Advertisement

- United States

- /

- Transportation

- /

- NasdaqGS:CAR

How Weak Rental Demand and Financing Needs Are Shaping Avis Budget Group’s (CAR) Investment Story

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier in November, Avis Budget Group was ranked third behind Enterprise and Hertz as the best domestic car rental company at the Travvy Awards, based on votes from thousands of travel advisors.

- Recent reports highlight disappointing rental demand, diminishing returns on capital, and constrained cash reserves, raising new questions about Avis Budget Group’s ability to maintain profitability without resorting to costly financing options.

- We will examine how rising concerns over Avis Budget Group’s fundamentals and financing challenges could alter its investment narrative.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Avis Budget Group Investment Narrative Recap

To be an Avis Budget Group shareholder right now, you would need to believe the company can adapt to weak rental demand and capital pressures by successfully advancing its premiumization and digital transformation strategy. The recent Travvy Awards ranking, while positive for brand reputation, does not appear to meaningfully shift the biggest short-term catalyst, the rollout of new premium offerings or the most pressing risk, which is the company's current cash constraints and the risk of resorting to expensive financing.

Of the latest company updates, the October launch of Avis First, a premium concierge service, stands out as particularly relevant given the industry trend toward higher-margin offerings. This new product aligns closely with the company's growth narrative and could provide near-term upside if it succeeds in capturing the elevated spend of travel customers seeking more personalized rental experiences.

In contrast, investors should be aware that mounting concerns about limited cash reserves could increase the company's exposure to unfavorable financing costs if short-term...

Read the full narrative on Avis Budget Group (it's free!)

Avis Budget Group's narrative projects $12.2 billion revenue and $1.0 billion earnings by 2028. This requires 1.4% yearly revenue growth and a $3.2 billion increase in earnings from the current level of -$2.2 billion.

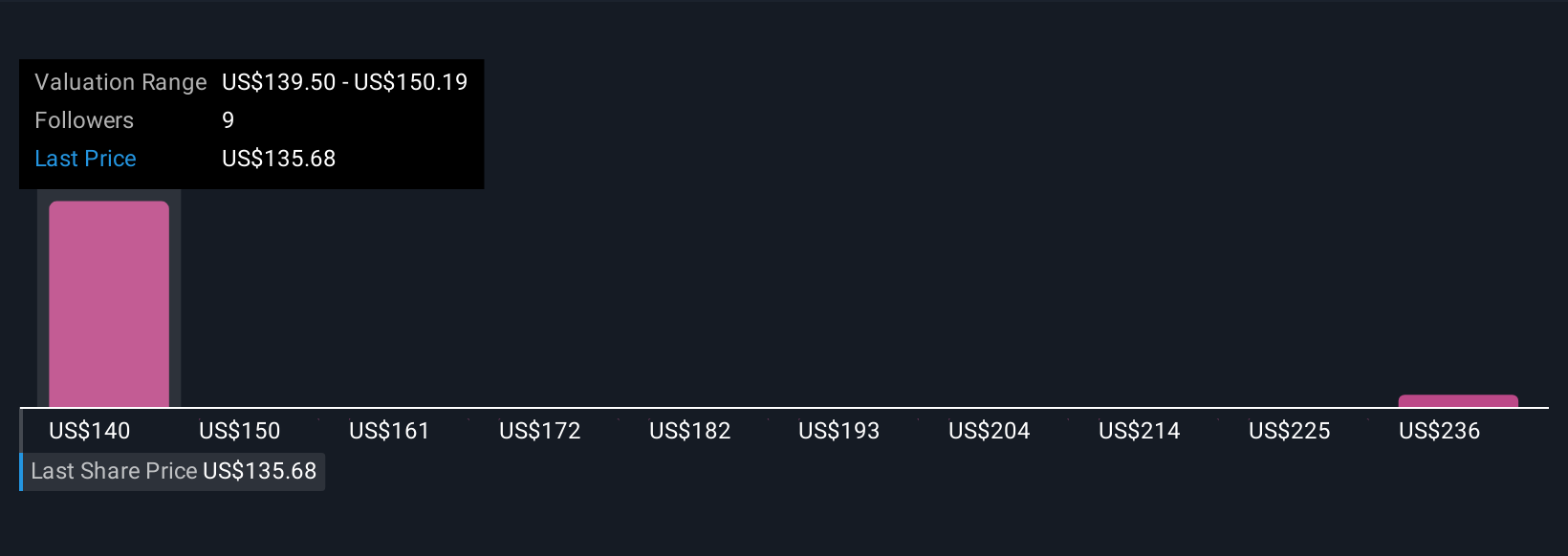

Uncover how Avis Budget Group's forecasts yield a $135.75 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members place Avis Budget Group's fair value between US$135.75 and US$246.44, based on two unique estimates. While opinions differ, ongoing cash flow and funding risks may shape future outcomes and spark further debate among market participants.

Explore 2 other fair value estimates on Avis Budget Group - why the stock might be worth as much as 84% more than the current price!

Build Your Own Avis Budget Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Avis Budget Group research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Avis Budget Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Avis Budget Group's overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CAR

Avis Budget Group

Provides car and truck rentals, car sharing, and ancillary products and services to businesses and consumers in the Americas, Europe, the Middle East and Africa, Asia, and Australasia.

Fair value with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

134 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

82 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

919 followersusers have followed this narrative

5 commentsusers have commented on this narrative

21 likesusers have liked this narrative