Advertisement

- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:TTMI

Assessing TTM Technologies (TTMI) Valuation After Strong Recent Share Price Momentum

TTM Technologies (TTMI) has attracted fresh attention after recent share price moves, prompting investors to reassess its role in printed circuit boards and RF components, alongside reported revenue of US$2.91b and net income of US$177.45m.

See our latest analysis for TTM Technologies.

The 1 month share price return of 40.47% and 90 day share price return of 47.75% point to strong recent momentum, while the very large 1 year and 3 year total shareholder returns suggest this move extends a much longer run.

If this surge in returns has you looking beyond a single name, it could be a good moment to see what else is happening in advanced electronics through our 28 robotics and automation stocks.

With TTM Technologies trading at US$98.58 against an analyst price target of US$118.50 and an internal estimate suggesting a sizeable intrinsic discount, you have to ask: is this a genuine mispricing, or is the market already factoring in future growth?

Most Popular Narrative: 4.5% Undervalued

Compared with a fair value estimate of $103.25, TTM Technologies at $98.58 sits slightly below what the most followed narrative assumes is reasonable, framing the recent price run in a different light.

Ongoing expansion into higher-value engineered solutions and advanced manufacturing capabilities, particularly through new capacity in Penang, Syracuse, and product mix shifts, increases pricing power and drives gross margin improvements over time, enhancing net margin profile.

Curious what kind of revenue mix and margin profile could support that valuation gap, and what future earnings power is baked into those assumptions? The narrative spells out a detailed path for growth, profitability and the future P/E investors would need to accept to line that fair value up with today’s price.

Result: Fair Value of $103.25 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story can change quickly if high operating costs at new facilities or customer concentration issues begin to weigh on margins and cash generation.

Find out about the key risks to this TTM Technologies narrative.

Another Angle On Valuation

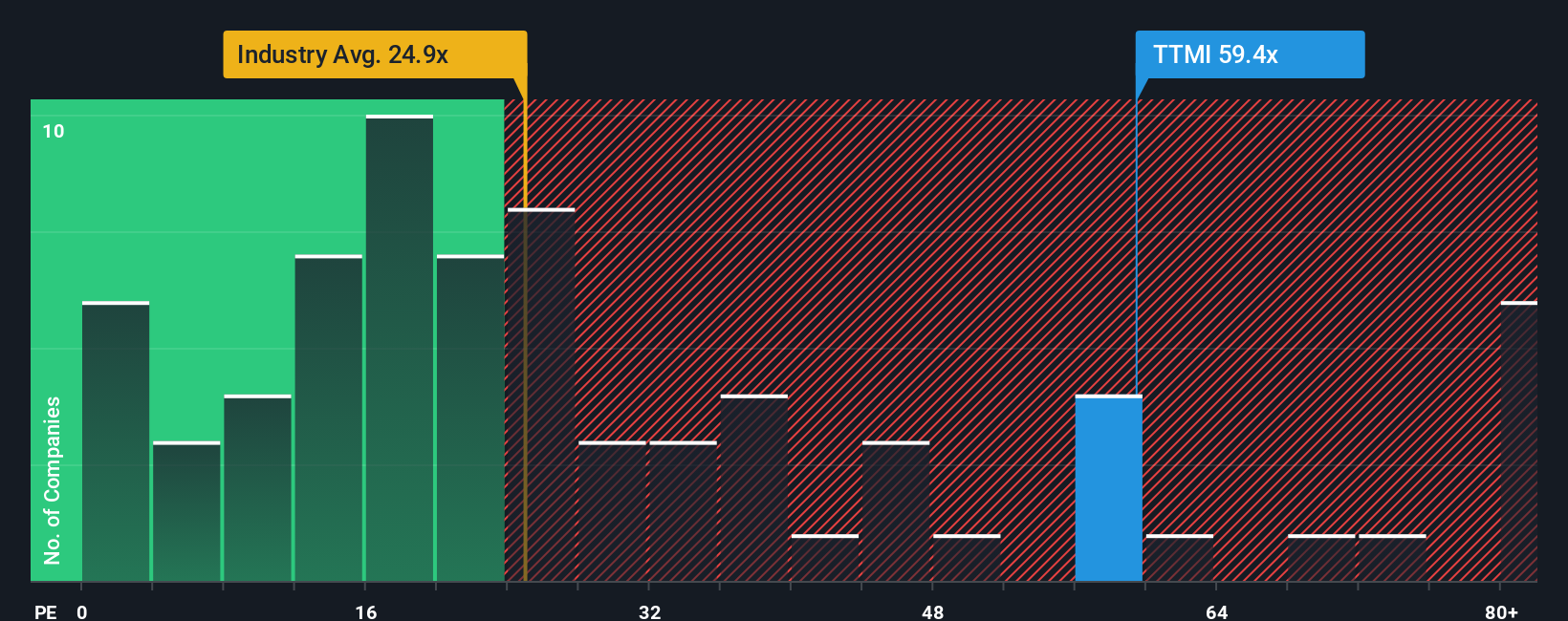

The earlier view leans on future cash flows, but the current P/E around 57.4x tells a different story. That is above the US Electronic industry at 27.4x, the peer average at 35.6x, and even our fair ratio of 50.6x. This raises a simple question: how much optimism are you really paying for?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own TTM Technologies Narrative

If you look at these numbers and reach a different conclusion or just prefer to run your own checks, you can build a custom view in minutes: Do it your way.

A great starting point for your TTM Technologies research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If TTM Technologies is on your radar, do not stop there. Broaden your watchlist with other opportunities that match the kind of portfolio you want to build.

- Spot potential value ideas early by scanning companies that show up in our screener containing 24 high quality undiscovered gems and might not yet be on everyone else’s list.

- Build a sturdier core for your portfolio by filtering companies using the solid balance sheet and fundamentals stocks screener (45 results) so you can focus on financial strength first.

- Target a mix of cash flow and yield by reviewing the income candidates in our 14 dividend fortresses before the crowd turns its attention to them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TTM Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TTMI

TTM Technologies

Manufactures and sells mission systems, radio frequency (RF) components, RF microwave/microelectronic assemblies, and printed circuit boards (PCBs) and substrates in the United States, Taiwan, and internationally.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

284 followersusers have followed this narrative

1 commentusers have commented on this narrative

41 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

94 followersusers have followed this narrative

1 commentusers have commented on this narrative

24 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4524.2% undervalued

7 followersusers have followed this narrative

3 commentsusers have commented on this narrative

3 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2803.2% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

MI

mircea582 on TriplePoint Venture Growth BDC ·

Why a 46 % NAV Discount May Be Mispriced

Fair Value:US$3.7659.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on Meta Bright Group Berhad ·

Meta Bright’s Bumidotearth Move: A Small Acquisition With Bigger Strategic Implications

Fair Value:RM 0.568.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AndrewHabib on NuScale Power ·

NuScale Power will achieve impressive revenue growth if Entra1 can deliver

Fair Value:US$13.537.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.3% undervalued

94 followersusers have followed this narrative

1 commentusers have commented on this narrative

24 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.230.7% undervalued

68 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9325.1% undervalued

1397 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative