Advertisement

- South Africa

- /

- REITS

- /

- JSE:BTN

Here's Why Burstone Group Limited's (JSE:BTN) CEO Compensation Is The Least Of Shareholders' Concerns

Key Insights

- Burstone Group's Annual General Meeting to take place on 2nd of September

- CEO Andrew Wooler's total compensation includes salary of R4.27m

- Total compensation is similar to the industry average

- Burstone Group's total shareholder return over the past three years was 17% while its EPS was down 130% over the past three years

Despite Burstone Group Limited's (JSE:BTN) share price growing positively in the past few years, the per-share earnings growth has not grown to investors' expectations, suggesting that there could be other factors at play driving the share price. These concerns will be at the front of shareholders' minds as they go into the AGM coming up on 2nd of September. They will be able to influence managerial decisions through the exercise of their voting power on resolutions, such as CEO remuneration and other matters, which may influence future company prospects. From the data that we gathered, we think that shareholders should hold off on a raise on CEO compensation until performance starts to show some improvement.

See our latest analysis for Burstone Group

Comparing Burstone Group Limited's CEO Compensation With The Industry

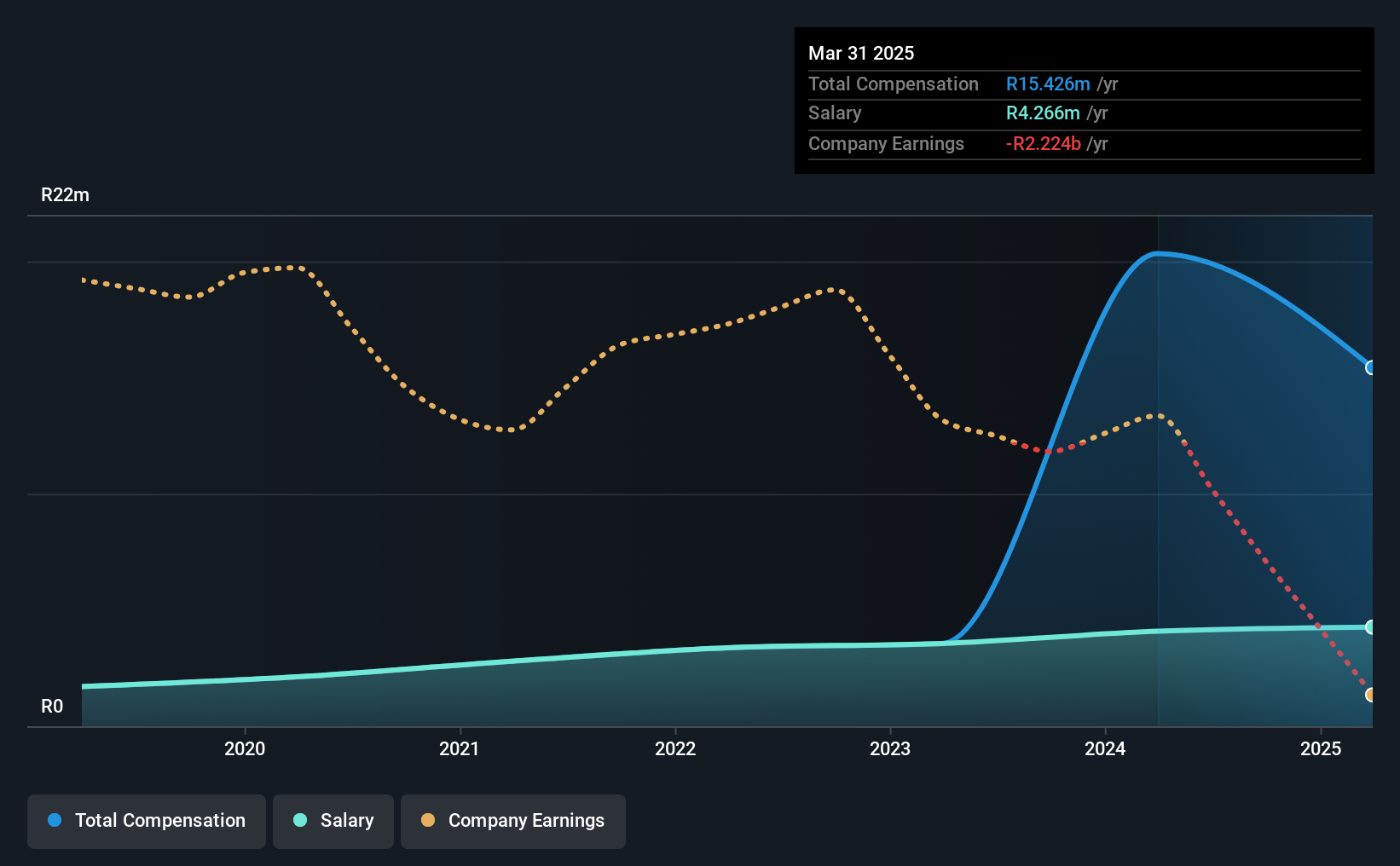

At the time of writing, our data shows that Burstone Group Limited has a market capitalization of R6.6b, and reported total annual CEO compensation of R15m for the year to March 2025. That's a notable decrease of 24% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at R4.3m.

On examining similar-sized companies in the South African REITs industry with market capitalizations between R3.5b and R14b, we discovered that the median CEO total compensation of that group was R13m. So it looks like Burstone Group compensates Andrew Wooler in line with the median for the industry. What's more, Andrew Wooler holds R5.1m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | R4.3m | R4.1m | 28% |

| Other | R11m | R16m | 72% |

| Total Compensation | R15m | R20m | 100% |

Talking in terms of the industry, salary represented approximately 33% of total compensation out of all the companies we analyzed, while other remuneration made up 67% of the pie. Burstone Group sets aside a smaller share of compensation for salary, in comparison to the overall industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Burstone Group Limited's Growth

Burstone Group Limited has reduced its earnings per share by 130% a year over the last three years. Its revenue is down 2.1% over the previous year.

Overall this is not a very positive result for shareholders. And the fact that revenue is down year on year arguably paints an ugly picture. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Burstone Group Limited Been A Good Investment?

Burstone Group Limited has served shareholders reasonably well, with a total return of 17% over three years. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

To Conclude...

Shareholder returns, while positive, should be looked at along with earnings, which have not grown at all recently. This makes us think the share price momentum may slow in the future. Shareholders should make the most of the coming opportunity to question the board on key concerns they may have and revisit their investment thesis with regards to the company.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 2 warning signs for Burstone Group that you should be aware of before investing.

Important note: Burstone Group is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Burstone Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:BTN

Burstone Group

A South African Real Estate Investment Trust, (REIT), which listed on the JSE in the Real Estate Holdings and Development Sector on 14 April 2011.

Fair value with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|7.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.4% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.6% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.0% undervalued

DA

Community Contributor