Advertisement

- United States

- /

- Marine and Shipping

- /

- NYSE:ZIM

ZIM (ZIM) Is Down After Significant Drop in Q3 Earnings and EPS – What's Driving the Pressure?

Simply Wall St

Reviewed by Sasha Jovanovic

- ZIM Integrated Shipping Services Ltd. reported third quarter and nine-month earnings for 2025, with net income and earnings per share both decreasing significantly compared to the prior year, reaching US$123 million and US$1.02 per share for the quarter.

- This sharp decrease in profitability highlights ongoing pressures in the container shipping sector and prompts investors to reassess the company’s growth prospects.

- We'll examine how the pronounced drop in net income may reshape analyst expectations for ZIM’s future earnings and industry outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

ZIM Integrated Shipping Services Investment Narrative Recap

Owning ZIM Integrated Shipping Services often means believing in the company's ability to weather cyclical shocks and capitalize on shifts in global trade flows. With the latest earnings report revealing a sharp drop in profitability, near-term optimism will likely center on ZIM's capacity to defend margins despite volatile freight rates, while the biggest current risk is whether industry-wide overcapacity could keep pressuring rates for longer than expected, this latest update meaningfully raises that risk for the short term.

Among recent developments, ZIM’s move to charter ten dual-fuel LNG vessels totaling about US$2.3 billion stands out, reinforcing the company’s focus on fleet modernization and environmental compliance. This initiative directly connects to the ongoing catalyst of aligning with stricter emissions standards and attracting sustainability-focused shippers, but the pace and magnitude of cost advantages remain key questions after the disappointing earnings figures.

Yet, for investors, the real challenge comes if capacity keeps growing faster than demand...

Read the full narrative on ZIM Integrated Shipping Services (it's free!)

ZIM Integrated Shipping Services is forecast to generate $4.9 billion in revenue and $61.6 million in earnings by 2028. This outlook assumes an annual revenue decline of 16.8% and a significant earnings decrease of $1.94 billion from current earnings of $2.0 billion.

Uncover how ZIM Integrated Shipping Services' forecasts yield a $13.26 fair value, a 21% downside to its current price.

Exploring Other Perspectives

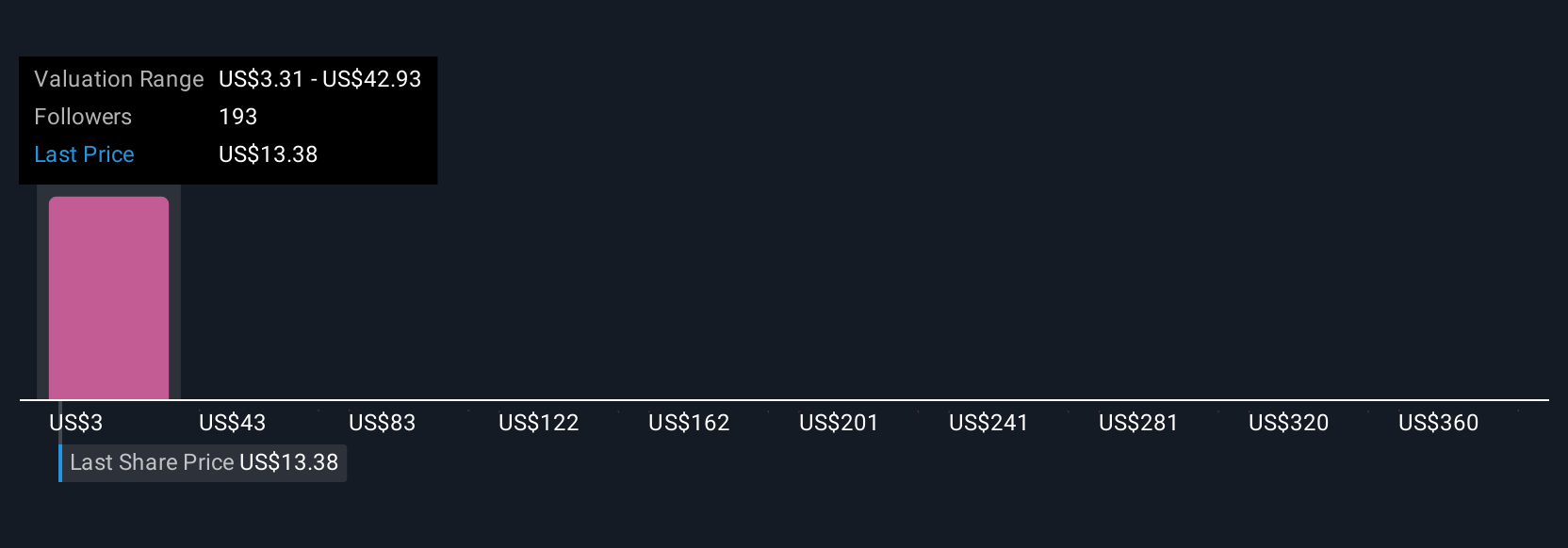

Fair value estimates from 34 Simply Wall St Community members for ZIM range from US$3.24 to US$452.35 per share. These widely differing views highlight how persistent industry overcapacity and volatile trade flows weigh on many investors’ outlooks for the company’s future performance.

Explore 34 other fair value estimates on ZIM Integrated Shipping Services - why the stock might be a potential multi-bagger!

Build Your Own ZIM Integrated Shipping Services Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your ZIM Integrated Shipping Services research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free ZIM Integrated Shipping Services research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ZIM Integrated Shipping Services' overall financial health at a glance.

Curious About Other Options?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if ZIM Integrated Shipping Services might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ZIM

ZIM Integrated Shipping Services

Provides container shipping and related services in Israel and internationally.

Excellent balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.3% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor