Advertisement

- United States

- /

- Electric Utilities

- /

- NYSE:PNW

Pinnacle West Capital (PNW): Margin Decrease Reinforces Dividend and Financial Stability Concerns

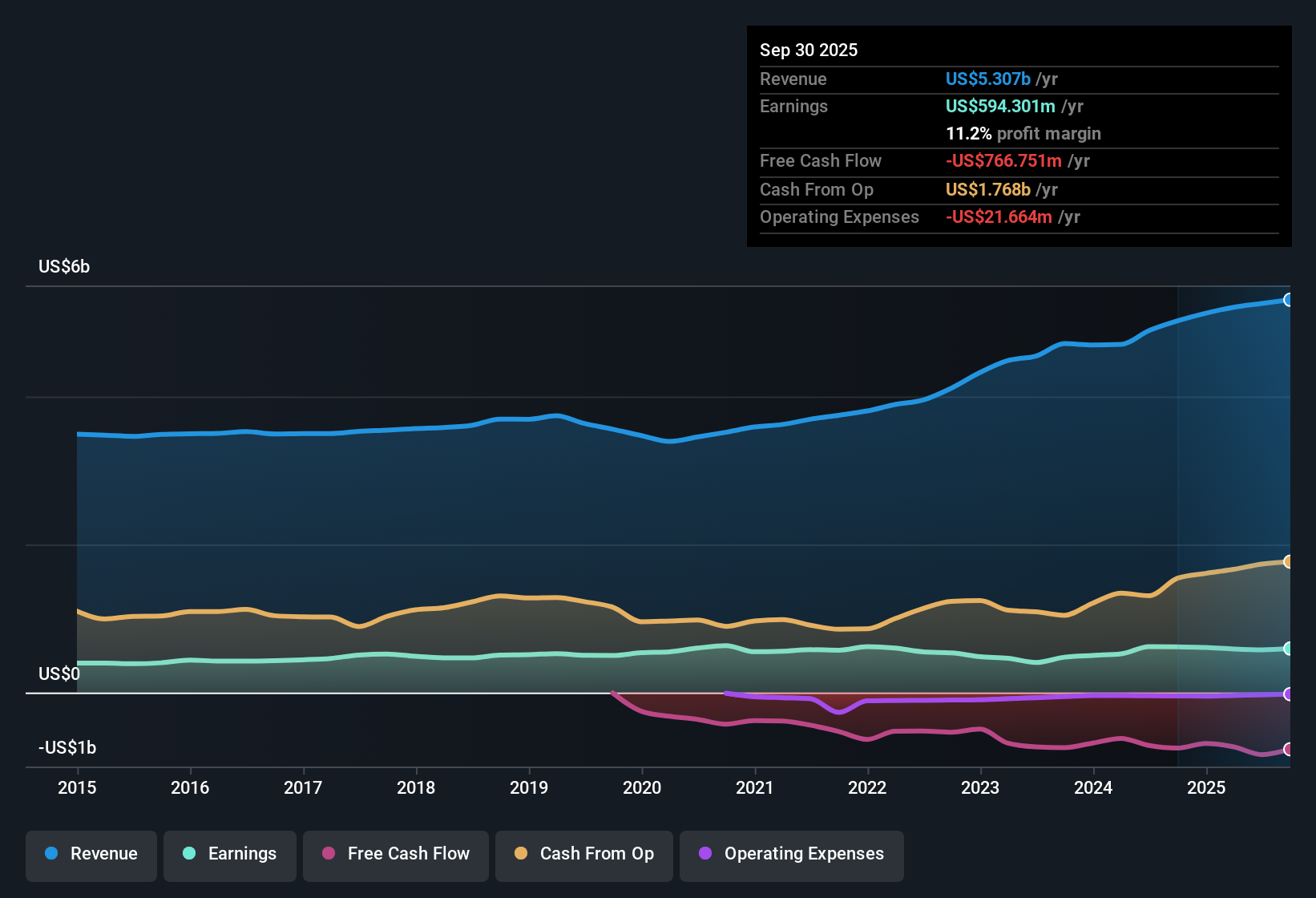

Pinnacle West Capital (PNW) is forecast to grow revenue at 4.7% per year, which trails behind the US market's expected 10.5% annual growth. Earnings are set to rise at a rate of 10.4% per year, while net profit margins have slipped to 11% from 12.7%. Over the past five years, earnings have averaged a 0.9% per year decline. Trading at $89.45 with a Price-To-Earnings Ratio of 18.5x, the stock sits just below its estimated fair value. Strong earnings quality and expectations of profit growth are keeping investors optimistic, despite some concerns over dividend sustainability and financial stability.

See our full analysis for Pinnacle West Capital.Next, we will compare these numbers with the prevailing narratives to determine whether the community view is supported or challenged by the actual results.

See what the community is saying about Pinnacle West Capital

Margin Recovery on the Horizon

- Analysts expect net profit margins to increase from 11.0% today to 13.0% by 2026, signaling a potential turnaround after the recent slip from 12.7%.

- According to the analysts' consensus view, forthcoming regulatory modernization and grid upgrades are seen as key levers to stabilize and improve margins, especially as these measures support better cost recovery and lessen the impact of regulatory lag.

- Consensus narrative notes that proposals for formula rate mechanisms and rate design reforms should help reduce lag, directly addressing margin pressures from recent capital projects.

- Grid modernization investments, such as wildfire mitigation and automation, are positioned as margin-friendly, helping insulate future profitability against rising operating and maintenance expenses.

- Consensus narrative suggests that this earnings momentum, if realized, could provide a stable foundation for long-term growth expectations, especially if forecasts for commercial and industrial demand materialize strongly.

Dividend and Debt Risks Resurface

- Pinnacle West Capital’s dividend sustainability and overall financial strength continue to be called into question, as risk screenings have flagged these areas for negative outcomes this period.

- Consensus narrative points to two underlying risks: first, that the ongoing reliance on fossil fuel infrastructure could raise long-term costs. Second, major regulatory decisions may not accommodate future capital recovery as quickly as needed.

- Bears highlight that cost recovery for large capital investments may lag behind, as the next significant rate relief is not expected until late 2026 and is tied to 2024 data, putting near-term margin improvement at risk.

- The lack of positive outcomes for dividend and financial position flags that even with profit growth forecasts, investors face uncertainty regarding cash distributions and balance sheet resilience.

Valuation Edge Versus Peers

- The current Price-To-Earnings Ratio of 18.5x stands below both sector (20.4x) and broader industry (21.5x) levels. With shares trading at $89.45, they sit just under the DCF fair value of $90.97.

- Consensus narrative sees this discount as making Pinnacle West Capital attractive in relative terms, with the 8.5% gap to the $95.79 analyst price target suggesting modest market upside if growth and margin improvements are achieved.

- The valuation gap could narrow if Pinnacle West delivers projected margin gains and revenue growth, which are both seen as credible by analysts despite recent earnings declines.

- Still, the close distance to fair value implies the stock is reasonably priced rather than a deeply undervalued opportunity. This reinforces the consensus that future results must deliver on improvement forecasts to justify upside.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Pinnacle West Capital on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Have a unique take on the figures? Shape that insight into your own narrative in just a few minutes. Do it your way.

A great starting point for your Pinnacle West Capital research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

See What Else Is Out There

Pinnacle West Capital faces uncertainty around its dividend reliability and overall financial health. Risk flags highlight concerns about balance sheet resilience and future cash distributions.

If you want more dependable fundamentals, check out solid balance sheet and fundamentals stocks screener (1978 results) to quickly spot companies with stronger balance sheets and robust financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PNW

Pinnacle West Capital

Through its subsidiary, provides retail and wholesale electric services in the state of Arizona.

Average dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

114 followersusers have followed this narrative

1 commentusers have commented on this narrative

20 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9823.0% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

30 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.0% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

12 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

EL

EllysiaL on Lynas Rare Earths ·

Lynas Rare Earths Will Continue to Surge Alongside The Transition To a Green Future

Fair Value:AU$33.3537.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Freehold Royalties ·

Freehold: Offers a fantastic growth-income intersection up to $50 WTI. Below $50 WTI, it may offer historic opportunities in terms of ROI.

Fair Value:CA$19.813.7% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Adobe ·

Adobe (ADBE): Record Q1 AI-Revenue and the End of the Shantanu Narayen Era

Fair Value:US$572.452.9% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.3% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59632.6% undervalued

1306 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9823.0% undervalued

36 followersusers have followed this narrative

0 commentsusers have commented on this narrative

30 likesusers have liked this narrative