Advertisement

- United States

- /

- Transportation

- /

- NasdaqGS:GRAB

Grab (NasdaqGS:GRAB) Valuation: Is There Upside After Recent Sector-Wide Pullback?

Simply Wall St

Reviewed by Simply Wall St

Grab Holdings (GRAB) stock has moved quietly in recent sessions, with no major news events drawing investor attention. Shares have slipped about 13% over the past month, a trend that reflects broader patterns among Southeast Asian tech platforms.

See our latest analysis for Grab Holdings.

Grab’s recent slide lines up with a broad cooldown across its sector. Setting aside the latest dip, the company’s 3-year total shareholder return is still an impressive 66%. Momentum has faded compared to earlier rallies as investors weigh growth against changing risk appetite and valuation expectations.

If you’re curious about other tech-driven companies across markets, this could be the ideal moment to broaden your search and discover See the full list for free.

With analyst price targets suggesting nearly 40% upside and strong revenue growth, investors face a key question: Is Grab undervalued at current levels, or is the market already factoring in its future potential?

Most Popular Narrative: 40.2% Undervalued

With Grab’s last close at $4.90 and narrative fair value set at $8.20, according to BlackGoat, this narrative paints a much brighter long-term view than the current stock price suggests. The dramatic gap calls attention to bullish assumptions under the surface and signals there is more to the story than meets the eye.

“I assume a 20% CAGR in revenue over the next five years, driven by rising digital adoption in Southeast Asia, Grab’s ecosystem expansion, and deeper monetisation of payments and financial services. By year five, I project net profit margins of around 15% (up from 3.6%), supported by operating leverage at scale, tighter incentive discipline, and incremental contribution from Ads and Fintech.”

What drives such an aggressive upgrade? One secret lies in a bold profit margin play and a future earnings multiplier usually reserved for tech titans. Can this fast-growing super app make the leap? Uncover the key assumptions and see where the math leads in the full narrative.

Result: Fair Value of $8.20 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, competition in Indonesia and rising incentive costs could quickly challenge these bullish assumptions. This may shift the narrative and impact Grab’s long-term outlook.

Find out about the key risks to this Grab Holdings narrative.

Another View: Multiples Raise Questions

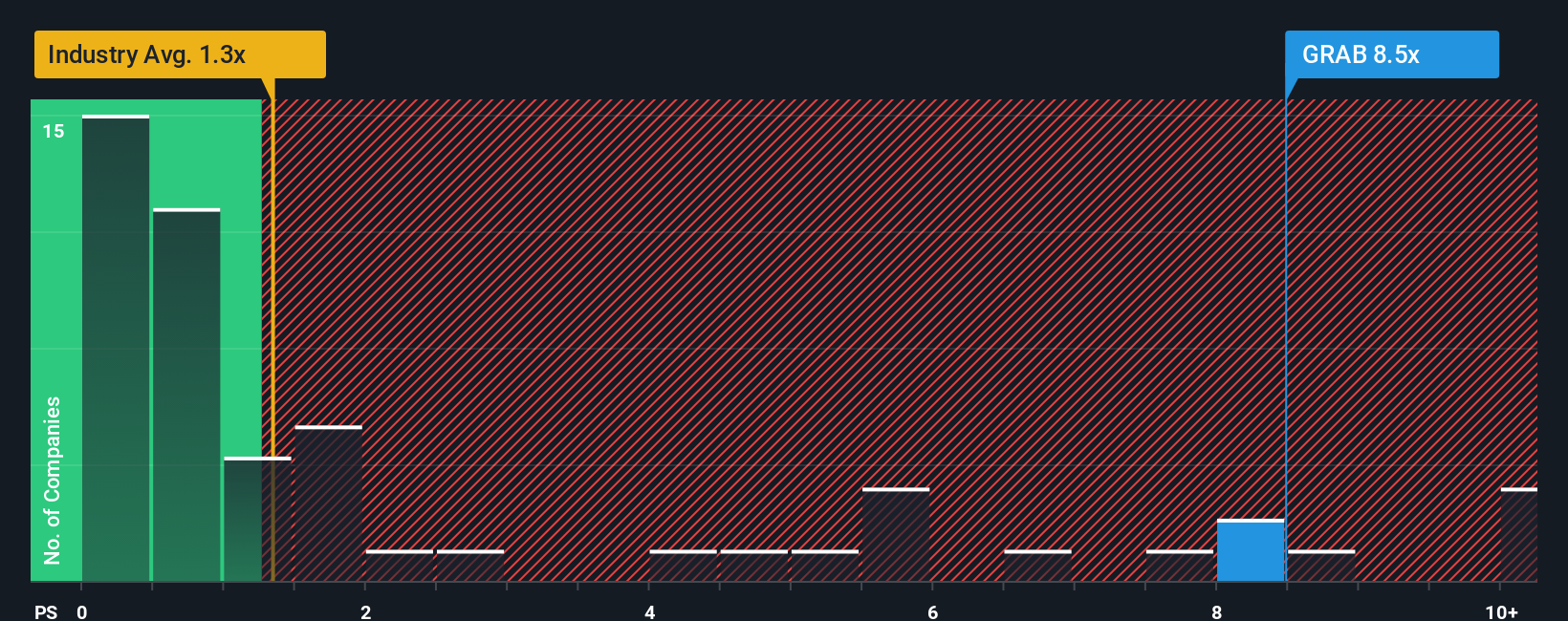

While the narrative fair value points to strong upside, comparing Grab's price-to-sales ratio (6.2x) to peers and industry averages tells a different story. The market is pricing Grab much higher than the US Transportation average of 1x and the peer average of 1.5x, with the fair ratio estimate at 3.5x. This premium suggests optimism but also signals valuation risk if growth slows. Could the market reset its expectations?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Grab Holdings Narrative

If you see the numbers differently or want to dig deeper, you can craft your own Grab Holdings narrative swiftly. It takes no more than three minutes. Do it your way

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Grab Holdings.

Looking for More Investment Ideas?

Stay ahead of the market and discover unique opportunities you might otherwise miss by tapping into hand-picked stock ideas that go beyond the obvious picks.

- Tap into future trends by checking out these 25 AI penny stocks, which are harnessing artificial intelligence breakthroughs for exponential growth.

- Secure steady payouts when you browse these 17 dividend stocks with yields > 3%, offering attractive yields above 3% for income-focused investors.

- Catalyze your portfolio’s performance with these 917 undervalued stocks based on cash flows, which stand out for their compelling cash flow valuations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:GRAB

Grab Holdings

Engages in the provision of superapps in Cambodia, Indonesia, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor