values and suppress loan quality, hindering long-term loan growth and recurring revenue.

- Although BBVA Argentina's investment in digital transformation has enabled impressive growth in digital customer acquisition and operational efficiencies that should support net margin improvement, the rapid advance of agile fintech competitors may accelerate disintermediation, particularly among younger or underbanked segments, limiting fee-based income and slowing customer growth over time.

- While the relaxation of foreign exchange controls and rising cross-border capital flows have driven a surge in FX-related business and created new revenue channels, increased dollarization and ongoing Argentine preference for hard currency could shrink the local currency loan book and fee-pool, potentially dampening both interest income and non-interest earnings.

- Even though demographic growth and a rising middle class present a substantial opportunity to expand the customer base and drive deposit and loan growth, the chronic tendency toward dollarization and capital flight in response to political or macro shocks could undermine long-term deposit stability and restrict scalable revenue growth.

- Despite BBVA Argentina's improved credit risk management and cautious portfolio expansion into higher-margin segments, episodes of rising nonperforming loans-particularly in retail credit-and historically low provision coverage rates suggest that sustained credit expansion may require higher future provisioning, threatening profitability and causing downward pressure on net earnings.

Banco BBVA Argentina Future Earnings and Revenue Growth

Assumptions

How have these above catalysts been quantified?- This narrative explores a more pessimistic perspective on Banco BBVA Argentina compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts.

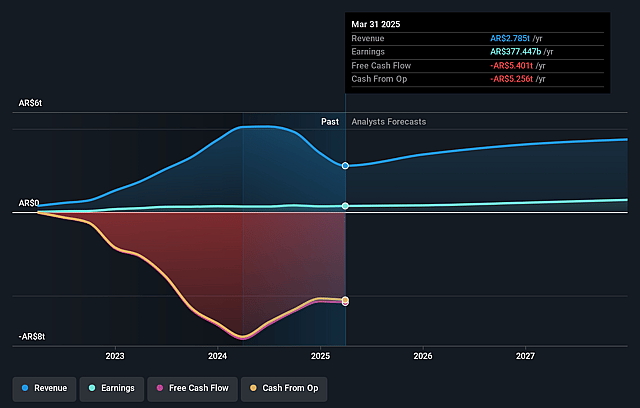

- The bearish analysts are assuming Banco BBVA Argentina's revenue will grow by 30.4% annually over the next 3 years.

- The bearish analysts assume that profit margins will increase from 12.1% today to 16.9% in 3 years time.

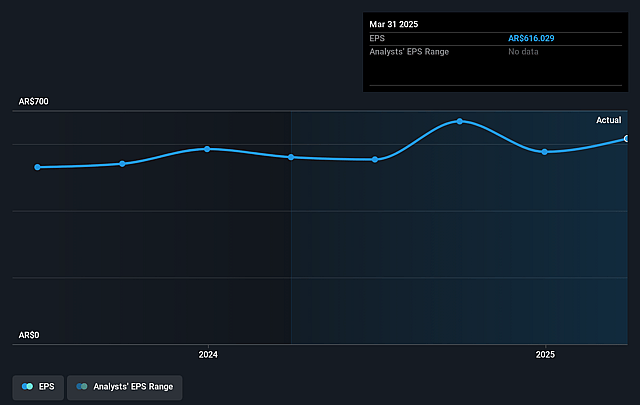

- The bearish analysts expect earnings to reach ARS 870.3 billion (and earnings per share of ARS 3.71) by about September 2028, up from ARS 279.5 billion today. The analysts are largely in agreement about this estimate.

- In order for the above numbers to justify the price target of the more bearish analyst cohort, the company would need to trade at a PE ratio of 12.0x on those 2028 earnings, up from 10.2x today. This future PE is greater than the current PE for the US Banks industry at 10.2x.

- Analysts expect the number of shares outstanding to remain consistent over the next 3 years.

- To value all of this in today's terms, we will use a discount rate of 25.81%, as per the Simply Wall St company report.

Banco BBVA Argentina Future Earnings Per Share Growth

Risks

What could happen that would invalidate this narrative?- Persistently high inflation and volatile interest rates in Argentina continue to pressure loan demand and increase operating costs, potentially leading to reduced net interest margins and lower profitability over the long term.

- Rising non-performing loans in the retail segment and historically low provision coverage ratios raise the risk of higher credit losses, threatening to erode net earnings and require increased provisioning expenses in the future.

- The shift to short-term instruments and treasury operations with rapid repricing creates exposure to sudden interest rate changes, which can negatively affect net interest income if deposits reprice more quickly than loans.

- Accelerated adoption of digital financial services and increased competition from fintechs may lead to margin compression and loss of market share, particularly in high-growth, low-cost segments, thereby reducing fee income and future revenue growth.

- The ongoing risk of regulatory changes, such as capital control relaxations or renewed restrictions, as well as evolving public sector exposure, underscores inherent uncertainties that can constrain the bank's ability to manage its balance sheet efficiently and depress overall returns.

Valuation

How have all the factors above been brought together to estimate a fair value?- The assumed bearish price target for Banco BBVA Argentina is ARS8540.0, which represents the lowest price target estimate amongst analysts. This valuation is based on what can be assumed as the expectations of Banco BBVA Argentina's future earnings growth, profit margins and other risk factors from analysts on the more bearish end of the spectrum.

- However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of ARS15200.0, and the most bearish reporting a price target of just ARS8540.0.

- In order for you to agree with the bearish analysts, you'd need to believe that by 2028, revenues will be ARS5135.7 billion, earnings will come to ARS870.3 billion, and it would be trading on a PE ratio of 12.0x, assuming you use a discount rate of 25.8%.

- Given the current share price of ARS4655.0, the bearish analyst price target of ARS8540.0 is 45.5% higher.

- We always encourage you to reach your own conclusions though. So sense check these analyst numbers against your own assumptions and expectations based on your understanding of the business and what you believe is probable.

How well do narratives help inform your perspective?

Disclaimer

AnalystLowTarget is a tool utilizing a Large Language Model (LLM) that ingests data on consensus price targets, forecasted revenue and earnings figures, as well as the transcripts of earnings calls to produce qualitative analysis. The narratives produced by AnalystLowTarget are general in nature and are based solely on analyst data and publicly-available material published by the respective companies. These scenarios are not indicative of the company's future performance and are exploratory in nature. Simply Wall St has no position in the company(s) mentioned. Simply Wall St may provide the securities issuer or related entities with website advertising services for a fee, on an arm's length basis. These relationships have no impact on the way we conduct our business, the content we host, or how our content is served to users. The price targets and estimates used are consensus data, and do not constitute a recommendation to buy or sell any stock, and they do not take account of your objectives, or your financial situation. Note that AnalystLowTarget's analysis may not factor in the latest price-sensitive company announcements or qualitative material.