What Happened in the Market Last Week?

Last week was a bit of a roller coaster for US markets with mid-term elections and inflation data driving the moves. When the US inflation data for October came in at 7.7% (below the expected 8%) investors loved the prospect of a less aggressive Fed, so markets rallied.

While it’s too early to tell, it was essentially evidence that inflation might finally be slowing, which is what the Fed said it needed to see in order to slow down the pace and size of rate increases.

Some of the developments we have been watching over the last week include:

- Commodity producers rallied amidst rumors of an end to China’s zero-Covid approach. While the rumors seem to be unfounded, there may be more to the relative strength of mining companies.

- Oil companies are making record profits as the shortage of capacity becomes increasingly apparent.

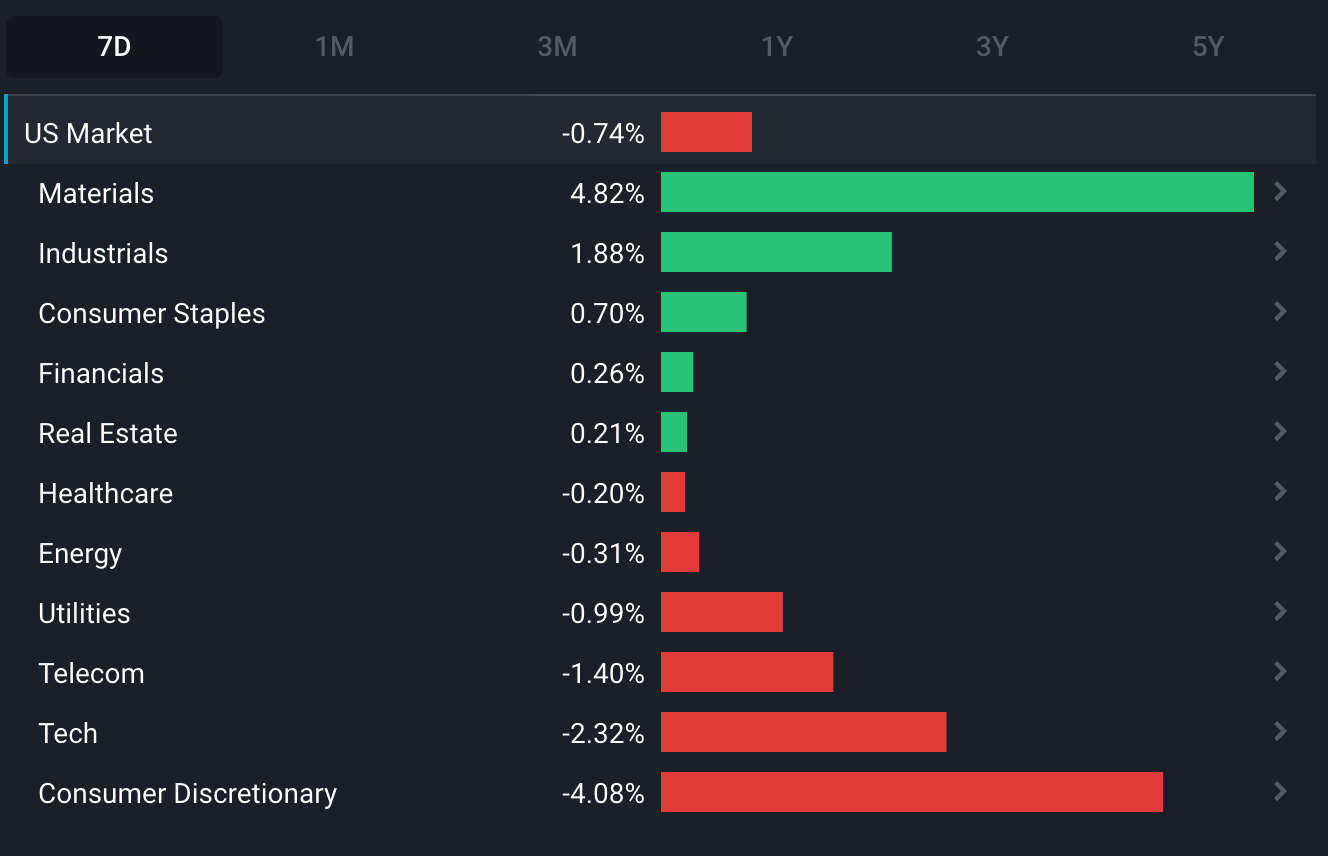

Commodity stocks are outperforming

The shares of commodity producers (and specifically industrial metal miners) like Rio Tinto (LSE:RIO) , Vale (BOVESPA:VALE3), Southern Copper (NYSE:SCCO), and Freeport-McMoRan (NYSE:FCX) woke up last week amid speculation that China will abandon its zero covid policy. Chinese officials have since denied the rumors , but it nevertheless shows just how sensitive commodity-related shares are to China’s economy.

The relative strength of commodity producers (both metals and energy stocks) over the last few weeks may also be related to the fact that the USD’s rally has paused. But some analysts also believe we are in the early stages of a new commodity super cycle . That may seem at odds with the current economic climate, particularly with regard to China’s economy. But, commodity cycles take a long time to evolve, and there are some reasons to believe a new super cycle is beginning.

Let’s have a look at how cycles play out in the commodity markets.

How do commodity cycles work?

The prices of commodities move in cycles that represent the relationship between supply and demand over time. A commodity cycle goes something like this: When demand for a commodity begins to outpace supply, the price of that commodity rises, and producers make higher margins. The higher margins incentivise more investment in production - ie. planting more crops, expanding mines, building refineries etc.

Eventually, with enough investment in increased production, supply catches up with demand and the price stops rising. But margins are still good, so producers carry on increasing their output - which ultimately leads to oversupply. Prices then begin to fall as producers compete with one another.

When the price falls far enough, output begins to fall too. In the case of agricultural commodities, farmers may simply choose to plant fewer crops. With metals, producers may shut down some mines and unprofitable producers may face bankruptcy. Prices stop falling when supply and demand are back in equilibrium. And then, when demand catches up with supply, the cycle starts again.

Of course, these cycles are also affected by other factors like the business cycle, the weather, labor disputes, supply chain dynamics and geopolitics, as we have seen in the last few years. The cycles followed by agricultural commodities are also closely related to weather patterns and seasonal demand. Nevertheless, the underlying cycle still occurs regardless of temporary factors.

What is a commodity super cycle?

Metals and energy commodities experience particularly long cycles, or super cycles, because of the capital-intensive nature of increasing production.

When prices are rising, there is a lag - that can last for years - between a company deciding to invest in a new project and that project becoming productive. This means it can take years for supply to catch up with demand.

When prices are falling, producers don’t simply stop producing. They usually hope the price slump will be temporary. So, they continue to produce despite falling margins, which keeps the pressure on the price. That means it takes longer for demand to catch up with supply.

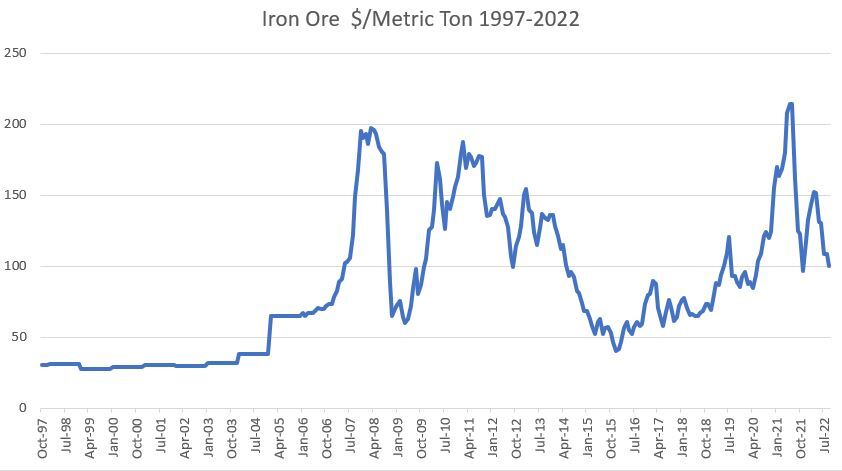

These dynamics create very long cycles. The chart below reflects the price of iron ore from 1997 to 2022. The period from 2001 to 2011 is generally regarded as the bullish phase of a super cycle (interrupted by the GFC). The phase from 2011 to 2019, was the bearish phase of the same cycle which resulted from oversupply.

In summary, the price rose by 550% and then fell 80% over an 18-year period. This chart is for iron ore specifically, but the prices of oil, copper, and other industrial commodities followed similar paths.

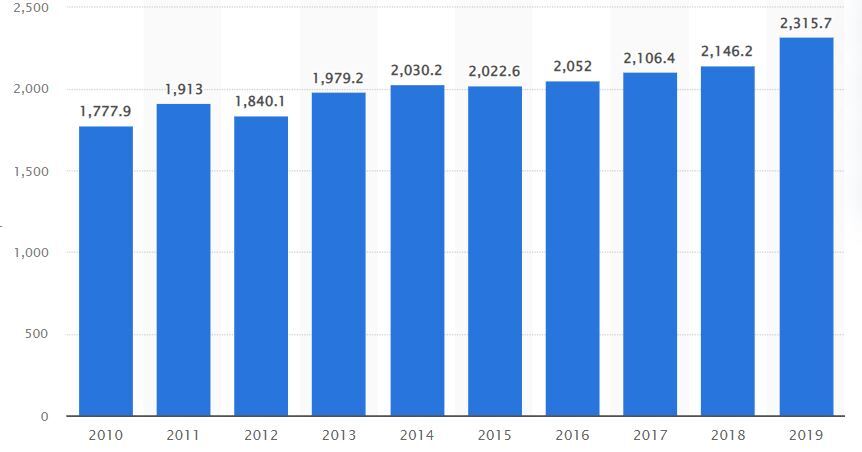

Looking at the chart above, you might assume there were large swings in production and consumption too. Au contraire - the chart below shows what global consumption looked like from 2010 to 2019, while the price fell as much as 80%. Global output followed a similar trend and was closely matched to demand. It only takes minor imbalances to move prices a long way.

The Insight: Not all commodity producers are created equal.

The Insight: Not all commodity producers are created equal.

As the global economy grows, annual consumption of commodities like oil and industrial metals rises steadily and seldom falls, even during a recession . The problem is that when commodity prices fall, producers stop investing in new productive capacity. In fact they tend to pay out any profits they do make as dividends to stop investors from selling their shares. Global capital expenditure by global mining companies was lower between 2016 and 2019 than it was during the GFC.

The massive spike in the iron ore price in 2021 was caused by supply chain issues, and the decline that followed was caused by the slowdown in China’s economy, and everything else that’s happened this year. But if forecasts come true, it seems that over the longer term, supply will inevitably catch up with demand. And that’s why analysts are calling for another super cycle.

For Short or Medium-Term Investors (< 5 years)

Regardless of the longer term cycle, commodities and the prices of commodity producers are still very sensitive to various factors:

- Expectations for global GDP growth and specifically China’s economy which has been the biggest consumer of commodities over the last 20 years. While consumption rises steadily over time, small changes in demand can have a big impact on prices in the short term.

- Inflation: Commodity prices generally rise with inflation. However, inflation also eats into the producers' margins in the form of higher energy and labor costs.

- The US dollar : Commodities are priced in USD, which can be a headwind when the USD appreciates relative to other currencies. However, it can also act as a tailwind for commodity demand when the USD weakens.

These factors have all played a role this year - and are likely to do so for the foreseeable future.

For Long-Term Investors (5+ years)

Commodity prices can move in persistent trends that last for years at a time. If you are investing in the shares of commodity producers, pay attention to these underlying trends, and where we might be in the cycle.

If the stock you’re looking at is a late-stage explorer or an early-stage producer without binding pricing contracts, it may not be able to survive a downturn in commodity prices unless it has enough cash on hand (so check the financial health of the business on our company report) . And if it doesn’t start production in the first few years of the supercycle, it won’t benefit as much as the established producers who are reaping those higher prices from early on.

But if you’re looking at those more mature producers, they typically have well-established production capacity and efficiencies that allows them to weather most kinds of slowdowns, and thrive during the booms.

So when looking at any commodity producer for the long term, it’s worth asking: where might we be in 5 or more years time (in terms of prices), and can this company survive any turbulence on the way there? (E.g. Do they have existing production capacity, diversity of commodities produced, and a strong cash balance?)

Oil companies are making record profits

We saw another consequence of the boom-bust nature of commodity cycles when two of America’s oil giants recently reported record profits. Exxon Mobil (NYSE: XOM) reported a record-setting $19.7 bln in quarterly net income, while Chevron (NYSE:CVX) wasn’t far behind with $11.2 bln. This prompted President Biden to propose a windfall profit tax on these companies if they don’t increase production. Biden wants lower prices for consumers, but the underlying problem runs a lot deeper. Energy companies have also underinvested in productive capacity over the last decade - and they have even less incentive than miners to do so.

Oil Capacity - Show me the incentive, and I’ll show you the action

There is general agreement that the world needs to move to renewable energy. But there isn’t enough renewable energy (or storage capacity) to make that happen just yet. At the same time, oil and gas companies have been told for years that their days are numbered and, now that prices are higher, that their excess profits will be taxed.

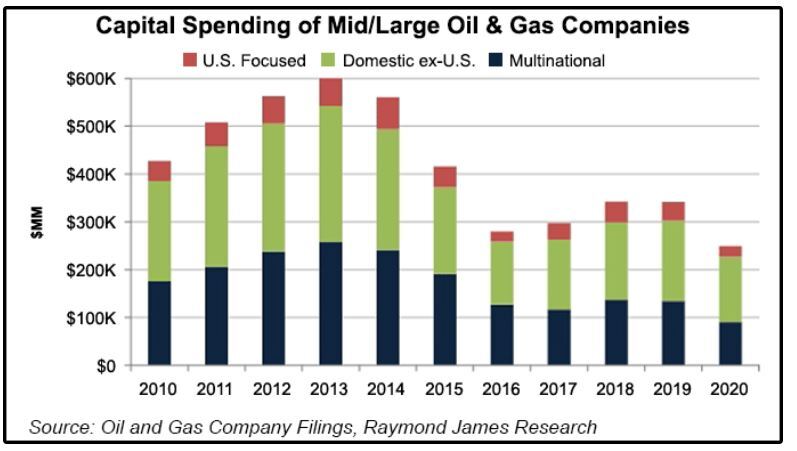

Put yourself in the shoes of an oil producer, and there was hardly any incentive to re-invest in new capacity over the last decade. This is why it should come as no surprise that we’ve seen falling investment since 2013. Capex (how much they’re investing) has picked up slightly now, but as we know, there’s quite a long lead time till they contribute to production, and this is what it looked like prior to 2020:

But wait, there’s more. On top of this, North America and Europe have fraught relationships with many of the world’s top energy producing countries (which fall under OPEC+). OPEC meanwhile is cutting production to prevent the oil price from falling.

The Insight: A little diversification never hurt anybody

Ultimately, the lack of capacity is at the heart of the problem. Russia’s war in Ukraine brought the problem to a head, but the West did little to increase its own capacity and production. This is the reason the US energy sector is up 50% over the last year, when the rest of the market is down more than 20%. Like industrial metals, some analysts believe the bull market in energy is just beginning , and it will take even higher energy prices to attract the investment that's needed to increase supply.

What this means for investors

Last week we looked at the second dot com bust that seems to be occurring. This week we’ve covered energy stocks that are up 50% over the last year, and the miners which have fallen 11%, but comfortably outperformed the market.

The last year has been a great example of the power of diversification. The US energy and US materials sectors can be quite unpredictable and volatile, but they are far less correlated to the broader market than other sectors. The remaining sectors are up during most years, but give back a lot of those gains during the occasional bear market. By spreading your portfolio across multiple sectors, you can reduce the overall volatility, which makes it a lot easier to sleep at night. If you’re looking for energy stocks, we’ve compiled a list of 6 energy stocks that benefit from rising energy prices .

Key Events Next Week

It’s a busy week for economic data in the UK with the unemployment rate, the inflation rate, a fiscal statement, and retail sales all due.

In the US the key release will be PPI on Tuesday. There is also retail sales data coming out on Wednesday and housing data due on Thursday and Friday.

Earnings season is winding down, but there are still a few large retailers and tech companies reporting this week. They include:

- Walmart (NYSE:WMT)

- Home Depot (NYSE:HD)

- Target (NYSE:TGT)

- Lowes (NYSE:LOW)

- Nvidia (Nasdaq:NVDA)

- Cisco (Nasdaq:CSCO)

- Alibaba (NYSE:BABA)

- Palo Alto (Nasdaq:PANW)

For next week:

- Democrats fared better than expected in the mid-term elections, but the GOP (Republicans) looks set to win control of the House of Representatives (at the time of writing).

US Elections went better than expected for Democrats - but still point to Gridlock

Democrats fared better than expected in last week's midterm elections, but still lost control of the House of Representatives and may lose control of the Senate, pending a runoff election.

Gridlock like this is generally considered a good thing for equity markets . When the presidency is in the hands of one party, and the other party has control of at least one of the houses of congress, there’s less chance of major legislation being passed. This leaves less room for uncertainty - and we know that markets don’t like uncertainty.

US equity markets also have a very good record in the period following midterm elections . In fact, the market has been higher a year later after the last 19 midterm elections - so a perfect record.

Will it be 20 out of 20? Possibly, but these types of relationships tend to work until they don’t, so perhaps not something to bet the house on.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.