Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:SMCI

Super Micro Computer (SMCI): Evaluating Valuation After Weak Earnings, Outlook, and Internal Controls Disclosure

Reviewed by Simply Wall St

If you own or are watching Super Micro Computer (SMCI), the past month may have put you on edge. The stock has tumbled nearly 30% following news of disappointing Fiscal Q4 earnings, a weaker outlook, and, most concerning to many, fresh disclosures of material weaknesses in SMCI’s internal financial controls as of June 30, 2025. While the company has launched efforts to shore up its procedures, investors remain uneasy as there is no clear assurance that these issues will be swiftly resolved.

Looking at the bigger picture, it is not just this quarter’s stumble attracting attention. Over the year, SMCI’s share price has slipped a touch below where it started, lagging broader markets and further dampened by the recent setbacks. However, put this next to its long-term returns alongside annual revenue and net income growth, and you have a company many once associated with strong performance. That momentum now seems to be at a crossroads: declining in the short run, yet still supported by a multi-year track record of robust expansion and buyback activity.

So with all this turbulence, is the market overreacting, or is it simply pricing in the risks and dialing back expectations for future growth?

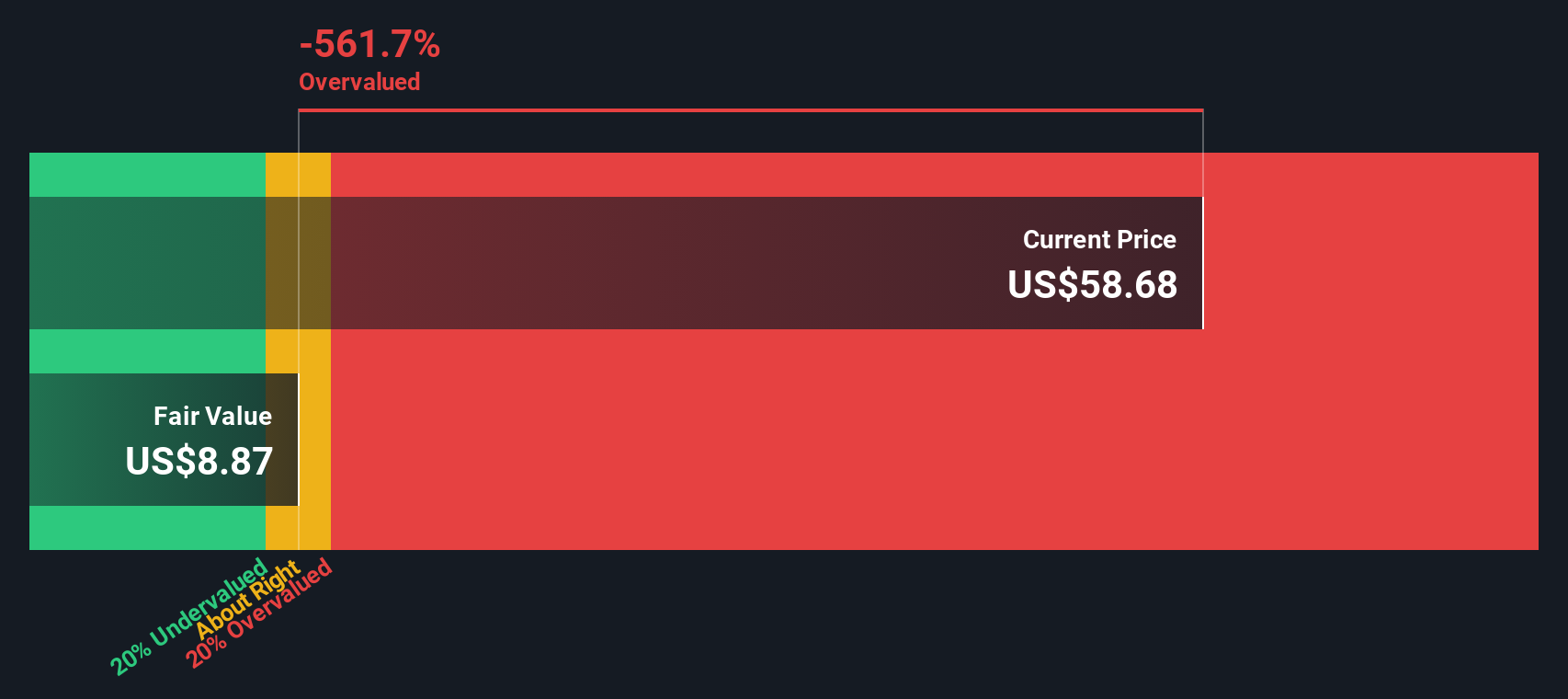

Most Popular Narrative: 46% Undervalued

According to DavidWSC, the most widely followed narrative sees SMCI shares trading at a significant discount to what underlying fundamentals could justify.

Partnerships with NVDA, AMD, xAI and Intel make them one of the most attractive providers of GPU data center infrastructure. The company also continues to profit from growth in other related industries such as Cloud, 5G and Storage. Using the SWS Fair Value tool and management's guidance of $23bn for 2025 and $40bn for 2026, I decided to use a revenue growth rate of 50% to reach an estimated revenue of $50bn for 2028, which I view as conservative.

Want to know what bold bets lie behind this massive undervaluation claim? The story hinges on game-changing growth rates and a future profit multiple that could rival the tech giants. Which data points flip the narrative from caution to optimism? Discover the crucial numbers at the heart of this bullish fair value estimate.

Result: Fair Value of $74.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, lingering worries about audit scrutiny and slower data center adoption could easily dampen this optimistic outlook if conditions deteriorate further.

Find out about the key risks to this Super Micro Computer narrative.Another View: Discounted Cash Flow Sends a Different Signal

While the narrative points to undervaluation, our DCF model sees things quite differently. This method suggests the shares may be trading above their intrinsic value. Investors are prompted to weigh both stories carefully. Which approach better captures reality?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own Super Micro Computer Narrative

If you see things differently or enjoy digging into the numbers yourself, take a few minutes to uncover your own perspective on SMCI. Do it your way

A great starting point for your Super Micro Computer research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don't settle for what's trending. Tap into unique opportunities and set your strategy apart. Handpick stocks built to perform by using these powerful tools today:

- Unlock the potential of technology’s next wave by scanning for quantum computing stocks, where innovation meets exponential growth.

- Generate income you can count on by checking out companies offering dividend stocks with yields > 3% for reliable yields above the market average.

- Spot bargains the market is missing when you search for undervalued stocks based on cash flows. Boost your portfolio with stocks priced below their real worth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:SMCI

Super Micro Computer

Develops and sells server and storage solutions based on modular and open-standard architecture in the United States, Asia, Europe, and internationally.

Exceptional growth potential with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Optimi Health ·

The Only Psychedelic Company Already Selling MDMA and Psilocybin to Real Patients, Yet Priced Like It Doesn’t Exist

Fair Value:US$1157.5% undervalued

47 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

WE

WealthAP on Novo Nordisk ·

Novo Nordisk (NVO): Is the "Easy Growth" Story Over?

Fair Value:DKK 407.7721.4% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

VA

ValueInvestingSubstack on Zoetis ·

Zoetis down -50% over the past year

Fair Value:US$92.9218.9% undervalued

23 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

CE

CentryResearch on Centrus Energy ·

Centrus Energy: The Next Nuclear Bottleneck Isn't Reactors. It's Fuel.

Fair Value:US$19013.7% undervalued

24 followersusers have followed this narrative

0 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

WI

WisetoWealth on PayPal Holdings ·

The Underrated Transformation of a Digital Payments Giant

Fair Value:US$90.3137.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

Blagget on Terra Balcanica Resources ·

The C$4M Explorer Positioned to Become Europe's First Antimony Mine

Fair Value:CA$0.487.5% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

david_6nroa on Charter Communications ·

Charter is undervalued - Here's why.

Fair Value:US$87.0741.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.919.1% undervalued

81 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28026.1% undervalued

185 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

BE

benjamin_lvieq on PayPal Holdings ·

PayPal: PayPal Doesn't Need to Grow – It Needs to Stop Falling – A Mispriced Cash Machine With a Cannibal Buyback

Fair Value:US$6513.6% undervalued

71 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

DE

derek_3wsdg on Teladoc Health ·

You’ve overlooked the activist investor factor. Travis Cocke’s Voss has announced 5% ownership through a 13G filing. They’ve added to that 5% since, and in doing so, have created a structural trap door for 27.42 Million Shares actively sold short. Chuck will announce lots of positives on July 29 but it’s what Voss announces shortly after that will rock the overextended Teledoc shorts. The Walmart partnership is the tip of the iceberg. The market is missing the sheer regulatory and enterprise friction of modern corporate healthcare. Teladoc isn't a "consumer app"; it is the primary digital infrastructure integrated directly into the legacy backends of Tier-1 insurance companies and fortune 500 employers, covering 105 million+ lives. Teladoc is acting as the digital top-of-funnel engine for the world's largest retailer. If Voss pushes the narrative that Teladoc is effectively the outsourced digital brain of Walmart's entire healthcare footprint, the fair value shifts from a basic health multiple to an enterprise distribution premium. Additionally , we are in a structural gold rush for high-quality, legally compliant, longitudinal medical data to train vertical healthcare AI models. Large technology hyperscalers and pharmaceutical giants cannot simply scrape the internet for this; they need structured clinical inputs. Teladoc sits on one of the largest de-identified virtual medical datasets on earth. From the activist playbook , we’ll see Voss demand the immediate creation of a Data & Diagnostics Licensing Division, transforming a legacy liability into an incredibly high-margin, pure-software data asset that requires zero human clinician hours to scale. Chuck is doing great work and deserves credi5 for the Teledoc turnaround but it will be Travis Cocke who will be responsible for a share price way beyond your $15 valuation.

1

|0