“Every once in a while, a new technology, an old problem, and a big idea turn into an innovation.” - Dean Kamen

This week we are having a look at another key secular trend: the transition to clean energy and the electrification of the global economy. We touched on some of the relevant industries in May , but there’s a lot more to cover, so let’s take a deeper look.

🎧 Would you prefer to listen to these insights? Checkout the audio recording on Spotify and Apple Podcasts !

The Accelerating Clean Energy Transition

The transition to cleaner sources of energy is not only a secular trend, but one that appears to be accelerating. There are three major reasons that this is occurring now:

- Energy Independence: The war in Ukraine and its effect on Europe’s energy supply has highlighted the risk of relying on other countries for energy needs.

- Climate Change: There’s an increased sense of urgency around climate change - the current heat waves around the world are another reminder.

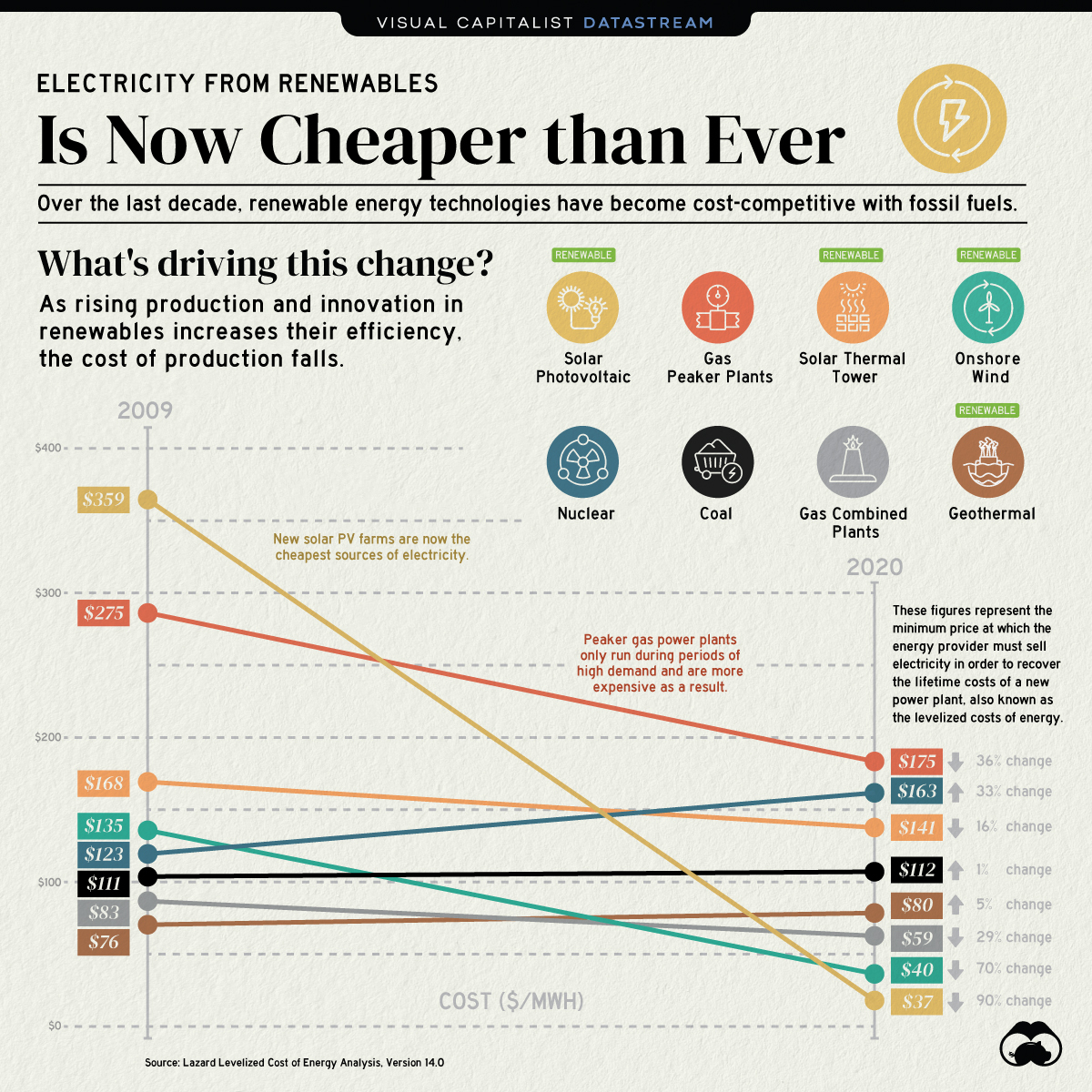

- Economics: By 2020, solar photovoltaic and onshore wind had become the cheapest forms of energy to finance. It took a lot of subsidies to get to that point, but renewable energy now makes sense from a business standpoint alone.

Energy Costs by Source 2009 to 2020 - Image Credit: Visual Capitalist

Some analysts believe that 2022 was a pivotal year and may have marked the peak in oil demand. This has been incorrectly predicted in the past, so don’t read too much into that.

What we do know is that the mix of generating capacity is tilting quickly toward renewables.

We also know that there’s a long way to go before the world can stop relying on fossil fuels, but the key word here is ‘transition’. We cannot sustain our current usage of fossil fuels environmentally or in terms of resources.

If we can achieve a mix of both renewable and fossil fuels that is sustainable for the long-term, then that’s a good place to be before a full energy transformation takes place.

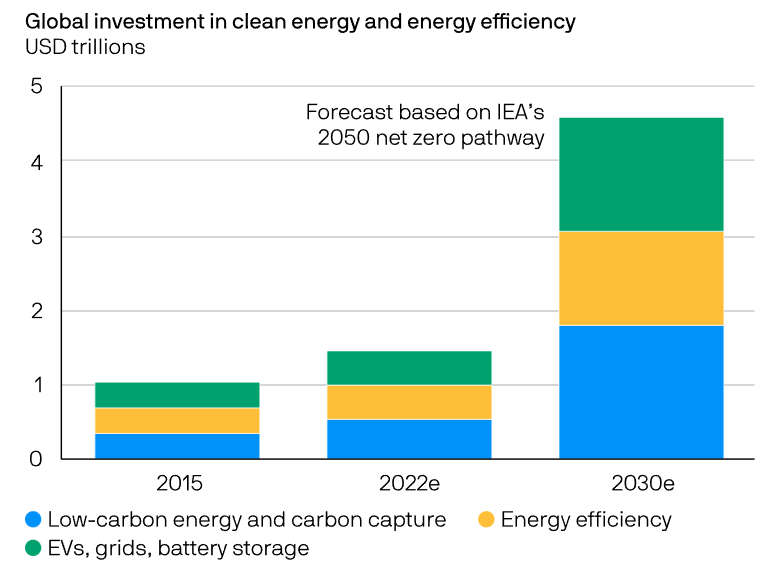

This chart from JP Morgan Asset Management shows how much would need to be invested by 2030 to stay on the ‘net zero by 2050’ scenario. That may seem like a pipe dream, but if the urgency increases it may happen sooner than we expect.

Global Investment in Clean Energy and Generation - Image Credit: JP Morgan Asset Management

As investors, we want to find companies that can generate above average returns AND that have the opportunity to reinvest profits for years and decades to come.

The energy transition is an ideal environment to find opportunities like this - and there are lots of industries to investigate. Broadly speaking they fit into three categories:

- Electrification

- Generation

- Storage

Electrification (and EVs)

If the world is going to use electricity from renewable sources, the demand side needs to be electrified. Most of the energy used for transport, manufacturing industries, and the heating and cooling of buildings still comes from oil, gas and coal. This consumption needs to be converted to electricity before the supply can come from renewable resources like wind and solar.

In May, we discussed electricity infrastructure and the HVAC (heating, ventilation, and air conditioning) industries that play an important role here. Electric vehicles are the well known face of this transition, thanks to the rapid success of Tesla and other EV makers.

Tesla and BYD are the world leaders in the EV space, and way ahead of smaller pure play competitors like Nio , Li Auto and Rivian . But most of the world’s legacy automakers are now also competing in the EV space.

The EV industry is caught between two competing narratives.

The bearish perspective is that while growth is a certainty, competition will drive margins down to the low single digits for those competing in the space. As Warren Buffett said recently when asked about EVs: “the auto industry is just too tough.”

The more bullish narrative is that EVs (led by Tesla) are ushering in a world of autonomous vehicles, and in particular, autonomous ride hailing services. If this happens, vehicles become income producing assets. It could also mean that demand will outpace supply for years to come and margins will remain at current levels.

Investors will need to weigh up these two narratives and the likely timelines, but there are other ways to invest indirectly. One is via the lithium battery industry (which we’ll cover shortly) and the other is by investing in companies that supply other components. Chip makers like NXP , STMicroelectronics , Onsemi and AMD are all key suppliers to the EV industry.

BorgWarner Inc is an interesting and lesser known company. The company historically supplied products used by legacy, hybrid and electric automakers. It’s now divesting from legacy assets to focus on EV related products.

Generation

Solar and Wind

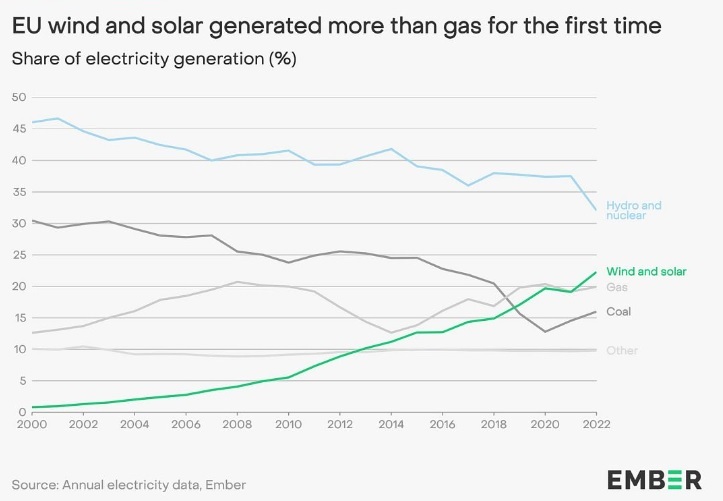

In 2022, wind and solar generation provided 22% of the EU’s electricity, edging out both gas and coal. Many countries now have ambitious targets to increase the share of energy generated from solar and wind projects. As an example, the Inflation Reduction Act in the US includes $369 billion for renewable energy generation.

EU Electricity Generation by Source - Image Credit: Morningstar

We mentioned the solar industry in May, so what about wind?

Wind energy generally involves industrial projects (rather than residential) with large upfront capital requirements. The advantage of wind is the fact that it's not confined to daylight hours. Ultimately, most governments are pursuing both.

From an investors point of view, both industries can offer opportunities to investors. The wind industry is diverse and includes multinational utility scale operators, independent power producers, and the companies that design, manufacture, install and service turbines.

Wind turbines are getting bigger too, the world’s largest has a diameter of 850 feet, or 259 meters! So logistics is an increasingly important part of the value chain.

This Wind Energy Stocks list includes companies operating throughout the wind energy value chain.

Storage

Storing energy created from renewable sources remains the biggest challenge.

Both solar and wind energy is intermittent, which means electricity needs to be stored for later use. Until this problem can be solved at a price that makes sense, alternatives are needed to provide baseload energy.

This problem also offers the greatest potential for innovation, and billions are being invested to drive that innovation.

The EV revolution is driving demand for lithium-ion batteries, which in turn is driving demand for lithium, cobalt, nickel and graphite. These batteries are becoming very efficient and several EVs now have ranges above 500 km. The downside is that they are very expensive. Our Battery Stocks Collection highlights six key battery and lithium companies if you’re interested in this angle on the narrative.

Currently the best alternative is hydrogen, which has applications beyond transport and residential installations. Hydrogen is produced using energy from any other source, and then later converted back into electricity by combining it with oxygen in a fuel cell. Green hydrogen is produced from renewable sources, while ‘blue’ hydrogen is produced from natural gas with the CO2 emitted being captured and stored.

Hydrogen is relatively light but takes up more space than lithium-ion batteries.

This means it's better suited to trucks and potentially for industrial applications. The downside of hydrogen is that it's relatively inefficient as energy is lost during its production and again when it is converted into electricity.

Despite its drawbacks hydrogen can be used to store energy for baseload generation and for industrial use. Equinor is currently building a hydrogen pipeline from Norway to Germany to supply blue, and later green hydrogen.

In the US Air Products , Bloom Energy and Plug Power are key players in the hydrogen industry.

There are actually lots of ways to store energy. Current experiments include hot sand, liquid air, and gravity systems in disused mine shafts . The challenge is making them cost effective and practical.

We haven't covered everything here, so in a future newsletter we’ll have a look at nuclear, hydro electric power and pumped storage, carbon credits and trading, and carbon capture.

💡 The Insight: Investing in the Energy Transition

Here are a few thoughts on investing in the energy transition:

- Keep an eye on regulations and policy. Regulations have held a lot of projects back, but things can change quickly when policy changes.

- The energy transition is likely to include a mix of solutions (including fossil fuels) for a long time. It’s worth looking at a few different industries.

- MSCI’s thematic indexes are a useful resource for finding companies in energy industries, as well as other secular trends. The index fact sheets typically list the largest 10 companies in each index.

Once you’ve found a stock (or multiple) that are within this big trend and set to benefit from it continuing to develop, it’s important to have a narrative built around each investment which can be used to justify a purchase decision, and then monitor the stock.

Here’s a structure that may help you organise your thoughts while you research a stock.

- Catalysts

- What are the key drivers of my narrative around this stock?

- These are typically qualitative and high level developments that you think will drive growth in the business and can range from catalysts that are quite presumptive/explorative or they can be relatively grounded in supporting facts/figures.

- Catalysts can relate to the company specifically, or just the industry in general.

- For example, one catalyst on a solar stock might be: “ Based on research by JP Morgan , investment in renewable energy sources by governments and industry will need to increase significantly over the coming decades to reach global emissions targets, and X stock is well positioned to continue to benefit from this trend since it is the industry leader in the solar space and already has a large pipeline of work lined up.”

- Assumptions

- To quantify the magnitude of the catalyst

- Here you then will try and provide an well informed estimate for the magnitude of each catalyst you have surrounding a stock, based on your research. This is to avoid airy fairy forecasts of “Solar is going to be huge, therefore X will benefit”. You have not grounded that assumption with a quantitative estimate, and therefore it can be very hard to track as it plays out. The key here is it doesn’t need to be precise, just an estimate.

- For example, your assumption on the previous catalyst might be: “ Global spending on solar investment from governments and industry is expected to reach $xbn by 2030. X stock currently has a market share of 30%, but I expect it will slightly lose market share over the coming years due to new competition, and it will decrease to around 25%. Therefore I believe it could generate revenues of $Xbn by 2030.”

- Risks

- What could prevent the catalysts above from playing out as expected?

- It’s important to consider the other side of the coin, and think about future outcomes in probabilities, rather than binary “right / wrong” scenarios.

- For example: “There is a risk that the industry forecasts don’t play out as expected, due to new innovations in other energy sources being more efficient, or the transition simply occurring slower than expected. This would result in my future revenue figures being lower. However, given the R&D up to this point, current reliance on solar, and continued efficiency gains, I don’t believe there is a high likelihood that solar will be replaced or superseded by alternative innovations, and it will continue to be a major energy source into the future.

- Valuation

- What do I think the business is worth, based on my expectations of its future prospects.

- There are many ways to conduct a valuation, but all involve figuring out a price to pay based on a company’s future prospects. One method is you can envision that future scenario where the company is generating a certain amount in revenue and profits that you think is likely by a certain year, and then estimate what it would be trading at based on those metrics, and discount that value back to today.

- For example: “ Based on my expectations, I believe X stock will generate $xbn in revenue by 2030, and $Xbn in profits by that year. Based on its 10 year average PE ratio of 20x, I assume it will have a market value of $Ybn (i.e. 20x * profits). When I discount that future value back at 9% per year (my discount rate), I get an estimated present value of $Zbn, which is 30% above the current price. Therefore, I think the stock is currently undervalued.

With this process above, you now have more conviction in your decision (be it buy/hold/sell), because you came to the conclusion yourself, you have a valuation to anchor your buy/hold/sell decisions to, and you have a narrative and valuation to monitor as time develops. You know what you own, and why you own it.

This is investing, without all these, you’re simply speculating or investing emotionally.

What Else is Happening?

First a recap of the key data releases we mentioned last week…

- 🇺🇸 US: The Federal Open Market Committee raised the Fed Funds rate 0.25% to 5.5%. This was widely expected, but takes the interest rate to 5.5%, the highest it's been in 22 years. Fed Chair Jerome Powell didn’t add much to his previous statements, but did say: “I’m saying we would be comfortable cutting rates when we’re comfortable cutting rates, and that won’t be this year, I don’t think it would be”

And then, a few news items that we thought were worth noting…

-

Second quarter earnings from big tech companies got off to a decent start:

- Microsoft reported record sales and beat estimates. But growth from its cloud business continued to slow and the company lowered its forward guidance.

- Alphabet reported slightly better growth from its cloud business (which is smaller than Microsoft’s) and a strong recovery in search.

- Meta also impressed the market with better than expected results and optimistic guidance. The results were driven by very strong engagement with ads on Facebook and Instagram. On the other hand, Meta’s metaverse experiment continues to rack up losses (which isn’t to say they won’t pay off eventually).

- The common theme here is that the recovery in advertising is continuing, but businesses are being more cautious with their spending.

-

🇨🇳 China Evergrande Group is the distressed company at the center of China’s real estate crisis. But it's not only struggling with real estate. Its subsidiary, China Evergrande New Energy Vehicle Group , disclosed a $10 billion loss for 2021 and 2022 when it reported long overdue financials.

- Evergrande is trying to diversify into the automarket - but facing the same problem automakers have faced for the last 100 years. Consulting firm AlixPartners recently estimated that there are 167 EV brands in China, and only 25-30 can survive the decade.

Key Events During the Next Week

The focus this week will be a string of employment numbers in the US. The JOLTs job openings are due on Tuesday, followed by the ADP employment report on Wednesday and non farm payrolls and the unemployment rate on Friday.

Interest rate decisions are due for Australia on Tuesday and for the UK on Thursday.

It’s another monster week for quarterly earnings. These are some of the big names, but there are lots more reporting:

- Avis

- ON Semiconductor

- Yum China

- SoFi Technologies

- Pfizer

- AMD

- BP p.l.c.

- Uber Technologies

- Vertex Pharmaceuticals

- Qualcomm

- Shopify

- PayPal

- Occidental Petroleum

- Apple

- Amazon

- Alibaba

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.