Advertisement

- United States

- /

- Electric Utilities

- /

- NYSE:PPL

Does PPL’s Grid Modernization Rate Hike Request Shift the Investment Thesis for PPL (PPL)?

Reviewed by Sasha Jovanovic

- PPL Electric Utilities recently filed its first distribution rate increase request in nearly a decade with the Pennsylvania Public Utility Commission, seeking to raise annual revenue by approximately US$356 million to fund grid modernization and smart-grid technology investments starting in mid-2026.

- This proposed rate hike, if approved, is designed to bolster the electric grid's resilience against severe weather, reduce outages, and strengthen operational reliability for both residential and business customers amid rising infrastructure needs.

- We'll examine how PPL's pursuit of regulatory approval for higher rates to fund grid upgrades may influence its long-term investment outlook.

Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

PPL Investment Narrative Recap

For a shareholder in PPL, the core thesis is that rising electricity demand, especially from data centers, and substantial infrastructure investment will drive long-term, regulated revenue growth and support consistent dividends. The recently filed US$356 million Pennsylvania rate increase is pivotal, as it aims to fund grid modernization, the biggest short-term catalyst. However, the real risk remains whether regulators will approve the rate hikes needed to cover PPL’s large investment plan; at this stage, the filing itself does not reduce that uncertainty.

Among PPL’s recent announcements, the reaffirmation of its 2025 earnings and dividend growth guidance stands out. This continued confidence, despite higher operating costs and the pending rate case, highlights management's expectations for resilience in cash flow, provided rate cases and investment returns proceed as planned alongside rising customer demand.

Conversely, investors should not ignore the heightened risk around regulatory lag and the possibility that …

Read the full narrative on PPL (it's free!)

PPL's narrative projects $9.6 billion revenue and $1.7 billion earnings by 2028. This requires 2.8% yearly revenue growth and a $714 million earnings increase from $986 million currently.

Uncover how PPL's forecasts yield a $38.31 fair value, a 4% upside to its current price.

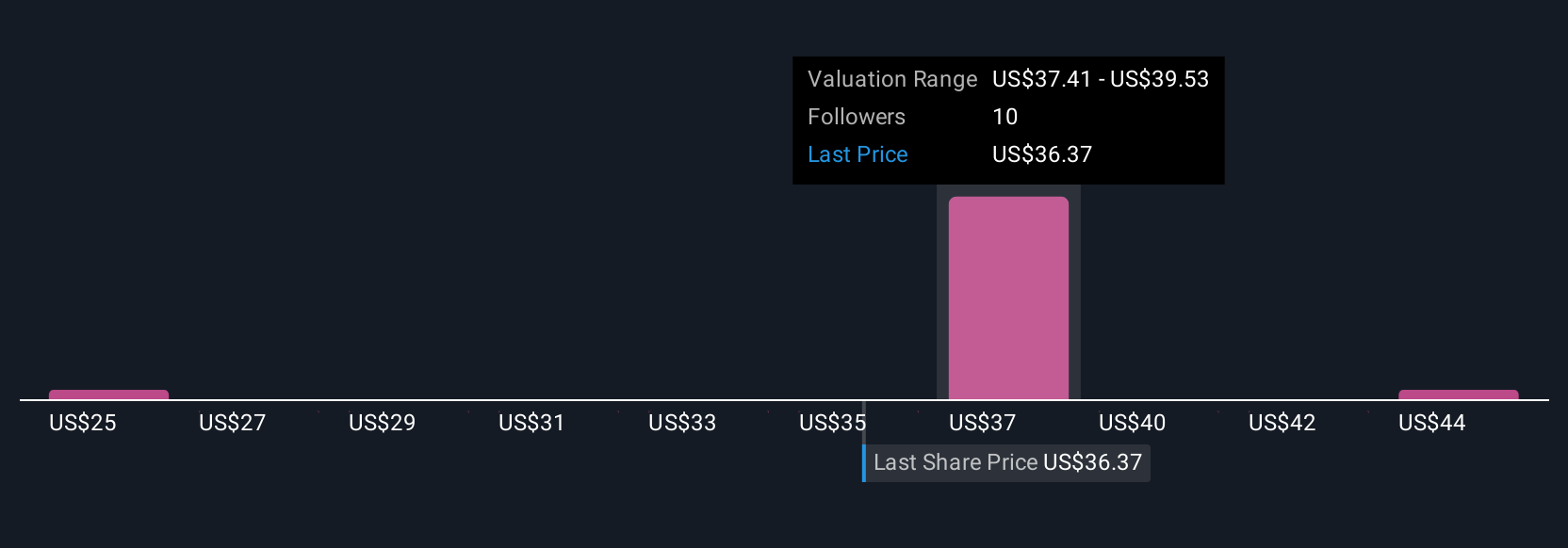

Exploring Other Perspectives

Simply Wall St Community valuations range from US$24.73 to US$45.87, with three individual perspectives collected. Regulatory approval of new rates will weigh heavily on how the company’s actual performance measures up, so consider these different viewpoints in light of what’s at stake for PPL’s future returns.

Explore 3 other fair value estimates on PPL - why the stock might be worth 33% less than the current price!

Build Your Own PPL Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your PPL research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free PPL research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate PPL's overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 32 companies in the world exploring or producing it. Find the list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PPL

PPL

Provides electricity and natural gas to approximately 3.6 million customers in the United States.

Solid track record and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

285 followersusers have followed this narrative

1 commentusers have commented on this narrative

42 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

95 followersusers have followed this narrative

2 commentsusers have commented on this narrative

25 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

8 followersusers have followed this narrative

3 commentsusers have commented on this narrative

3 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

62 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus The Amplify Reset, State-Backed, Debt-Disciplined, and Building Toward €400M FCF by 2030

Fair Value:€817.9% undervalued

39 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Loadstar Capital K.K ·

A positive setup for active capital recycling in 2026

Fair Value:JP¥6.18k51.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

95 followersusers have followed this narrative

2 commentsusers have commented on this narrative

25 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.230.7% undervalued

68 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9325.1% undervalued

1398 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative