Advertisement

- United States

- /

- Construction

- /

- NYSE:NETI

New Forecasts: Here's What Analysts Think The Future Holds For Eneti Inc. (NYSE:NETI)

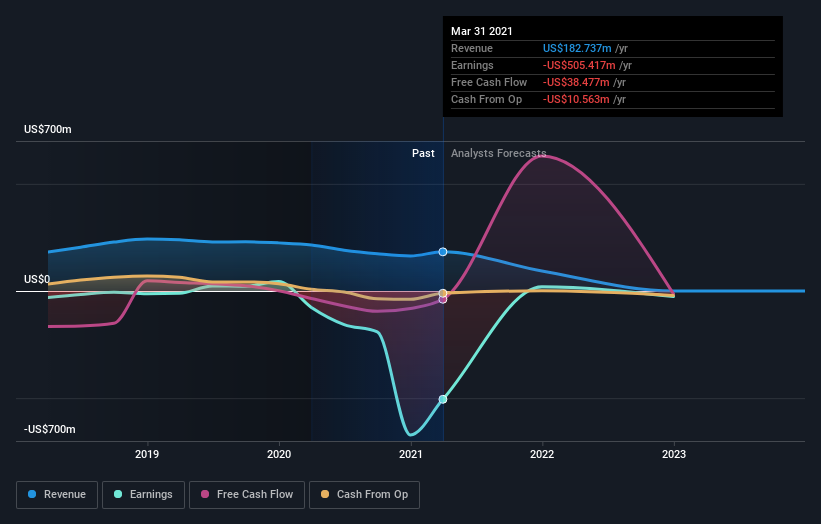

Shareholders in Eneti Inc. (NYSE:NETI) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

Following the latest upgrade, the current consensus, from the three analysts covering Eneti, is for revenues of US$123m in 2021, which would reflect a painful 33% reduction in Eneti's sales over the past 12 months. Prior to the latest estimates, the analysts were forecasting revenues of US$93m in 2021. It looks like there's been a clear increase in optimism around Eneti, given the considerable lift to revenue forecasts.

View our latest analysis for Eneti

There was no particular change to the consensus price target of US$29.33, with Eneti's latest outlook seemingly not enough to result in a change of valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Eneti at US$50.00 per share, while the most bearish prices it at US$18.00. We would probably assign less value to the forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. With this in mind, we wouldn't rely too heavily on the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 41% by the end of 2021. This indicates a significant reduction from annual growth of 17% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 4.5% annually for the foreseeable future. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Eneti is expected to lag the wider industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts lifted their revenue estimates for this year. They also expect company revenue to perform worse than the wider market. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Eneti.

Better yet, Eneti is expected to break-even soon - within the next few years - according to analyst forecasts, which would be a momentous event for shareholders. You can learn more about these forecasts, for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you’re looking to trade Eneti, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Eneti might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:NETI

Eneti

Eneti Inc. focuses on marine-based renewable energy through the installation of offshore commercial wind turbine generators.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|5.1% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|27.7% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.2% overvalued

LI

Community Contributor

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|64.4% undervalued

DA

Community Contributor