Advertisement

- United States

- /

- Wireless Telecom

- /

- NYSE:AD

A Look At Array Digital Infrastructure’s Valuation After Strong Q4 Results And 2026 Guidance

Array Digital Infrastructure (AD) has drawn fresh attention after fourth quarter results showed sales of US$54.99 million, revenue of US$60.33 million, and net income of US$37.48 million, alongside 2026 revenue guidance of US$200 million to US$215 million.

See our latest analysis for Array Digital Infrastructure.

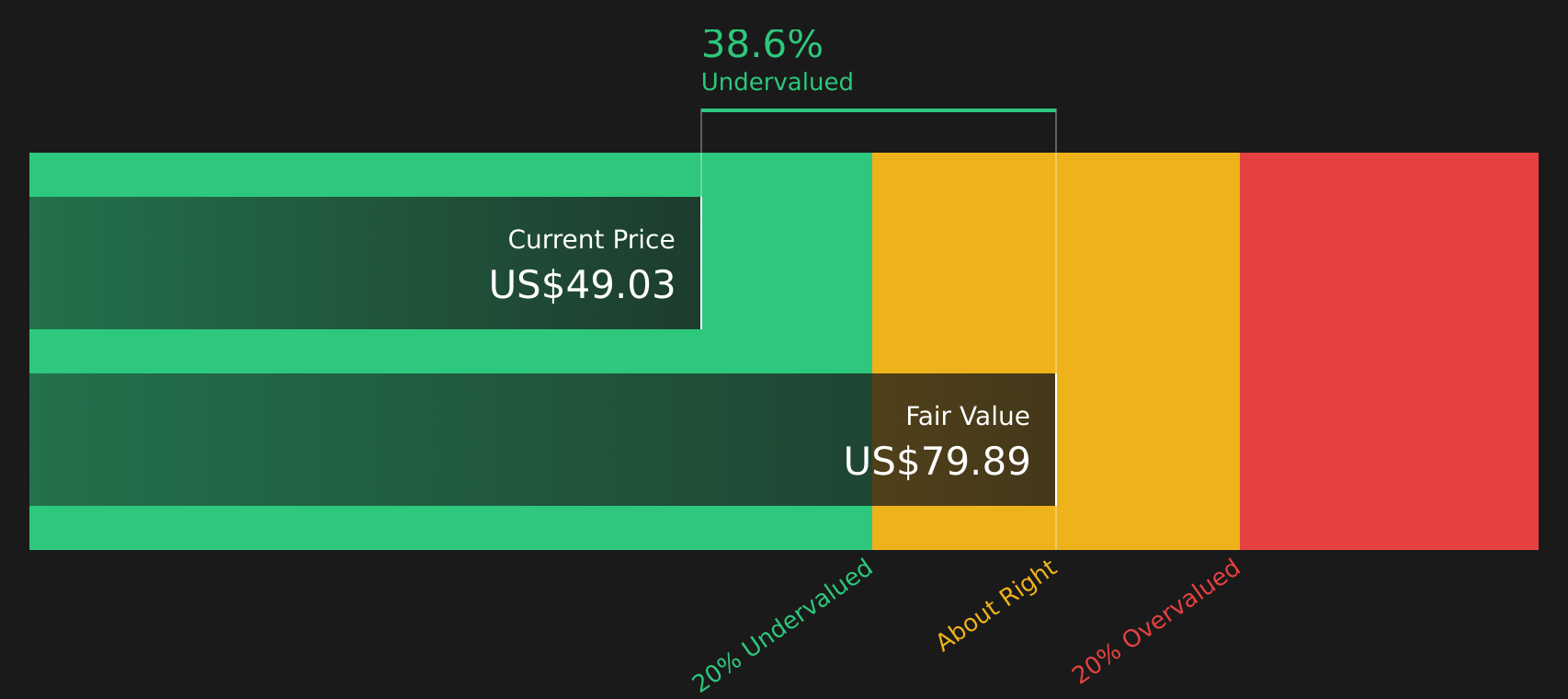

The recent earnings release and 2026 revenue guidance arrived alongside a 1 day share price return of 1.18% to US$48.88. However, the year to date share price return is a 9.48% decline, while the 1 year total shareholder return of 32.97% and very large 3 year total shareholder return of around 3.8x suggest longer term momentum has been stronger than in the latest quarter.

If Array Digital Infrastructure has you looking more closely at wireless and data infrastructure, it could be a good time to scan our list of 34 AI infrastructure stocks as potential next ideas.

With earnings growing and the share price still below some intrinsic value estimates, the big question is whether Array Digital Infrastructure is quietly undervalued or if the market is already pricing in much of its future growth?

Most Popular Narrative: 16% Undervalued

Array Digital Infrastructure’s latest fair value narrative points to a value of about $58.17 per share compared with the last close at $48.88. This puts the spotlight on what is driving that gap.

The analysts have a consensus price target of $80.75 for United States Cellular based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $85.0, and the most bearish reporting a price target of just $72.0.

In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be $3.6 billion, earnings will come to $173.7 million, and it would be trading on a PE ratio of 46.4x, assuming you use a discount rate of 6.8%.

Curious how that fair value is built? The narrative leans on revenue stabilising, margins pushing higher, and a rich future earnings multiple that is usually reserved for faster growing names. You may want to see exactly which assumptions around profitability, cash flows and required return had to line up to reach that conclusion.

Result: Fair Value of $58.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this depends on key swing factors, including regulators approving major spectrum transactions and wireless competition not constraining tower and service revenues more than expected.

Find out about the key risks to this Array Digital Infrastructure narrative.

Another Angle On Valuation

While the fair value narrative suggests Array Digital Infrastructure is trading about 16% below an implied $58.17 per share, our DCF model points to a value of $75.22 based on projected cash flows. With that kind of difference, which set of assumptions do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

All of this might sound either encouraging or cautious. Move quickly to check the full picture for yourself and weigh the trade off between upside and risk with 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If this story has you thinking about what else might be hiding in plain sight, do not stop at one ticker when the screener can surface dozens.

- Target potential value opportunities before they get crowded by checking our list of 49 high quality undervalued stocks that currently screen well on fundamentals and pricing.

- Prioritise resilience and sleep easier by scanning 75 resilient stocks with low risk scores, focused on companies that show lower overall risk scores in the model.

- Get ahead of the crowd by reviewing the screener containing 24 high quality undiscovered gems, where strong underlying numbers have not yet attracted widespread attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:AD

Array Digital Infrastructure

Owns and operates shared wireless communications infrastructure in the United States.

Mediocre balance sheet unattractive dividend payer.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

284 followersusers have followed this narrative

1 commentusers have commented on this narrative

41 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

92 followersusers have followed this narrative

1 commentusers have commented on this narrative

23 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

7 followersusers have followed this narrative

3 commentsusers have commented on this narrative

3 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

62 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on Evaxion ·

The "AI-Immunology" Asymmetric Opportunity – Validated by Merck (MSD)

Fair Value:US$20.2579.9% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AnonymousPlanner on Adobe ·

Good Value for a Creative Monopoly

Fair Value:US$317.6619.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Ronesans Gayrimenkul Yatirim ·

Investing in the future with RGYAS as fair value hits 228.23

Fair Value:₺313.4139.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

92 followersusers have followed this narrative

1 commentusers have commented on this narrative

23 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.230.7% undervalued

68 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9325.1% undervalued

1396 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative